This has been the year from hell for coal-fired power and the coal industry. If current projections hold, coal generation in 2020 will be 21% lower than last year and 62% lower than the 2007 peak. The coal share of the generating mix, which for decades hovered around 50%, will finish the year at 20%, the lowest on record. Coal production will be the lowest since 1964 and down by a quarter just from 2019.

The new year may bring relief. The U.S. Energy Information Administration’s (EIA’s) Short-Term Energy Outlook (STEO) projects that coal generation will recover most of its 2020 losses in 2021, bringing some stability to coal plant operators and coal miners. The key factor behind a coal power recovery is higher prices for natural gas, which indeed appear likely in 2021. Nonetheless, a coal recovery in 2021 is highly contingent on other dynamics. A close look illustrates how factors such as fuel inventories, capacity additions, and trends in electricity demand growth could mute the impact of higher gas prices. A review also shows how coal-fired power, once the bedrock of American power generation, has become dependent on factors—such as winter weather in northeast Asia and the price liquefied natural gas (LNG) commands in Europe—that once would have been considered arcane and irrelevant.

A Recovery in 2020?

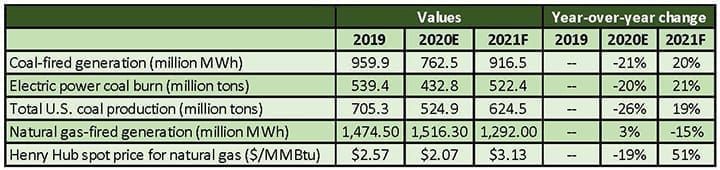

The EIA is currently projecting a turnaround for coal generation and coal consumption in 2021. As shown in Table 1, coal megawatt-hours and coal burn (tons) are expected to increase by about 20%, recovering most of the ground lost in 2020, while gas-fired generation drops by 15%. After accounting for other coal demand sectors and inventory changes, miners are expected to enjoy a 19% increase in production, a reprieve from the 2020 disaster.

This forecast pivots on a key factor—an expected increase of 51% in the market price of natural gas. The EIA expects the Henry Hub price for natural gas in 2021 to remain above $3.00 per MMBtu for the entire year, something that has not happened since 2014. The assumption is that high natural gas prices will lead generators away from gas and back to coal.

While the natural gas price is the key driver, the projected price increase is caused by the interaction of several factors:

- Reduced domestic natural gas production in response to low gas prices in 2020.

- Lower oil prices and resulting reduced oil output is expected to cut the supply of associated gas produced as a byproduct from some oil wells.

- The National Oceanic and Atmospheric Administration is predicting a colder winter than in 2019, which would boost space heating demand for gas.

- Robust and even record demand for LNG exports from the U.S.

The volume of LNG exports from the U.S. now plays a major role in domestic gas/coal competition. LNG trade is particularly important as a marginal draw on supply with an outsized impact on domestic gas prices. In 2015, LNG exports from the lower 48 states were zero. With the advent of ample fracked gas, net LNG exports are expected to reach 2.2 trillion cubic feet (Tcf) in 2020 and 3.1 Tcf in 2021. Demand for American LNG is projected to grow due to the El Nina effect causing a cold winter in Japan, Korea, and northern China. LNG prices have been increasing in Europe, drawing in more American cargos.

To put LNG volume in context, projected exports in 2021 will be equivalent to about 30% of the gas used for power generation. However, the level of exports is highly dependent on market prices in Asia and locations such as the Title Transfer Facility virtual trading point in the Netherlands. American gas prices, and the competitive balance between coal and natural gas in the domestic power market, have become part of an international energy market.

These factors are not expected to produce a domestic supply shortage, in part because of ample gas storage (which will be discussed further below), but they would result in tighter supplies and higher prices. But these factors are also contingent, most obviously on the weather, and their interactions are complex. While gas prices are almost certain to rise from 2020, which have been depressed by the COVID-19 recession, there is no consensus about 2021. In contrast to the EIA’s forecast of an average price at Henry Hub of $3.13 per MMBtu, the energy analysts at Deloitte and the brokerage house Stifel, for example, expect a 2021 average of about $2.70 per MMBtu. The following discussion illustrates the uncertainties in the gas price and coal power outlooks for 2021 and later.

Natural Gas Inventories

A key driver of gas prices is the amount of gas in storage. Gas inventories are built in the injection season (April to October) so that local distribution companies will have enough supply to meet winter demand (November to March). If a winter is severe and inventories are low at the end of the season, storage operators will need to buy large volumes of gas in the spring and summer to restore inventories, driving up prices. But a mild winter can result in an excess of gas in storage, driving down prices.

Gas inventories as of the first week in October were the largest ever for that period (3.8 Tcf of working gas) and before the end of the month may reach the highest level ever recorded—more than 4 Tcf. Storage levels nevertheless must reach normal levels by the end of the winter to avoid a spring gas price collapse. This will require an unusually large storage draw. The EIA currently projects a 2.1 Tcf drawdown from early October to the end of March. This would be the fourth largest on record and only 0.3 Tcf shy of being the second largest.

Several factors will determine the rate of inventory depletion during the upcoming winter, including demand from the power and industrial/commercial sectors, and the level of production. But the key factor will be the weather, which drives residential space heating demand and demand for American LNG. The expectation that the gas market will avoid a large storage overhang and low prices in 2021 is essentially a bet on cold winter weather in the U.S., and on weather and international gas prices yielding record U.S. LNG exports to Europe and Asia.

Power Prices and Capacity Additions

Higher natural gas prices have two benefits for coal generators. First, if gas is more expensive, coal-fired units are more likely to win the competition for hourly and daily dispatch. Second, higher cost gas will likely drive up wholesale power prices. Because coal units are relatively expensive to run (considering both variable and fixed operations and maintenance costs) higher power prices will benefit both the short-term dispatch and the longer-term economic viability of the plants.

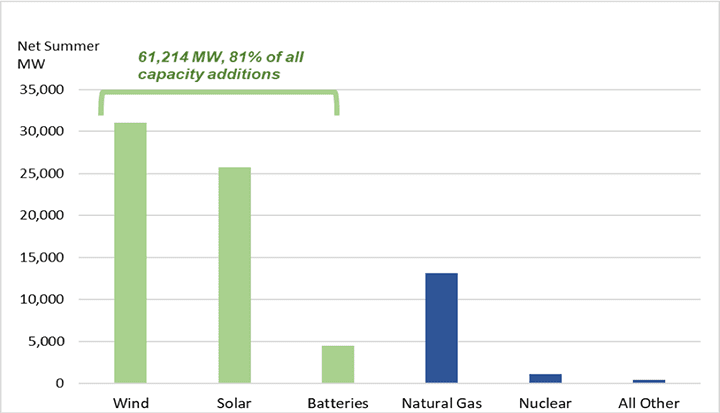

However, the penetration of solar and wind energy into the power market is a countervailing factor. Solar plants have zero variable costs and wind variable costs are low, which means that these plants will tend to lower wholesale prices, at least in the markets where they are concentrated. Batteries, by effectively expanding the scope of wind and solar utilization and reducing the need for gas-fired peakers, can have a similar effect. As shown in Figure 1, actual and planned additions of wind, solar, and battery capacity in 2020 and 2021 is enormous: a combined 61,214 MW accounting for 81% of new capacity. Other than the Vogtle 3 nuclear plant, most of the remaining capacity is new gas plants (13,117 MW), mainly combined cycles (9,042 MW) of presumably new and efficient design.

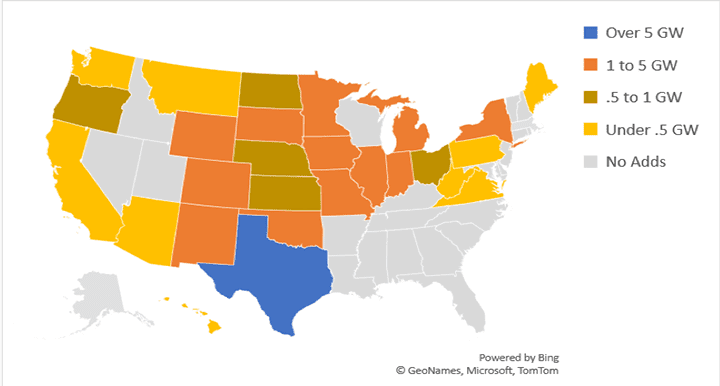

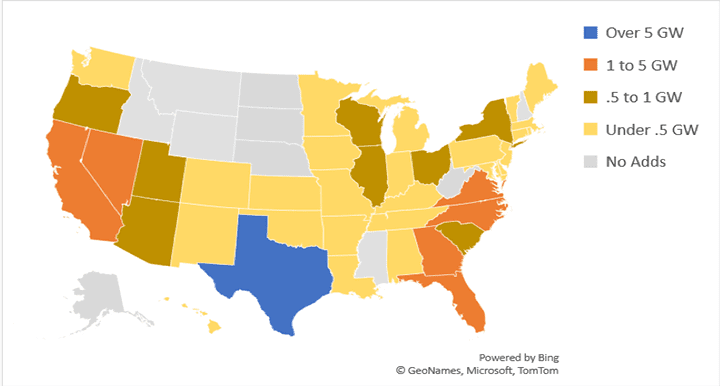

As illustrated in Figures 2 and 3, the solar and wind capacity additions are not a regional phenomenon but are widely distributed across the country. While this new capacity will not negate the effect of higher natural gas costs on wholesale power prices, it will likely have a moderating impact—to the detriment of coal plant operators.

Electricity Demand

In addition to natural gas price increases, growth in power demand could boost coal burn. Many coal units have been displaced from baseload to load-following service by gas-fired combined cycles and renewables. A significant increase in electricity demand would benefit coal plants that operate on the margin. But even with a recovery from the COVID recession, a big increase in electricity demand is not in the offering for 2021.

Electricity demand has become sticky, particularly since the 2008 Great Recession, due to a shift from heavy industry to services and the impact of energy efficiency measures. Even in a poor economy, demand reductions are limited, but so is the rebound when the economy recovers. The EIA’s current estimate is that real gross domestic product (GDP) will contract 4.1% in 2020, but electricity demand will drop by only 2.4%. This is the good news, but the flip side is that the projected recovery in 2021—a 3.5% increase in real GDP—will be accompanied by only a 0.5% jump in electricity demand. In essence, electricity demand growth will be almost nil in 2021 and will provide no lift to coal generators. This makes coal generators almost entirely dependent on natural gas price increases to drive growth in 2021.

Coal Mines and Coal Piles

For coal plants to survive, they must have a reliable, low-cost source of fuel. However, the coal industry is in free fall, with production down 55% since peaking in 2008. Miners have begun to spin-off free cash to shareholders—to the tune of $4 billion since 2017 for one group of four large coal producers—rather than investing in operations. Some miners are fleeing thermal coal for the more profitable coking coal market (such as Arch Resources, which recently dropped the word “Coal” from its name).

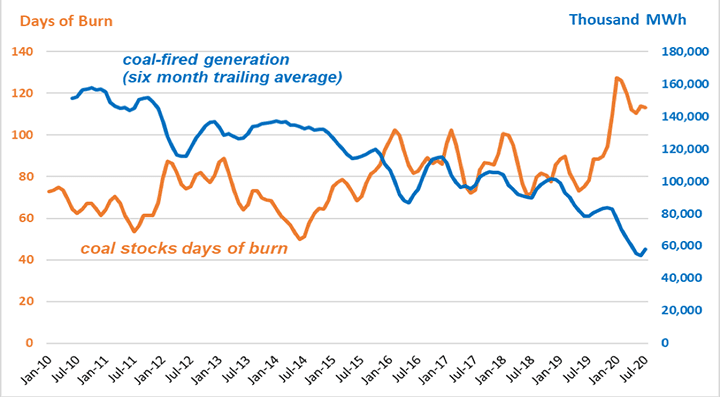

An increase in coal-fired generation that revived coal production could provide a welcome respite to miners. However, greater coal-fired generation may not yield a proportionate increase in coal production. The problem is that power plants are holding bloated coal inventories. Power plant coal stocks have usually fluctuated around 60 to 80 days of burn (the number of days of operations inventories would support if deliveries ceased) but ballooned to 113 days by July 2020 as coal burn dropped (Figure 4). Inventories consume working capital, so plants benefit by reducing coal stocks rather than buying more coal.

The EIA expects coal production to increase by 100 million tons in 2021, making up all the ground lost in 2020. But this forecast assumes a modest reduction of about 14 million tons in power plant coal inventories, which currently stand at 134 million tons (excluding lignite). This would leave an excessive 101 days of burn. Even if operators have contract limits on their freedom to cut deliveries, more aggressive stock burns are probable. And every ton of stock burn is likely one less ton of coal mined.

For example, an inventory drawdown to 70 rather than 101 days of burn would take another 37 million tons out of stocks, displacing more than a third of the projected growth in coal production. One more change to the 2021 scenario—say a 10% increase in coal-fired generation rather the forecasted 20%—would reduce power sector coal requirements by another 46 million tons, and the forecasted recovery in coal production becomes de minimis (Table 2). The upshot is another disastrous year for miners.

A Reckoning?

The prospects for coal-fired power in 2021 are highly uncertain. The EIA’s short-term outlook projects a modest recovery for coal. Morgan Stanley has warned that a cold winter could produce the tightest gas market in 10 years and send average natural gas prices in 2021 above $4 per MMBtu. This would almost certainly produce a big boost to coal-fired plants and miners. But other outcomes are entirely possible. The cold weather expected in northeast Asia might not develop, the winter could be milder than expected in the U.S., or LNG prices in Europe could be low. These and other outcomes would drive down gas and power prices, and abort the expected coal recovery. What then?

Given the pounding coal generators and miners have been taking for more than a decade, another year as historically bad or worse than 2020 could accelerate the cascade of coal plant retirements and the withering of coal production. In late September alone, Duke Energy released planning scenarios that include retiring up to 9,000 MW of coal plants and Vistra Corp. announced its intention to retire 6,800 MW of coal capacity by 2027. S&P Global Market Intelligence has warned that COVID-related electricity demand reductions have increased the possibility of accelerated coal plant retirements with concomitant financial stress on coal suppliers. These kinds of developments would likely lead to more miner bankruptcies and disinvestment, and more miners taking flight from thermal coal.

The winding-down of the coal power and mining sectors was never going to be pretty. In 2021, it could get ugly.

—Stan Kaplan (stankapl@gmail.com) has worked in the electricity and fuels areas since 1978, as a consultant, regulator, utility executive, and until retiring in 2018, a senior manager with the Department of Energy. He most recently taught a graduate class on energy policy at George Washington University.