Offshore wind capacity is slated to surge to more than 234 GW by 2030—a remarkable boost when compared to the current 29.1 GW that was installed worldwide at the end of 2019, the Global Wind Energy Council (GWEC) said in an August-released analysis of the sector.

In the second edition of its Global Offshore Wind Report, GWEC pegs its optimistic projections on policy ambitions, declining technology costs, and international commitments to decarbonization, as well as growth in emerging markets and a build out of floating technology. It also noted about 6.1 GW was added globally last year—which made 2019 the “best year in history” for the global offshore wind industry. About 6.6 GW is expected to be installed in 2020, despite the COVID pandemic’s impact on the wind industry’s supply chains. “Offshore wind has been less impacted by the pandemic compared to other energy sectors,” and the sector is “being seen as a major contributor to post-COVID economic recovery by governments around the world,” GWEC said.

According to Alastair Dutton, chair of GWEC’s Global Offshore Wind Task Force, offshore wind now makes up a 10% share of total global wind installations—up from just 1% only 10 years ago. Over the next 10 years, GWEC expects accelerated growth in traditional markets—notably in the UK, Germany, Denmark, Netherlands, Belgium, and China—and emerging markets, which include Taiwan, the U.S. Atlantic Coast, Japan, South Korea, and Vietnam, he said. New markets are also in the “preparation phase,” he said. Examples include Brazil, Mexico, India, Sri Lanka, and Australia.

Floating Offshore Wind Coming of Age

Meanwhile, the sector is gearing up for a “coming of age” of floating offshore wind technology by 2030, which promises to triple the technical potential for offshore wind across the world. “Initially the key markets are France, Japan, South Korea, Scotland, Norway, Portugal, Spain and U.S. Pacific Coast. Once commercial scale projects are established and costs come down many other locations will come into play, for example South Africa, Canada, Philippines and many island states,” Dutton said.

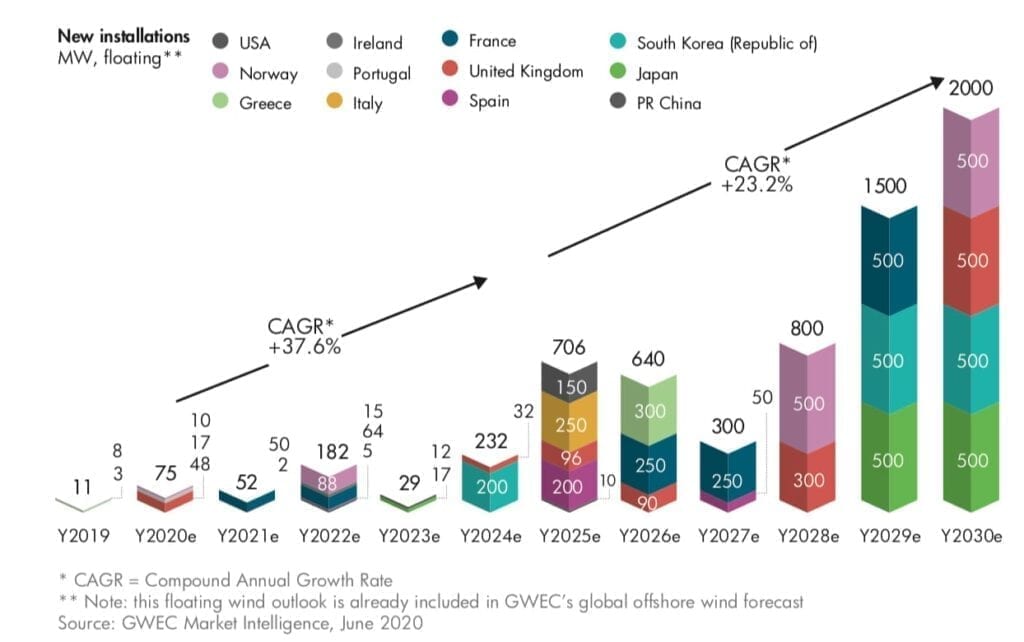

Since the world’s first megawatt-scale floating offshore wind turbine was grid-connected by Equinor in Norway in 2009, only about 65.7 MW of floating offshore wind capacity has been installed globally at the end of 2019—and the subsection has yet to reach “full commercialization.” About 32 MW is so far located in the UK, 19 MW in Japan, 10.4 MW in Portugal, 2.3 MW in Norway, and 2 MW in France. Still, “After a decade of development, floating offshore wind is no longer simply an R&D [research and development] area. With more oil majors such as Shell and TOTAL starting to focus on floating wind, this sub-section of offshore wind is ready to progress quickly to full commercialisation,” GWEC said.

So far, GWEC’s 2030 floating offshore wind forecast ranges from 3 GW to nearly 19 GW, “depending on how quickly [levelized cost of energy (LCOE)] can be brought down to an affordable level and its adoption by new markets,” it said. GWEC Market Intelligence predicts 6.2 GW of floating wind may be built by 2030, based on the existing project pipeline.

However, more than 90% of this volume won’t likely come online until the latter half of the decade, “when large-scale floating wind projects tendered through auctions are expected to be installed,” it said. The floating offshore wind sector faces a number of formidable challenges and barriers, GWEC noted. These include high costs—almost double the cost of fixed-bottom offshore wind energy—a lack of standardization and industrialization, and a lack of “tailor-made” supportive policy frameworks.

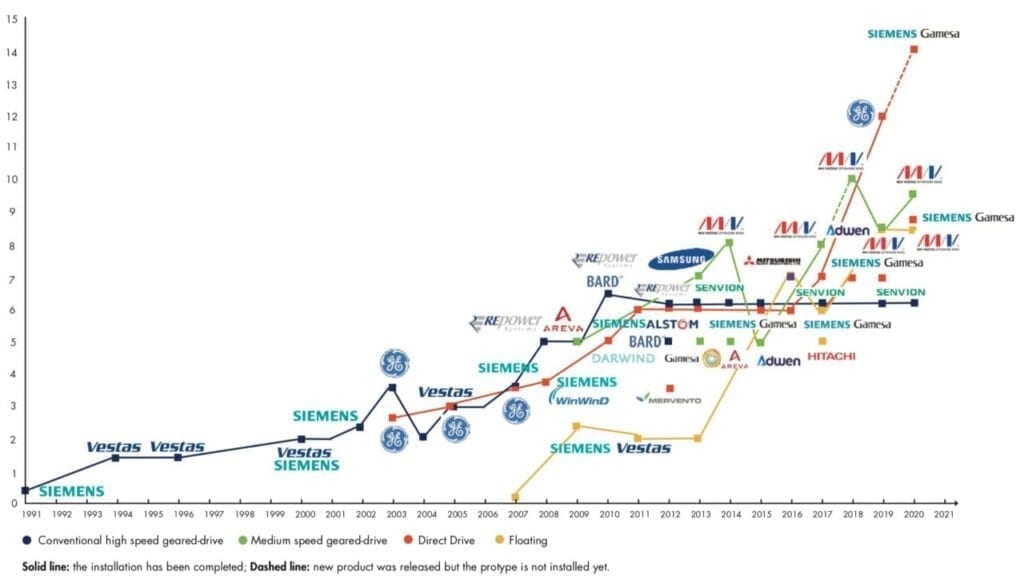

Offshore wind LCOE, notably, has tumbled in recent years, owing to installations of larger turbines. “When the bigger offshore turbine is released with a higher nameplate capacity, rotor diameter and tower height, the technical capacity factors are higher, which in turn increases the annual energy production (AEP),” the organization explained. “Although larger turbines per unit are more costly than smaller ones, it saves the CAPEX [capital expenditures] for foundations, cables and installation as well as the OPEX [operational expenditures] due to lower [numbers of] turbine units.”

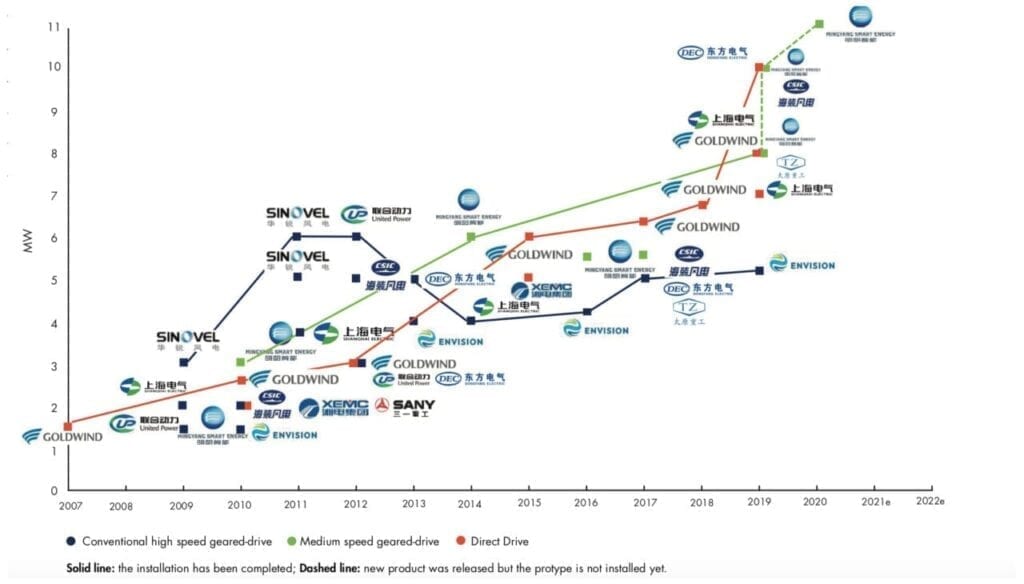

The Race for the Largest Wind Turbine

Examples of mammoth turbines being tested today include GE Renewable Energy’s 12-MW direct-drive (DD) Haliade X model, and Siemens Gamesa’s recently launched SG 14 222 DD model, which can reach 15 MW with Power Boost technology. While the SG 14 222 DD model is slated to be commercially available in 2024, GWEC’s offshore wind ambassador Henrik Stiesdal predicted in a recent webinar that the next generation of offshore turbine technology could probably be around 20 MW with a 275-meter (m) rotor diameter by 2030.

However, how much wind turbine size could grow will depend on a number of factors, such as “continued turbine technology innovations, drive-train optimization, alternative materials, regulatory barriers, and logistical constraints for both transportation and installation,” GWEC noted.

Offshore wind’s economics could also benefit by emerging power-to-x solutions, along with other general power sector trends, such as digitalization and widespread electrification. “Power-to-X is one of the most promising storage options for offshore wind that minimises waste and maximises efficiency by deploying stored power for a myriad of uses,” GWEC said.

The group said that stored electricity can be electrolyzed into hydrogen to be used as feedstock to produce bulk chemicals like methanol or ammonia for industrial processes or combined with captured CO2 to make carbon-neutral liquid fuels such as crude, gasoline, diesel, and aviation fuels. It can also generate heat through heat pumps or electric boilers for houses and factories.

Or it can be stored in underground formations like salt domes and fed back to the grid as needed. But while power-to-x has been shown to be technically feasible, the technology is “limited by the scale of projects, making it too expensive to be widely deployed at this stage.” However, the industry is primed to take the next step, “so it’s just a matter of ‘when,’ ” it said.

—Sonal Patel is a POWER senior associate editor.