Source: EIA

It’s election season (thankfully, not for much longer), and that means we’ve been hearing a lot of rhetoric out of Washington that is not necessarily what it seems, but is rather one calculated attempt or another to affect the results. Though partisans on both sides would have you believe otherwise, market fundamentals have far more influence on the energy world than politics. That’s why, for example, domestic oil production declined during the ostensibly pro-oil Bush administration and has risen under the allegedly anti-oil Obama administration. Most industry veterans know to take a lot of this stuff with a healthy dose of salt.

Some things, though, deserve some comment because they threaten to distort sound policy decisions. One of these is the increasingly shrill complaining about the Obama administration’s supposed “war on coal.”

On September 18, coal producer Alpha Natural Resources announced that it was cutting production by 16 million tons, laying off 1,200 miners, and closing eight mines in Virginia, West Virginia, and Pennsylvania. Though Alpha’s statement spread the blame around, citing a poor market and unfavorable regulatory environment, conservative media outlets and Republican politicians—starting with Mitt Romney—seized on the news as dramatic evidence that President Obama was out to destroy the coal industry. (Virginia and Pennsylvania, it must be noted here, are key swing states in this year’s presidential election.) The following week, the GOP-led House of Representatives, on a mostly party-line vote, passed the largely symbolic “Stop the War on Coal Act” as its final act before heading out on its pre-election recess (“largely symbolic,” because the Democrat-controlled Senate has no plans to take it up).

The root of this issue, of course, is an array of impending regulations on power plant emissions, most of which fall most heavily on coal plants. Without going into the alphabet soup of regulation, which needs a regulatory lawyer to unravel, it’s worth pointing out two things:

-

The rules represent real, substantial future expenses for owners of coal plants.

-

The rules, in general, exempt existing plants, don’t take effect for years, and/or are currently suspended as a result of court action.

There’s no question that plant owners are going to need to spend a lot of money to comply with the new regulations, and that some older plants will be shut down because upgrades are not cost effective. It’s also clear that the impact of these rules is often badly overstated and that the plant closures and chaos in the coal business are not always what they may seem to be if you listen to general media reports.

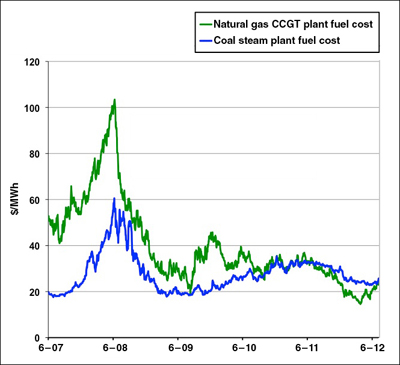

Remember that market fundamentals are usually much more of a factor than politics. And what are those fundamentals? Let’s start with a chart that appeared in the August GAS POWER, which tracks coal and gas prices for power generation since 2007:

1. Gas has been cheaper than coal on a MWh basis since mid-2011. Source: EIA, NYMEX.

Look closely at what happens in mid-2011. Since last June, coal has been more expensive than natural gas on a MWh basis. That’s why there’s been a dramatic shift toward gas-fired power over the past year—it’s simply cheaper. This year, coal plants have been running at reduced capacity, coal inventories have piled up, and plant owners have been looking for ways to slow or even halt coal deliveries. That’s a bad situation for coal producers, but it has nothing to do with the Environmental Protection Agency (EPA).

The other thing to understand is there are two different coal markets: thermal and metallurgical. The latter—high-quality bituminous coal used in steel production—isn’t affected by the new rules, but that market hasn’t been any better. The reason is something entirely different: the slowdown in China’s economy. China is the world’s largest steel producer and the largest consumer of metallurgical coal. So when the Chinese are making less steel, as is the case right now, coal producers feel the pinch.

Said the Wall Street Journal recently:

While many have blamed the downturn in the U.S. coal industry on cheap natural gas supplanting coal and tougher environmental regulations, the slide in metallurgical coal demand has been equally devastating. Coal companies were caught flat-footed after ramping up production last year with the expectation that steep prices would cover their rising costs, despite coal’s past cyclicality. Instead, demand in China began to falter just as Australian metallurgical coal production—interrupted by floods last year—surged back into the market.

These shifts have caused the price of metallurgical coal to collapse, falling almost 25% from its peak earlier this year. And who just happens to be the U.S.’s largest metallurgical coal producer?

Well … it’s none other than Alpha Natural Resources, which just had to make substantial cutbacks in its operations because of reduced demand for its coal. On this point, at least, the investing community hasn’t been fooled by the political rhetoric, advising investors to stay away from companies like Alpha whose main source of revenue is metallurgical coal.

And Patriot Coal, whose bankruptcy in July caused a similar round of hand-wringing? Also a big metallurgical coal producer.

As Bloomberg explained in an August 29 report, several major U.S. coal producers, including Alpha, made bad bets on the price of metallurgical coal last year and are now paying the price for it. Since metallurgical coal typically sells for two to three times more than Central and Northern Appalachian thermal coal (and at least 10 times more than Powder River Basin coal), it’s a cash cow when the price is high—but a big drop can be potentially fatal to a company’s bottom line.

The incessant complaining about the “war on coal” has produced some other embarrassing events. Last summer, Dallas-based Luminant Energy, Texas’s largest electricity producer, began issuing dire warnings that the Cross-State Air Pollution Rule (CSAPR) was going to force it to shutter two coal-fired units at its Monticello plant, removing 1,200 MW from an already badly overstretched grid.

So when, in August, the Fifth Circuit Court of Appeals threw out the CSAPR, GOP politicians and pundits in Texas rejoiced over having saved the plants. Yet within a week, Luminant had to make a rather awkward announcement: It had to idle the plants anyway because the price of electricity, largely set by gas-fired power in Texas, had fallen so low that these coal-fired plants couldn’t compete. And it conceded, when pressed by the Texas media, that the shutdowns had nothing to do with its spat with the EPA.

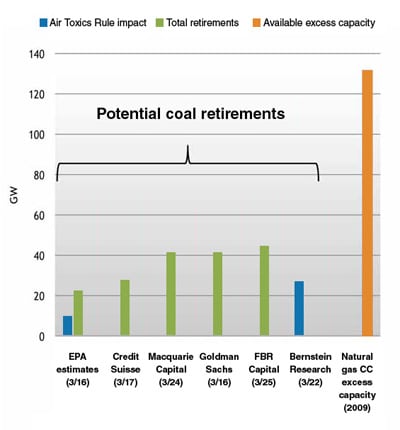

Even some normally reliable news outfits have been tripped up by the hype. In early October, the Brattle Group updated its 2010 report on coal plant retirements, predicting between 59 GW and 77 GW of retirements over the next five years due to a variety of factors, about 25 GW more than they had originally projected. Unfortunately, rather than read the report closely, Reuters, The Christian Science Monitor (CSM), and several other sources rushed forward, trumpeting the study as more evidence of the “war on coal.” After cooler heads (like POWERnews) pointed out that the study actually attributed the increase to low gas prices and further stated: “gas prices are a much more significant influence on retirements than the stringency of the remaining regulations,” the hasty articles were all withdrawn (the CSM link, for example, now redirects here.]

The Brattle Group isn’t the only outfit taking a dispassionate look at this issue and finding that the rhetoric has run far ahead of reality. A peer-reviewed study published in The Electricity Journal in July found that “recent downward adjustments in natural gas prices and electricity demand projections have a substantially larger impact on electricity prices and generation mix than do the new EPA regulations.” Quantitatively, the authors estimated that the market-driven decline in coal was five to six times greater than that attributable to the regulations.

Closer to home, my colleague David Wagman adds some interesting perspective on this issue in the October POWER. After analyzing data on coal plants in the 27 states covered by the CSAPR, some illuminating trends emerged:

| Updated analysis. Key characteristics of coal-fired power plants in CSAPR and non-CSAPR states, including those slated for retirement. Sources: POWER and Burns & McDonnell |

||||

| Median MW | Median year built | Median capacity factor | Median heat rate (Btu/kWh) | |

| CSAPR state | ||||

| Unit has scrubber | 444 | 1974 | 67.7% | 10,066 |

| Unit has FGD | 411 | 1974 | 67.4% | 10,090 |

| Unit has SCR | 570.5 | 1973 | 68.4% | 10,045 |

| Non-CSAPR state | ||||

| Unit has scrubber | 383 | 1978 | 76.1% | 10,497 |

| Unit has FGD | 203 | 1968 | 64.0% | 10,355 |

| Unit has SCR | 241 | 1969 | 86.2% | 9,894 |

| CSAPR state, units for retirement | ||||

| All units for retirement | 125 | 1955 | 49.3% | 10,786 |

| Unit has scrubber | 117.5 | 1957 | 35.8% | 10,844 |

| Unit has FGD | 133 | 1957 | 42.0% | 10,807 |

| Unit has SCR | 212 | 1961 | 62.3% | 10,092 |

| Notes: CSAPR = Cross-State Air Pollution Rule, FGD = flue gas desulfurization, SCR = selective catalytic reduction. | ||||

Of those plants currently slated for retirement, he says,

The data show these units have a median nameplate capacity of 125 MW, a median in-service date of 1955, a median capacity factor of less than 50%, and a median heat rate in excess of 10,750 Btu/kWh. Some of these units have environmental controls, but even here the units are small, old, less likely to be dispatched, and inefficient.

Need further proof? The coal companies themselves, when speaking to investors, are considerably less pessimistic about the situation. Said John Eaves, president and CEO of Arch Coal (the country’s second largest producer), in their third-quarter earnings call on Oct. 26:

We estimate that 45 GW of coal generating capacity could be retired by 2018, but these at-risk plants are the smallest and least efficient in the coal fleet and are already running at very low levels. Those at-risk plants likely will consume just 40 million tons of coal in 2012, down from 75 million tons consumed in 2010. Thus, any incremental negative impact from these potential coal plant retirements is likely to be modest. More importantly, the lost consumption could be offset by increasing utilization at the remaining 280 GW of installed coal-fueled capacity.

It’s also worth noting here that Arch, unlike the companies mentioned above, is focused primarily on thermal coal—less than 10% of its reserves are metallurgical coal.

The takeaway from this, from where I’m sitting? If there are casualties in the “war on coal” right now, most of them are plants that would have been shut down anyway for purely economic reasons.

None of this is to suggest that things would be no different if all the offending rules were repealed. But it’s also clear that the chatter surrounding this issue is heavily divorced from reality, and mostly intended to score political points in an election season.

As always, the first place to look is market fundamentals. Most of what you hear otherwise is just Macbeth’s “sound and fury,” signifying nothing.

—Thomas W. Overton, JD is POWER’s gas technology editor. Follow Tom on Twitter @thomas_overton.