If the planned expansion of nuclear power materializes, it will amplify demands on a nuclear fuel supply system that is only beginning to recover from decades of neglect. Uranium production, which supplies about 70% of estimated reactor requirements, has increased only 5% since 2005, despite higher prices. However, enrichment — the process of increasing the concentration of uranium-235 atoms in uranium fuel so that it can drive modern reactors — is expanding more rapidly due to technological advances and growth.

The question is: Who will control these expanding markets for uranium and enrichment? Increasingly, enrichment plants will have the ability to take control away from utilities and uranium producers.

Fuel Competition: Uranium vs. Enrichment

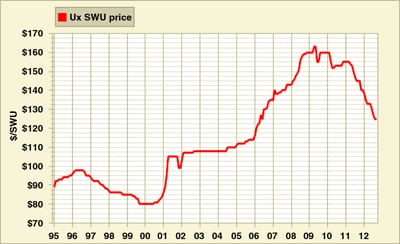

Uranium and enrichment are substitutes for each other in the production of nuclear fuel. Mined uranium has only 7 out of 1,000 atoms that are U-235. The enrichment process uses separative work units (SWU) to increase the concentration of U-235 atoms. When uranium prices were low, it was economic to recover only about half of these essential atoms, using fewer SWU and more uranium. However, when uranium prices began to rise a few years ago, it became economic to recover more — using more SWU and less uranium. The potential range of substitution can be as much as 30%.

Utilities typically purchase uranium and enrichment separately. In the past, free contractual flexibilities allowed utilities to decide on the economically optimum mix of uranium and enrichment to make fuel, based on relative prices, by picking the "tails assay," or fraction of U-235 atoms thrown away in the enrichment process. These flexibilities caused uranium and enrichment suppliers to endure punishing swings in demand and prices.

Today, uranium and enrichment suppliers limit such contractual flexibilities. For enrichment companies, this means writing contracts with fixed tails assays. Utilities must deliver a specific quantity of uranium to the enrichment plant in exchange for a specific amount of fuel according to a set "transaction" tails assay that may be quite different from the "operating" tails assay set by enrichment plants.

An Economic Balancing Act

By fixing contractual tails assays at relatively high levels, but building in flexibility to lower actual operating tails assay, enrichers can "underfeed" (use less uranium than utilities deliver while still producing the same amount of fuel) and resell uranium into the market. Given enough capacity and flexibility in operations, enrichers will exercise considerable control over uranium supply, demand, and price.

By returning uranium to the market through substitution of enrichment for uranium, net demand for uranium from primary production can be reduced — essentially turning enrichment plants into uranium mines and potentially lowering prices for uranium.

Enrichers will continue to underfeed as long as the revenue from sales of uranium exceeds the loss of revenue from selling the SWU used to obtain the uranium. As long as enrichers have the operational flexibility to underfeed, uranium and enrichment prices will tend to come into equilibrium with each other. If uranium prices rise, underfeeding will increase because it is more profitable for enrichers to use enrichment capacity to minimize uranium use in production of fuel and resell uranium into the market than to sell SWU. This, of course, will reduce uranium prices, restoring price equilibrium.

Conversely, if enrichment prices fall, it may make sense to divert enrichment services to uranium sales. This might happen, for instance, if enrichment capacity overexpands. Enrichers can turn a surplus in enrichment into a surplus of uranium, raising prices for enrichment but lowering those for uranium.

(Elsewhere, I have analyzed the economic tradeoffs between uranium and enrichment, given the likely expansion of enrichment capacity compared with the expansion of uranium supply.)

In 2007, when uranium prices spiked, enrichers might have increased revenue by about 45% by underfeeding and selling uranium, an effect only partly limited by contractual and operational inflexibilities. In fact, the rise in uranium prices did result in an increase in enrichment prices by more than 40%. To reach a new equilibrium, given higher enrichment prices, long-term uranium prices fell by 30%.

The Enrichment Sector’s Growing Control

Today, the rapid expansion of enrichment capacity and rigid new contract terms appear likely to give enrichment companies substantial control over both enrichment and uranium markets. Uranium mining companies cannot exercise such technical flexibility and thus may have to yield market power to enrichment companies. Of course, this is a compelling argument for vertical integration. AREVA already has both uranium mining and enrichment operations, and Cameco has invested in GE-Hitachi’s Global Laser Enrichment project, whose technical and economic feasibility may be proven by next year.

The era when nuclear utilities had the contractual flexibility to minimize costs for fuel appears to be ending, with control over uranium and enrichment price equilibrium shifting to others, who may not have the same interests. There are major implications for uranium miners as well as utilities, both of whom will have to find new strategies for dealing with technological change and growth in the enrichment sector.

—Thomas L. Neff, PhD (tlneff@mit.edu) works at the Center for International Studies at the Massachusetts Institute of Technology in Cambridge, Mass.