Courtesy: U.S. Coast Guard

Over the last decade, the United States experienced significant improvements in exploration and production technologies that led to a dramatic growth in gas supply, improvements in end-use technology, and improvements in natural gas vehicle (NGV) technology that now make them ready for prime time. We at the American Public Gas Association (APGA) believe natural gas is not just a bridge fuel—rather it is the cornerstone for America’s prosperity in the 21st century.

In 2011, the U.S. consumed approximately 67 Bcf/d of natural gas. Today, 18 applications for export of liquefied natural gas (LNG) have been filed at the Department of Energy (DOE), totaling 27.4 Bcf/d, and more are sure to follow. If exportation does occur, almost 50% of our current daily natural gas consumption may be shipped abroad, and the American economy and consumers will surely feel the resulting negative impacts.

Natural gas is the best fuel America has and is clean, abundant and affordable. Even Main Street is now beginning to realize that America’s natural gas industry will need to play a key role to move our country through and out of this economically difficult time. The question is—What should America do with our newfound abundance of natural gas?

APGA’s Perspective

Early in 2011, APGA leaders wrestled with the issue of LNG exports and concluded that U.S. policymakers must carefully consider and prioritize the use of domestic resources. Policies on our domestic resources should be implemented to encourage such use according to the national interest over both the short and long-terms.

As gasoline prices rise and the use of natural gas for transportation and electric generation increases, the U.S can take significant strides toward both energy independence and clean air. Additionally, these steps will help improve our economy by creating jobs and improving our national security.

However, such prioritization of domestic use is predicated upon access to affordable natural gas for both the short and long term. Therefore, APGA opposes the export of domestically produced natural gas, as it will increase the prices paid by U.S. consumers ranging from homeowners to large industrial enterprises, and sacrifice America’s best opportunity to reduce our dependence on foreign oil.

To preface our arguments opposing LNG exports, the following questions may help frame our perspective:

- Do we know how large the near- and mid-term growth in demand will be as our electric generation plants move away from coal to natural gas?

- Do we know how large the near- and mid-term growth in demand will be as our industrial loads return and industrial operations move to America to gain access to an abundant, reliable, and affordable gas supply?

- Do we know how large the near- and mid-term growth in demand will be if we move away from gasoline and diesel towards NGVs?

- Will producers be allowed to continue with hydraulic fracturing?

- What regulatory burdens and/or restrictions will be placed on producers by federal and/or state environmental agencies?

- What will happen to domestic natural gas prices when they become part of a global market?

- Should America move forward in a haphazard manner before these questions are answered?

APGA has four main reasons to oppose the export of LNG:

- The price impact on consumers

- The need to reduce our reliance on imported energy

- A recognition that there is a fast-growing domestic demand

- The unknowns regarding shale gas

Price Impact

First, U.S. consumers currently enjoy low natural gas prices that result from newly available supplies and a market that is largely limited to North America. According to a December 2011 study by IHS Global Insights, the emergence of shale gas has lowered U.S. consumers’ electricity costs by 10%. And, from 2012 to 2015, the study projects that the lower prices paid by Americans for electricity and natural gas will add $926 in disposable income to each consumer.

This effective increase in consumers’ disposable income is directly threatened by exports of LNG. Earlier this year, the U.S. Energy Information Administration (EIA) released a report that affirms increased prices as a result of the export of LNG. The EIA estimates price increases ranging from 3% to 9% for natural gas, 1% to 3% for electricity consumers, and a 54% increase in the price of natural gas at the wellhead. The EIA concluded that, under all of the cases and scenarios considered, increased LNG exports of domestically produced natural gas will lead to higher domestic natural gas prices. The debate is effectively over: Exports of natural gas will increase prices for U.S. consumers. The only questions now are how quickly and by how much will the price increase?

Energy Independence

APGA’s second reason for opposition is that LNG exports undermine and actually run counter to our national goal to reduce dependence on foreign energy. If we replace current diesel- and gasoline-powered fleets with natural gas vehicles (and support infrastructure), we can significantly reduce our dependence on foreign oil, thereby enhancing U.S. security and strategic interests as well as reducing our trade deficit (approximately 60% of our trade deficit in 2011 was from imported oil according to the Consumer Energy Alliance).

Substantial resources are being expended today to put natural gas infrastructure in place around the country. However, to accomplish the goal of moving towards energy independence, supplies of natural gas in the United States must remain stable, abundant, and affordable. The export of large quantities of domestic gas threatens our ability to obtain this goal.

Surging Domestic Demand

The third reason for APGA’s opposition is based on the fact that there is already mounting domestic consumer demand for natural gas. In addition to the growing popularity of NGV’s, we are now also seeing more dramatic increases in gas usage in both the industrial and electric generation sectors.

Abundant and affordable natural gas is bringing the industrial sector back to America. For instance, shale gas and shale gas liquids have been vital job creators in the chemical manufacturing sector. In April of 2012, Dow announced that it was building a $1.7 billion ethylene plant in Texas that would create 35,000 new jobs. At the macro level, shale gas supported 1 million jobs in 2010 and is projected to grow to 1.5 million jobs by 2015, according to a June 2012 IHS Global Insights study.

Moreover, a report earlier this year from the U.S. National Association of Manufacturers said affordable supplies of natural gas could help its members reduce their expenses by as much as $11.6 billion a year through to 2025, and allow them to create 1 million new jobs.

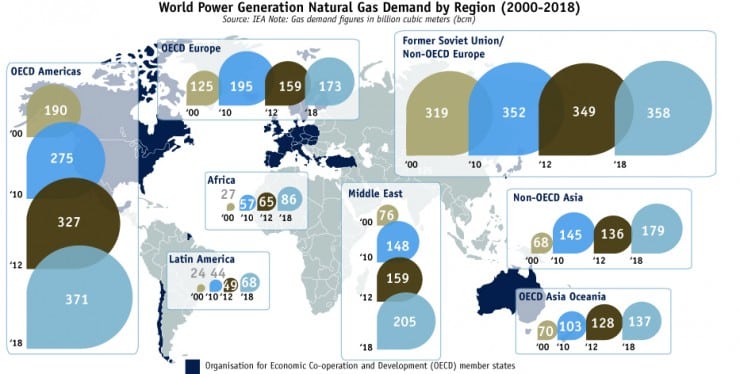

Natural gas in the electric generation sector is also on the rise as we are shifting away from coal faster than anticipated. Actual electric generation from coal was 52% in 2000 while natural gas’ share was 16%. In April of this year, natural gas and coal both provided 33% of actual electric generation. This shift is predominantly driven by natural gas’ environmental attributes, abundance, and affordability.

How will this impact the future demand side pressure on natural gas? There are approximately 21 GW of announced coal plant retirements over the next five years. Between 50 GW and 80 GW, which represents about 15% to 20% of the existing U.S. coal-fired generation fleet, will be retired over the next 15 years.

How does this growth in gas demand convert into Bcf/d? Depending on the heat rate of the facility, 75 GW of coal-fired generation retirements replaced by natural gas generation may result in about 12 to 15 Bcf/d of new natural gas demand. With the current flow of natural gas in the U.S. of about 67 Bcf/d, an additional 20% demand will require a significant increase in both methane production and pipeline capacity. Would a reasonable person conclude that a 20% increase in daily demand would impact price? Would the impact on price be in a particular direction?

An Uncertain Future

Finally, APGA opposes LNG exports because of several unknowns that could further exacerbate the impacts of LNG export. These unknowns are: supply and future regulation of hydraulic fracturing, if not an outright moratorium.

In regards to supply, the EIA now estimates that the “unproved technically recoverable resource of shale gas for the United States is 482 trillion cubic feet.” This number is substantially below the previous estimate of 827 tcf. This reduction “largely reflects a decrease in the estimate for the Marcellus shale, from 410 trillion cubic feet to 141 trillion cubic feet,” a reduction of over 65%. This extreme volatility and uncertainly in resource estimates should give policymakers and the general public pause. It would be highly unwise to export large quantities of natural gas because lower supply could make the price impacts on consumers even more significant. The amount of gas we have is an enormously important consideration to take when prioritizing how our nation actually puts it to use.

The second unknown includes the impacts of potential legislation and regulation on shale production. Congress ordered the EPA to study water quality, water use, and waste fluid disposal issues associated with hydraulic fracturing. In addition, the EPA announced it would initiate proposed rulemakings to regulate the disposal of waste fluid produced by hydraulic fracturing, and to require disclosure of the chemical substances and mixtures used as fracturing fluid. In addition to the federal oversight, states are also looking at regulating hydraulic fracturing. What type of impact will these regulations have on natural gas prices for our domestic consumers?

In light of these matters, and rejecting a “free market approach” no matter the costs to our recovery, economy, and energy security, the APGA board of directors made a deliberate decision to oppose the export of domestic natural gas. The confluence of inevitable price increases for consumers, a lost opportunity to reduce our dependence on foreign oil, significant new domestic demand, questions about supply, and regulatory uncertainty, makes exporting our natural gas resources a reckless course. It is incumbent upon our policymakers to ensure that domestic natural gas remains plentiful and affordable for U.S. consumers.

At this critical time in our history, APGA submits that the wise policy choice by our elected officials is to limit natural gas exports so that we may realistically pursue the greater goals of energy independence, clean air, and a revitalized domestic manufacturing sector. Those who argue that this matter is not an either-or situation are wagering our long-term national well being on short-term profits.

—Bert Kalisch is president and CEO of the American Public Gas Association