|

| Courtesy: iStockphoto |

The availability and low price of natural gas enticed many U.S. utilities to fuel switch on a grand scale in 2012. Increased demand has put upward pressure on prices, moving coal back to the top of the dispatch order in some regions. Expect the price momentum to shift often in 2013.

An unexpected boom in gas production as a result of advances in hydraulic fracturing, combined with an unusually mild 2011–2012 winter, sent gas inventories spiraling to record high levels. The traditional withdrawal season ended two weeks early, with storage levels touching bottom at an all-time high of 2,369 Bcf. The result was a crash in gas prices, which spent most of April 2012 below $2.00/MMBtu. Henry Hub spot prices finally hit a floor of $1.82/MMBtu on April 20.

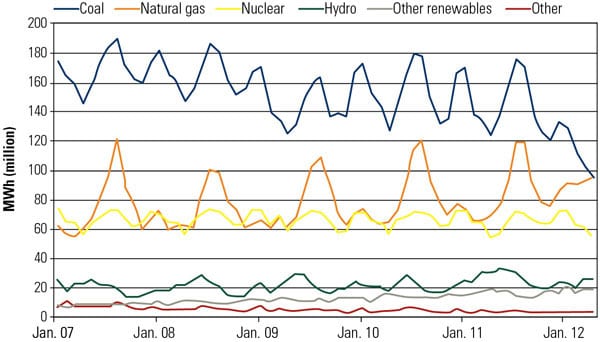

Awash in a sea of cheap gas—which was now substantially cheaper on a MWh basis than coal—plant owners across the country threw standard dispatch plans out the window and pushed open the throttles on their gas turbines. Coal-fired generation collapsed, while gas-fired power surged. In May, for the first time ever, gas power reached parity with coal power at about 32% each. Coal plants that had long been dispatched first as the core of baseload capacity saw themselves sidelined as peakers or idled altogether. Meanwhile, many combined cycle plants that had seen capacity factors around 30% were running at 80% or higher.

|

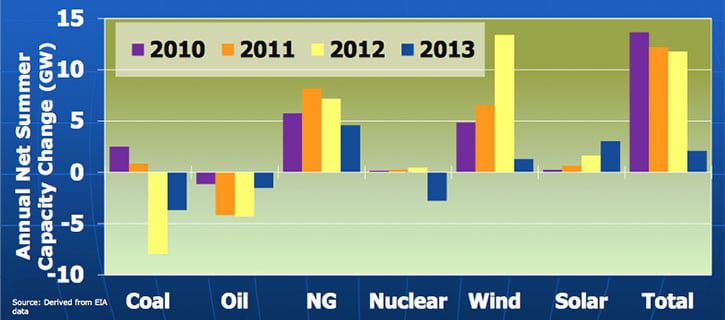

| 1. Give and take. Natural gas consumption for electric power generation is expected to fall this year, giving up some of the gains achieved in 2012, when historically low prices drove coal-to-gas switching across much of the Eastern Interconnect. Source: EIA, “Short-Term Energy Outlook,” November 2012. |

What Goes Up Must Come Down

The U.S. Energy Information Administration (EIA) projects that gas prices will average $3.49/MMBtu in 2013, which means they likely will spend some time above $4.00. Many analysts project even higher prices. Speaking at the LDC Canada Gas Forum in Toronto in November, Scott Speaker of J.P. Morgan projected an average price of $4.25/MMBtu for 2013, with continued growth beyond that. “I see relatively good production, but high demand going forward,” he said.

The $4 threshold is more than just psychological, as it represents the general point at which—with the higher transport costs for coal factored in—coal regains a cost advantage over gas. The EIA projects gas power burn to fall 11.2% during 2013, and some industry sources report that the gas-to-coal switchback has already begun.

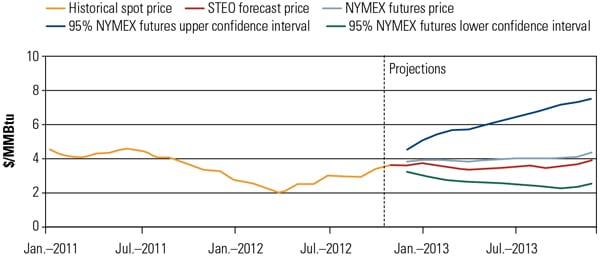

The drop in power burn is not expected to reduce pressure on gas prices, however, as residential, commercial, and industrial demand is projected to surge, leaving overall demand essentially unchanged for 2013. Heating demand as a result of more normal winter weather, combined with growth in industrial consumption, should make up for the decreased power burn (Figure 2).

|

| 2. Prices expected to rise. Natural gas demand may remain flat for 2013, but price forecasts agree (the blue and green lines bracket the 95% confidence zone) that the price is moving up. The only question is how fast. Source: EIA, “Short-Term Energy Outlook,” November 2012. |

“Between early, thus far, sustained colder-than-normal temperatures and nuclear outrages and maintenance,” gas market analyst Jay Levine told POWER in November, “natural gas continues to remain buoyant and stronger than many anticipated.”

The “fracking” rush, like most booms, badly overshot its target in 2011–2012, leaving thousands of drilled but uncompleted gas wells waiting for a resurgence in prices. Gas at $2/MMBtu is a money-loser for the drillers, but should prices begin edging above $4/MMBtu, returns on investment become attractive enough that it is likely some of these wells will return to production.

In addition, the shale oil boom continues unabated, with associated gas accounting for an increasing percentage of the current production. While a shocking amount of this gas is being flared because of a lack of gathering infrastructure—in North Dakota, almost 30% of it was flared last year—this will change as several key pipelines in shale fields come online. Likewise, continued strong demand for natural gas liquids has kept production levels high despite a big drop in the gas rig count.

Finally, despite the record power burn, gas inventories remain at record levels, having ended the 2012 injection season just below 4,000 Bcf—an unthinkable amount not so long ago.

Political Uncertainties Remain

The first political uncertainty is a series of proposed rules on hydraulic fracturing and gas production. In April, the Environmental Protection Agency (EPA) issued its final rule on emissions from fracked wells. While the rule is fairly clear, the level of enforcement, and the commensurate costs, are not. Estimates have ranged from essentially negligible to hundreds of thousands of dollars per well. If the higher estimates prove correct, this could put a brake on future production.

Another set of rules covering the entire fracking process on federal lands is currently pending from the Bureau of Land Management. With the final form uncertain, the impact is as well, but these too are likely to increase production costs to some degree.

The other major political uncertainty concerns liquefied natural gas (LNG) exports. In mid-2012, shortly after Cheniere’s Sabine Pass export project received Department of Energy (DOE) approval, the Obama administration put all other applications on hold until after the November elections, ostensibly to allow further study of the effects on the domestic energy market.

LNG exports are facing substantial opposition from a variety of quarters, creating some odd bedfellows: Environmental groups such as the Sierra Club are joining forces with petrochemical companies and several natural gas advocacy groups in an attempt to block exports.

With upwards of 20 Bcf/day of proposed projects currently awaiting DOE approval or in the process of application, a few observers have taken a “sky is falling” view of the market, seeing huge amounts of domestic gas heading overseas. More levelheaded analysts have noted that, no matter the political outcome, the U.S. is unlikely to see much beyond 6 Bcf/day of exports, particularly given the cost to build LNG export facilities.

Waiting for Demand Growth

Another big uncertainty is demand for electricity generation. In 2012, shares of total U.S. electricity generation averaged 30.6% for gas and 37.2% for coal. Higher gas prices—while coal prices remain flat—are projected by the EIA to reset that breakdown to more traditional levels in 2013, back to 27.2% for gas and 40.1% for coal.

But there are signs that any such rebound is likely to be temporary. With estimates of impending coal plant retirements ranging anywhere from 40 GW to over 80 GW by 2015, the ability of the coal fleet to shoulder significant price-induced gas-to-coal switching may be limited. This range of retirements equates to around 4 to 8 Bcf/day in gas demand.

Spurred by lower prices, the need for greater dispatch flexibility, and favorable regulatory treatment, strong development of gas-fired generation is likely to continue. Meanwhile, even advanced “clean coal” plants face significant developmental roadblocks.

Finally, the pace of the current economic recovery remains unclear. While the U.S. is seeing modest growth, there are clouds over Europe and Asia. Another downturn would limit electricity demand and likely keep gas power burn below 2012 levels for some time. Stronger growth, on the other hand, may exert upward pressure on gas prices.

Scenario Options for 2013

The first possible scenario takes the Obama administration at its “all-of-the-above” word and assumes the regulatory impact on gas remains light, while the U.S. economy continues its slow recovery. In this case, the large supply overhang is able to meet increased demand outside the power sector, keeping prices steady at around $3.50 to $4.00, in line with current projections. In the event gas demand exceeds projections, producers will have sufficient time to resume exploration.

If, on the other hand, President Obama’s reelection heralds new regulatory pressure on fossil fuels—both gas and coal—gas production may be handicapped just as significant coal generation begins to go offline. This would mean higher-than-expected demand, possibly more than the current supply overhang can meet, leading to short-term supply constraints and consequent price spikes.

— Thomas W. Overton, JD is POWER’s gas technology editor. Follow Tom on Twitter @thomas_overton.