A milder reliability assessment, 58 GW of new resources, and softening load forecasts have eased the near-term mood. Analysts and executives warn the breathing room is borrowed time.

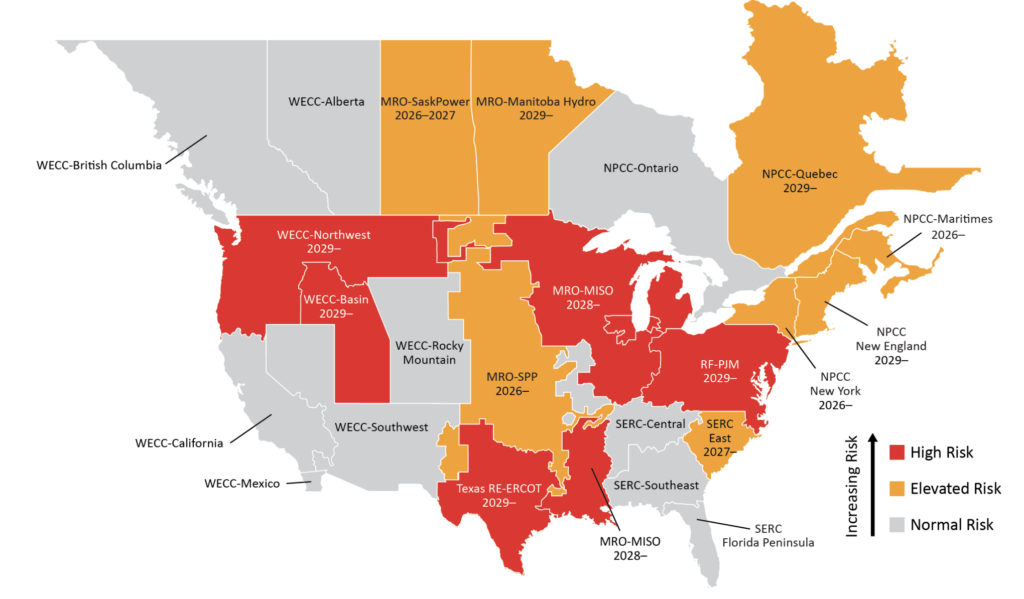

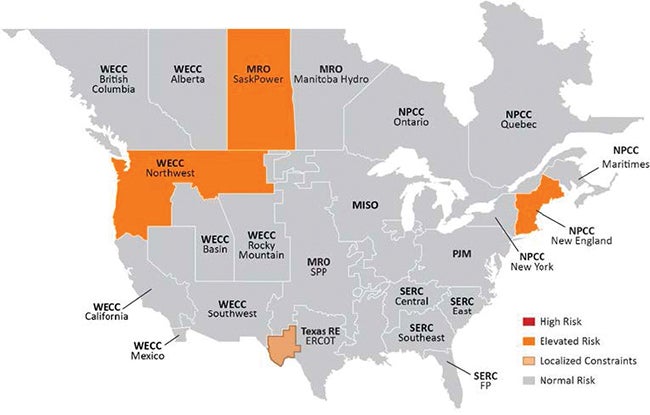

For the first time in several summers, the North American grid is heading into the cooling season without a single region flagged as high-risk. The North American Electric Reliability Corporation’s (NERC’s) 2026 Summer Reliability Assessment, released in May, found every assessment area carries adequate anticipated resources for normal peak conditions, and it identified only a handful of areas—New England, SaskPower, the Northwest, and pockets of Far West Texas—facing elevated risk under more extreme scenarios. The bulk power system added slightly more than 58 GW of new resources year on year, a build-out large enough to outpace demand growth and lift reserves across much of the continent (Figure 1).

|

|

1. The North American Electric Reliability Corporation’s (NERC’s) 2026 Summer Reliability Assessment expects sufficient operating reserves across most of its jurisdiction, with elevated risk only in parts of New England, Texas, Saskatchewan, and the Northwestern U.S. Courtesy: NERC |

That is a notably calmer reading than the one NERC delivered a year earlier, and the reasons run deeper than a single mild forecast. Aggregated peak demand still climbed by more than 11 GW from the prior summer’s projections—growth that actually exceeds the 10-GW rise that preceded summer 2025—but several assessment areas have revised their load forecasts downward to account for large loads arriving more slowly than anticipated. The grid, in other words, caught a break on both ends: more supply showed up, and some of the demand that planners feared did not.

The question dominating mid-year conversations is whether that break is structural or simply a pause. Across keynote remarks by utility and equipment executives at the Edison Electric Institute’s (EEI’s) annual gathering—held this year in Las Vegas, Nevada, during the first week of June—and interviews with analysts at major research and advisory firms, the answer arrives with striking consistency: this is a reprieve, not a turning point. The forces that produced the calmer outlook—slower data center interconnection, a wave of solar and battery additions, and favorable timing—are the same forces that could reverse, and most of the people building and financing the system are planning for the harder scenario to return by the end of the decade.

The Load That Hasn’t Arrived Yet

The single biggest driver of the softer outlook is also its most fragile assumption. Large computational loads, chiefly data centers, are connecting to the grid more slowly than developers projected a year ago, and that lag has quietly relieved pressure that planners had braced for.

In This Issue

Full issue“The pace of data center interconnection may be slower than anticipated,” said Doug Giuffre, head of Americas Power and Renewables at S&P Global Energy. “The intensifying local opposition to data centers may slow the pace at which new projects are completed. This may ease some of the near-term supply challenges facing the industry as the delays allow for power infrastructure to be installed.” He pointed directly to NERC’s own language—that multiple areas revised forecasts downward to reflect “the observed rate of completion for large load interconnections and the slower-than-expected pace at which some of those loads are coming on-line.”

The Electric Reliability Council of Texas (ERCOT) offers the clearest illustration. The Texas Interconnection, long the poster child for runaway demand, actually saw its net internal demand forecast fall 4.6% from last summer, the result of updated load modeling that better reflects how large computational loads behave at peak and how much of that load operators can curtail in an emergency. The revision helped push ERCOT’s anticipated reserve margin to a comfortable 67.9% and dropped its modeled probability of declaring an energy emergency during the August peak hour to 0.43%, down from 3.1% a year earlier—a decline NERC attributes largely to continued battery storage additions.

But the relief is widely understood to be a timing artifact, not a reversal. “Large loads are connecting to the electric grid more slowly than anticipated, which has helped mitigate the near-term supply challenges,” Giuffre said. “But substantial new load is slated for operation over the next 2–3 years and will require a stronger supply response.” S&P Global projects more than 85 GW of incremental gas capacity entering commercial service between 2026 and 2030, and Giuffre cautioned that firm supply, not just nameplate, is what the system will need.

His colleague Hill Vaden, S&P Global Energy’s executive director for Financial and Capital Markets, framed the underlying problem as one the industry has been slow to internalize: how much capacity factors actually matter. “Industry has been so focused on the growth in absolute capacity over the past decade or so that it’s overlooked tightness in effective capacity. The rise of AI [artificial intelligence]–oriented data centers is bringing this imbalance into focus for developers and policymakers,” he said. A grid can add gigawatts of nameplate and still tighten if those gigawatts cannot deliver when demand peaks.

A Supply Response Constrained at Every Turn

If demand is merely deferred, the obvious answer is to keep building. The harder truth is that the most-wanted firm capacity—new natural gas generation—is more difficult to finance and slower to deliver.

“New gas generation is difficult to build with capital costs in the $2,000–$3,000/kW range,” said Scott Wilmot, principal analyst at Enverus Intelligence Research. “In this cost range, economics and debt service coverage ratios are below where they need to be to get financed. This issue is compounded in an energy-only market like ERCOT. We either need capacity prices above the cap in PJM or long-term premium PPAs [power purchase agreements] with offtakers.” Wilmot sees PJM’s proposed reliability backstop procurement, under which generators would sign long-term bilateral agreements directly with loads, as a step toward getting expensive gas built—though he noted that questions about cost allocation and ratepayer affordability remain unresolved.

The equipment to build those plants is its own constraint. Gas turbine backlogs have stretched years into the future, and the manufacturers racing to expand are running into the limits of supply chains and skilled labor. Siemens Energy President and CEO Christian Bruch (Figure 2), who recently committed more than $1 billion to scale up U.S. production of grid and gas turbine equipment, described an investment pushing in three directions at once: capacity expansion, supply chain reinforcement, and workforce. The last, he argued, is the one the industry keeps shortchanging.

|

|

2. Harry Sideris, president and CEO of Duke Energy, and Christian Bruch, president and CEO of Siemens Energy, on stage at the Edison Electric Institute (EEI) 2026 event. Source: POWER |

“Everybody at the moment discusses about what to build, but I think we have to think about what to operate and what to service,” Bruch said at EEI 2026. “We will need a lot of workforce.”

That observation captures a defining feature of the U.S. market in 2026. “In the U.S., everything is at the moment about speed to electricity—give me an electron as fast as possible—and then the other things are lower prioritized,” Bruch said, noting that this is very specific to the U.S. because of the race for AI supremacy. He contrasted it with Europe, where capital is flowing toward grid resilience, and Asia, where the priority is general electrification—a reminder that the American obsession with raw speed is not universal.

Trade policy has made the build harder to plan. Bruch said the swings in U.S. tariffs have forced his company to repeatedly rethink where it fabricates and how it runs its supply chain. “You cannot change the scheme every 12 months,” he said—qualifying a new component supplier takes far longer than that. The net effect, he argued, is a global push toward local fabrication and supplier diversification, a hedge that will take “decades” to complete. Siemens Energy began diversifying its rare-earth and specialty-materials sourcing away from China roughly five years ago, building alliances in Japan and elsewhere, precisely to avoid the kind of single-point dependency that can halt a delivery even when the component is a small share of a product’s value.

The disruption is reshaping how projects are sequenced. Engineering and construction firms report that the traditional design-build model is inverting under supply chain pressure: rather than design a plant and then procure the equipment, developers now secure scarce turbines and long-lead components first and engineer around whatever they can get. Engineers from Burns & McDonnell and 1898 & Co., its consulting arm, described clients securing equipment early and advancing project development around those procurement decisions—a reversal that complicates planning when a project’s start depends on a turbine slot that may not open until late in the decade. The insiders noted the squeeze is steering some buyers toward reciprocating engines and other technologies that can be sourced faster than large frame turbines.

Even the bottlenecks that aren’t about turbines deserve more attention than they get, Wilmot argued. “Labor costs have come up significantly over the past several years and [are] materially impacting project costs across all technologies. I don’t think this is getting enough air time,” he said.

The Workforce Math Doesn’t Add Up

Bruch’s worry about who will operate and service the new fleet is the leading edge of a constraint that may prove harder to engineer around than any turbine slot. The capital flooding into the sector has to be executed by people who, by several accounts, do not exist in sufficient numbers.

Tom Keefe, who leads Deloitte’s Power and Utilities practice, put the scale in perspective. Power and utilities spent nearly $215 billion in capital expenditure (CAPEX) last year, he said, and the industry is on track for $1.4 trillion through 2030—“ballpark numbers, double what it was historically running.” Executing that build requires far more engineers, electricians, and skilled trades, “but almost nobody is doubling their back office,” Keefe noted. Accounting and finance departments facing twice the transaction volume with the same headcount will have to lean on AI and robotic process automation to keep up. “It’s got to get done,” he said, but seemingly not by hiring proportionally.

His colleague Christian Grant, a partner on Deloitte’s consulting side, argued that the talent gap—not a desire to cut costs—is what will actually drive automation into utility operations. “We’re not producing all those engineers that are in demand, and all those electricians,” Grant said. The question becomes “how can I get one electrician to do the job and the effectiveness of, like, four others” when the other three cannot be recruited. He sees advanced analytics and automation maturing first in the roles utilities simply cannot fill, such as in control rooms and line work—jobs that have been hard to staff for years.

Michelle Fay, who leads the Energy Providers practice at Guidehouse, flagged the same shortfall as the concern she hears least discussed relative to its importance. “When you think about the number of skilled and knowledgeable people that are retiring, and then the demand for all of this increased investment,” she said, “there’s not enough people to do that work.” The squeeze extends beyond utilities’ own rolls to the contractors and vendors they depend on to build—a constraint Fay expects to surface as real capacity limits on how fast some utilities can execute their plans. Closing the gap, she argued, will require workforce planning that spans the contractor base and partnerships with universities and other institutions to train people the industry cannot develop on its own.

Fay also pointed to a more immediate lever that recurs across these conversations: wringing more out of what already exists while the new build catches up. Optimizing the current system to free up capacity, leaning on demand response, and treating gas as a bridge are interim moves utilities are reaching for, she said, alongside nuclear uprates and grid-enhancing technologies that squeeze more from existing assets than a greenfield plant could deliver on the same timeline.

Weather Moves to the Supply Side

The 58 GW that improved this summer’s outlook is dominated by resources whose output depends on conditions outside any operator’s control. Solar photovoltaic (PV) led the additions at 30.5 GW of nameplate capacity, with battery storage contributing 14.7 GW of on-peak capability. Those resources perform well across more hours of a summer day than they do in winter, which is part of why reserves improved—but their weather dependence shifts a familiar variable to an unfamiliar place in the equation.

“More than half of this year’s 58 GW in new capacity is solar,” Vaden noted, “and the report calls out a lack of snowpack in the West this winter [that] may strain hydro facilities in the WECC [Western Electricity Coordinating Council]. Weather has always played an important part on the demand side of the power equation, but it now plays an increasingly important role on the supply side. That’s a new normal and becomes more critical by 2030 if data center demand shows up as expected.”

NERC’s assessment bears him out. Almost the entire Western Interconnection is in drought or at heightened risk of it, and Washington’s snow-water equivalent sat at 52% of normal as of April 1, when snowpack typically peaks. The Northwest, which draws 55% of its generation from hydropower, is the only area NERC’s probabilistic modeling flagged with measurable expected unserved energy this summer, with the hour of greatest risk falling around 6 p.m. in early September—well after the solar that pads midday reserves has begun to fade. It is a precise illustration of Vaden’s point: the resource mix that looks comfortable at the peak demand hour can thin out at the real risk hour.

The Affordability Squeeze

While engineers track megawatts, the political center of gravity has shifted to price. Capacity prices have hit the cap in PJM, double-digit rate increases are on the table across multiple jurisdictions, and the question of how much of the buildout’s cost should fall on data centers has moved into mainstream politics.

For utilities, the old habit of treating reliability, affordability, and sustainability as separate goals no longer holds. “You can’t do that anymore,” said Calvin Butler, CEO of Exelon and EEI’s outgoing chair (Figure 3). “They all have to be done at once and balanced with intention.” Butler was blunt about where the pressure lands: when prices rise for reasons largely outside a utility’s control, “the utilities tend to be an easy point of inflection,” the visible line item a frustrated customer can point to. He was equally blunt that regulatory frameworks are not keeping pace. Asked whether policy is moving fast enough, he answered, “Absolutely not,” and warned of an institutional reflex to wait for a crisis before acting: “You need a crisis or something existential to happen, then everyone will hurry up and act.” Operating within PJM, he said, means watching a market “many would argue right now is dysfunctional,” with 65 million customers exposed to the consequences.

|

|

3. David Campbell, chairman and CEO of Evergy; Calvin Butler, president and CEO of Exelon; and Drew Maloney, president and CEO of Edison Electric Institute (EEI) on stage at EEI 2026. Source: POWER |

Latif Nurani, senior regulatory counsel at the American Public Power Association (APPA), pointed to a driver of rising bills that gets less attention than capacity markets: transmission. It has been “one of the fastest-growing components of customer bills for over a decade,” he said, but most of that spending has gone toward local asset management—replacing aging equipment and hardening the grid—rather than large regional expansions. That is now changing. Regional transmission organizations have approved multi-billion-dollar expansion plans necessary to maintain reliability and connect new resources, and when those costs begin reaching customers, Nurani warned, “the rate impacts could far exceed anything we have seen over the past decade.” Permitting reform, in his view, is one of the most effective levers to contain the damage. He knows of projects “doubling or even tripling in cost after prolonged delays in interconnection queues or extended litigation,” costs that ultimately flow to ratepayers. Streamlining approvals while preserving environmental review and community input, Nurani argued, could meaningfully lower the price of new infrastructure.

The question of who pays for the largest new loads remains unsettled. Many data center developers have signed the President’s Ratepayer Protection Pledge, Nurani noted, but “implementing those concepts will be easier said than done.”

S&P Global Energy’s analysts expect the affordability story to get worse before it improves. “Retail electricity prices are likely to continue to outpace inflation over the next 12–18 months,” Vaden and Giuffre said jointly, predicting that genuine fixes from industry and regulators will eventually outweigh the well-intended policies that make the problem worse—but that “things may get messy in the short run.” Wilmot reported hearing far more interest in squeezing existing infrastructure harder before building new. Among the solutions he cited were dynamic line rating, reconductoring, advanced power flow control, demand response, and distributed energy resource management.

One emerging mechanism points toward a constructive outcome. Fay highlighted utilities partnering with hyperscalers in ways that let the data center investment defray costs for everyone else on the system. She pointed to NIPSCO, which is lowering rates in northern Indiana on the strength of an Amazon Web Services–backed generation arrangement—an alternative funding path that supports much-needed investment “without having to go to the ratepayers in order to fund it.” If that model proliferates, it could blunt the political backlash that has otherwise made data centers a lightning rod.

The Scramble for Scale

Affordability and speed-to-power are also driving a wave of consolidation. The proposed NextEra-Dominion merger, with an enterprise value of $420 billion, the largest in the sector’s history, is being read across the industry as the opening move in a broader reordering. “The pending NextEra-Dominion merger really elevates the importance of scale in meeting data centers’ speed-to-power requirements and ratepayers’ affordability concerns,” Vaden said. “I think we’ll see more power M&A [merger and acquisition] announcements as the big look to get bigger.”

Deal volume is already running well ahead of historical norms. Keefe counted 157 deals in the industry in 2025, worth roughly $142 billion and accounting for 144 GW of generation changing hands—about 10% of all U.S. nameplate capacity. The first quarter of 2026 alone saw 44 deals worth $68 billion. “It’s just really accelerating,” he said, and he sees little to slow it: utilities need capital to fund a CAPEX program that has roughly doubled, but they cannot simply lever up without breaking the credit ratings and dividend commitments that keep Wall Street satisfied. Merging is one way to get a bigger balance sheet that can absorb more risk. Private equity is “massively involved and investing really across the board,” Keefe added, drawn by the same growth-and-returns logic pulling capital toward new generation.

Bill Drolet, executive director of M&A at The Post Oak Group, frames the NextEra-Dominion deal as the visible expression of a deeper thesis: that the physical power layer beneath the AI boom is where the bottleneck—and the investment opportunity—now sits. “What you see in the press about AI changing the world is all the application layers that are going to affect us day to day, but without the power, we don’t have that,” he said. “The application layers are moving faster than the power is being generated.” Investors chasing the application layer for returns, in his view, are “really behind owning the physical layer underneath”—the generation that consolidation is now racing to lock up. He expects “a bunch” of deals like NextEra-Dominion over the following six months, with capital coming from “the BlackRocks of the world” and the big banks hunting growth. “When there’s a gold rush, you want to be selling shovels,” he said.

Drolet pointed to Entergy as a logical next target: the utility is building power plants for Meta’s massive AI data center complex in Louisiana (Figure 4), a buildout he expects to more than double the New Orleans market’s current needs. He does not rule out hyperscalers acquiring a utility outright—“I do think that is a possibility,” he said, given the “dry powder” the largest tech companies command—though he questioned whether regulators would allow it.

|

|

4. Meta announced it will build a $10 billion artificial intelligence data center in northeast Louisiana, a transformational investment that puts this picturesque rural community on the leading edge of a global digital revolution. Courtesy: Louisiana Economic Development |

Grant is more skeptical that direct ownership becomes a lasting strategy. The behind-the-meter generation hyperscalers are building, he argued, is about solving a near-term problem, not entering the power business. He drew an analogy to the buildout of America’s industrial base, when a manufacturer might erect a power plant next to a new factory and then promptly offer it to the local utility. “I don’t want to be a power company—you guys run it,” is how he characterized the mindset. “I just needed the input.” Short-term plays to secure power, in his view, should not be mistaken for long-term integration. Keefe agreed that most hyperscalers would rather connect to the grid and let someone else run the generation; they turn to behind-the-meter solutions only when the grid cannot deliver fast enough.

What Carries to 2030

The mid-year picture, then, is of a system that bought itself time and knows it. The reprieve is real: reserves are healthier, no region is in the danger zone, and the relentless demand curve bent, at least for a season. But nearly everyone responsible for keeping the lights on reads the calm as conditional.

Not everyone reads it the same way, though. Nurani is more confident than most that his members will navigate the next several years intact. Public power utilities are accountable directly to the communities they serve, he argued, and that accountability “drives disciplined planning and better visibility into real—rather than speculative—load growth.” Municipals plan resource portfolios years ahead and build in contingencies, he said, which is why community-owned systems have weathered past stress with fewer interruptions—a reminder that how an institution is governed shapes how well it plans, even when the macro pressures are identical.

The deferred data center load is expected to arrive within two to three years, and meeting it will require firm capacity that is hard to finance, equipment that is hard to procure, and a workforce that does not yet exist at scale. Half the new supply is weather-dependent at the precise moment weather is becoming a supply-side risk rather than only a demand-side one. Affordability has hardened into a political constraint that will shape what gets built and how fast. And the consolidation underway suggests the industry itself believes only scale can square speed against price.

NERC’s calmer assessment is best understood not as the end of the capacity crunch but as a measure of how much depends on the next three years going right. The grid did not solve its problem this summer. It earned a chance to.

—Aaron Larson is POWER’s executive editor.