The conventional wisdom about uranium fuel—that demand is steady, supplies are adequate, and prices will be stable—is wrong, according to three experts at an online seminar sponsored by The Energy Daily earlier this month.

Leading off the May session, Raffi Babikian, vice president at Toronto-based Dundee Securities Corp., laid out the consistent message at the publication’s “Uranium Supply and Demand” conference. Babikian claimed a “consistent underestimation of nuclear generation going forward.” China leads the pack with its latest estimate of 75 GW of new nuclear construction by 2020. As of May 2009, he noted, there have been approximately 276 new nuclear units proposed. China’s target has jumped from 45 to 75 GW in a year.

Can New Mines Make Up the Difference?

On the supply side, said Babikian, the conventional wisdom overestimates supply. Resource plays, including new supplies from Australia—where the Ranger mine is presumed to increase supply and new mines are expected—are probably smoke and mirrors, according to Babikian. “Many proposed mines have not achieved expected output (or have been shelved completely),” he said.

Dustin Garrow, marketing manager for Paladin Energy Ltd., a relatively new, publicly traded Canadian uranium producer, echoed Babikian’s views. Paladin is developing and operating mines in Africa (Namibia and Zambia) and Australia. Regardless of worldwide economic conditions, said Garrow, demand for nuclear fuel “won’t drop,” because nukes are the ultimate baseload generation: They run 24/7/365, flat out.

The focus of the new nuclear build, said Garrow, is China and India, which will put pressure on global supply. As demand increases, some of the uranium fuel supply chains will tighten. He explains that the U.S.-Russia program to take Russian highly enriched weapons-grade uranium and blend it down to reactor-grade fuel (some U.S. observers call this “uranium impoverishment”) will end in 2013 and Russia has made it clear that it has no intention of resuming the program. That program has generated 24 million pounds of reactor fuel annually, according to Garrow.

Garrow’s bottom line? Demand for uranium will go up steadily; supply won’t match the demand.

Bleak Supply Outlook

That’s also the view of Jerry Grandey, CEO of Canada’s Cameco Corp., one of the granddaddies of world uranium producers. He cited the demand expected by new reactors in China, India, Japan, and Korea, and the difficulties of developing new uranium supplies. Cameco’s 10-year outlook, said Grandey, is for a worldwide supply deficit of approximately 400 million pounds of U3O8 by 2018.

That supply deficit, says Grandey, points to the need to develop new mines. But mine development is difficult and expensive. Prices will have to rise before developers will commit capital to new mines.

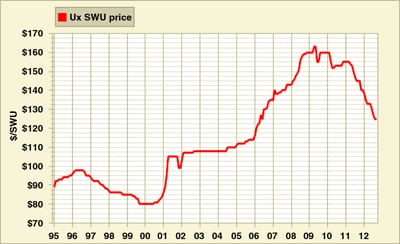

In sum, all three speakers at the online conference agreed: Demand is growing faster than anticipated; supply is going to be stretched to keep pace. What does this mean? Higher uranium prices ahead.

It would have been worthwhile had there been a speaker available to challenge the assertions of the panel members, all of whom appear to have a vested interest in high uranium prices. Are China and India’s aspirations for new nukes realistic and sustainable? Is it possible that, given higher prices, new supplies will become available, including increased production at Australia’s Ranger mine?

As is the case with most supply chain issues, the answers will be in the marketplace, not in learned seminars.

—Kennedy Maize is executive editor of MANAGING POWER.