The U.S. Department of Energy’s (DOE’s) final energy efficiency standards for distribution transformers appear to strike a compromise with industry, softening the agency’s stance on steel requirements for essential transformer components and extending compliance deadlines to five years.

The DOE’s final standards issued on April 4 seek to reduce losses in three types of distribution transformers—liquid-immersed, low-voltage dry-type (LVDT), and medium-voltage dry-type (MVDT)—through specific percentage-based energy efficiency standards. The agency said it determined these standards by evaluating trial standard levels (TSLs), agency-developed benchmarks that evaluate certain criteria, and efficiency levels (ELs) for each representative unit, which are based on an engineering analysis.

Compared to the DOE’s contentious January 2023 proposed rule, which would have required almost 90% of all transformers to feature amorphous steel cores, the final rule will allow 75% of distribution transformer cores to rely on grain-oriented electrical steel (GOES), which a primary core steel used in distribution transformers. That capacity can be manufactured domestically by the nation’s sole GOES manufacturer, Cleveland-Cliffs subsidiary AK Steel, at its facilities Butler Works in Pennsylvania and Zanesville Works in Ohio, U.S. Secretary of Energy Jennifer Granholm told reporters on April 3.

Granholm said the final standards will also support a 10% to 25% increase in the availability of amorphous metal (AM) core distribution transformers. The U.S. currently only has one AM manufacturer—Metglas, a subsidiary of Tokyo-headquartered Proterial, which operates a plant in Conway, South Carolina, with an annual domestic capacity of 45,000 tonnes—and relies on AM product imports from China.

The final rule also addresses another key industry sticking point: compliance timeframes. In contrast to the January 2023 proposed rule, which gave the industry just three years (until 2027) to make required changes to accommodate a surge in AM core production—including redesigning factories, establishing a dependable supply chain, hiring a workforce, and redesigning infrastructure—the final rule gives it five years, until 2029.

Granholm said the crucial change, which responded to “stakeholder feedback,” will allow transformer manufacturers to “maintain existing production capacity and choose how best to update their facilities and designs to meet customer needs.”

What Are the Final Standards?

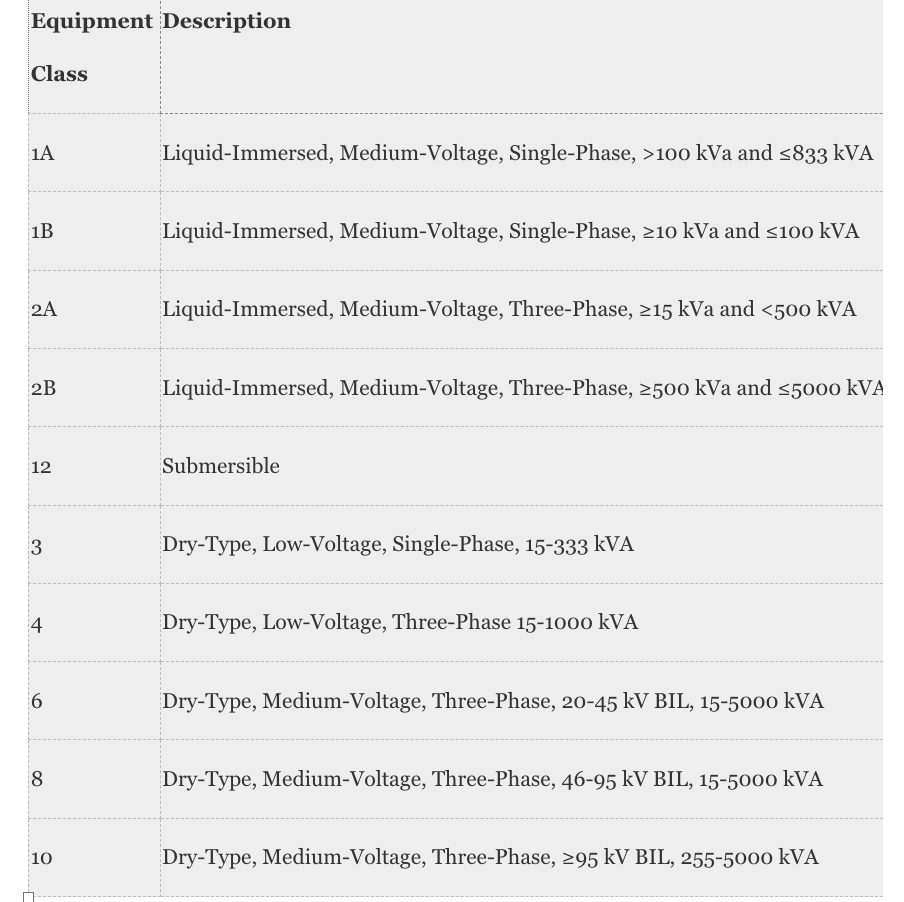

The final rule, as laid out in a 628-page document (and supported by an accompanying 1,116-page technical support document [TSD]), covers 10 equipment classes.

The rule relies on five trial standard levels (TSLs). TSLs are agency-developed benchmarks that group individual efficiency classes, based on the type of energy used, capacity, or other performance-related features. The use of “TSLs allows DOE to identify and consider manufacturer cost interactions between the equipment classes, to the extent that there are such interactions, and price elasticity of consumer purchasing decisions that may change when different standard levels are set,” the agency explained.

The final rules are summarized below:

A TSL 3 for Liquid-Immersed Distribution Transformers. That corresponds to a 5% reduction in losses for single-phase transformers ≤ 100 kVA and three-phase transformers 500 kVA. It also corresponds to a 20% reduction in losses for single-phase transformers ≥ 100 kVA and three-phase transformers ≤ 500 kVA.

A TSL 3 for LVDT Distribution Transformers. That corresponds to a 30% reduction in losses for single-phase LVDT distribution transformers and a 20% reduction in losses for three-phase LVDT transformers.

TSL 2 for MVDT Distribution Transformers. That corresponds to a 20% reduction in losses.

The DOE adopted its TSLs from the proposed rule—with the exception of the liquid-immersed TSL 3, which it modified to include equipment classes to ensure “capacity for amorphous ribbon increases driven by equipment classes 1A and 2A.” The determination “leaves a considerable portion of the market at efficiency levels where GOES remains cost competitive, equipment classes 1B and 2B,” the DOE reasoned. “Further, TSL 3 ensures that units that are more likely to have high currents (equipment class 2B) and units that are more likely to be overloaded (equipment class 1B), have additional flexibility in meeting efficiency standards to accommodate this consumer utility.”

The DOE said that to bring products into compliance with the final standards, the industry would incur total conversion costs of $187 million for liquid-immersed distribution transformers, $36.1 million for LVDT distribution transformers, and $5.7 million for MVDT distribution transformers. However, it said the final standards would save a “significant amount of energy.”

The agency noted it screened technology options in consultation with “interested parties” to determine if “they are practicable to manufacture, install, and service; would adversely affect product utility or availability; have adverse impacts on health and safety; or utilize proprietary technologies.”

In addition, it assessed the economic impacts on both consumers and manufacturers—including life-cycle cost savings for consumers and changes (in the net present value of the industry cash flow) for manufacturers. The final rule also considers national benefits and costs, projecting significant reductions in greenhouse gas emissions and associated climate and health benefits.

“DOE concludes that the standards adopted in this final rule represent the maximum improvement in energy efficiency that is technologically feasible and economically justified and would result in the significant conservation of energy,” the final rule says.

“Specifically, with regards to technological feasibility, products are already commercially available that either achieve these standard levels or utilize the technologies required to achieve these standard levels for all product classes covered by this proposal. As for economic justification, DOE’s analysis shows that the benefits of the standards exceed, to a great extent, the burdens of the standards.”

Addressing a Critical Supply Chain Crunch

The “burdens of the standards” have been a key sticking point for the power industry. Over the last three years, industry has repeatedly warned that distribution power transformers and large power transformers (LPTs) are in critical short supply. It has also urged the Biden administration to support the domestic production of electrical steel, warning that shortages are contributing to “significant and persistent” supply chain challenges.

According to a February 2024 study from the National Renewable Energy Laboratory (NREL) that leverages “extensive interviews” with transformer manufacturers and power trade groups, utilities are experiencing extended lead times for transformers of up to two years.

That’s “a fourfold increase on pre-2022 lead times,” the report notes. In addition, reporting prices have surged by as much as four to nine times in the past three years. “Current shortages have been attributed to pent-up post-pandemic demand; difficulty recruiting, training, and retaining a skilled workforce; component supply chain challenges; and materials shortages (grain-oriented electrical steel, aluminum, and copper),” it notes.

The American Public Power Association (APPA), a trade group that represents 2,000 U.S. community-owned electric utilities, in January told POWER lead times for distribution transformers appear to be growing. “We are hearing that lead times are around two years, with many members saying it’s more like three,” it said. “The delays cause extreme measures to be taken on our systems, including delaying or piecemealing replacement projects in our service territory, and it has caused delay or cancellation of expansion projects.”

Compared to power transformers, typically used in transmission networks of higher voltages and for step-up and step-down applications and are generally rated above 200 MVA, distribution transformers are used for lower-voltage distribution networks as a means of end-user connectivity. Distribution transformers have input voltages of 34.5 kV or less and output voltages of 600 V or less and have a capacity of 10 kVA to 2500 kVA for liquid-immersed units and 15 kVA to 2500 kVA for dry-type units.

NREL’s report suggests the majority of the nation’s distribution transformers are owned by municipal, cooperative, and investor-owned utilities across the U.S. It estimates—with caveats—a stock range of between 60 million to 80 million transformers with upwards of 3 TW of installed capacity. However, the age of the current stock is ambiguous, given that the individual utility stock is “highly heterogenous,” it says.

The DOE has suggested that the brunt of the new measures will be carried by manufacturers of the three categories of distribution transformers and purchasers of distribution transformers, which vary. In its TDS, the DOE highlighted it was keenly aware of the supply chain challenges across “all segments of the market.”

The shortages, it noted, “have largely been attributed to demand for distribution transformers, along with other electric grid related equipment, increasing substantially, as opposed to decreases to the supply. As a result, lead times for transformers have increased, and utility companies’ transformer inventories have been reduced.”

However, “manufacturers have been actively pursuing capacity expansions to meet the increased demand for distribution transformers” in response to the shortages, it said. Hitachi Energy, for example, a major manufacturer of submersible and pad-mounted liquid-immersed distribution transformers at a facility in Missouri recently announced a $10 million expansion to support increased production of larger distribution transformers to address renewable power and data center specifications. The company also produces pole-mounted liquid-immersed transformers in Quebec.

Electric Research and Manufacturing Cooperative, Inc (ERMCO), likewise, plans to expand production to an estimated 1 million transformers in 2024 at its facilities. Eaton, which produces three-phase transformers, single-phase transformers, and substation transformers at facilities in Wisconsin and Texas is looking to expand production capacity with $130 million in new investments. And Howard, which owns the largest transformer plant in the world in Missouri, recently broke ground on a facility that will specialize in the production of amorphous metal cores.

Promulgating a Fine Balance

Last week, Granholm underscored the complexity of promulgating a balanced final rule that considered social and environmental benefits while championing innovation and ensuring minimal burden to industry. The new rule, broader and more stringent than existing distribution transformer energy efficiency standards that were finalized in April 2013 (and which have applied to units manufactured after January 2016), will apply over 30 years, she noted.

But, the final rule’s apparent compromises still fall short of limits posed by a bill introduced in January by a bipartisan group of 12 U.S. Senators. As POWER reported, the bill was strongly backed by industry. It moves to restrict the Energy Secretary from finalizing “any rule” under which the efficiency level of a liquid-immersed type, LVDT type, or MVDT type transformer is greater than trial standard level 2 (TSL 2). In addition, the bill introduces a 10-year delay in implementing any regulations finalized by the Energy Secretary that affect liquid-immersed type transformers, LVDT, or MVDTs with efficiency levels of TSL 1 or TSL 2. However, no action has been taken on the bill after it was read twice and referred to the Senate Committee on Energy and Natural Resources in January.

Granholm last week suggested the final rule is necessary. “Currently, there are over 60 million distribution transformers mounted on utility poles and pads in neighborhoods nationwide, and a lot of these have been running for decades and just need to be replaced.” Meanwhile, she pointed to the recent NREL study, which estimates distribution transformer capacity may need to increase by 160% to 260% compared to 2021 to meet new energy demand driven by aging infrastructure and electrification.

“Ultimately, this improved final rule will save Americans over $14 billion in energy costs, and it’ll also slash nearly 8 million metric tons of carbon dioxide pollution,” she said. “And it will save American utilities and commercial industrial entities $824 million per year in electricity costs,” Finally, “it’s critical for long-term supply chain security for domestic manufacturing,” Granholm noted.

The Rule Still Makes a Case for Amorphous Transformers

The final rule notably also highlights a competitive slant related to the adoption of amorphous transformers, in addition to responding to industry concerns that they may exhibit performance deficiencies compared to GOES. “Adoption of amorphous metal transformers has significantly increased on a global scale in the past decade. In Canada, for example, over 90% of sales for liquid-immersed distribution transformers are estimated to utilize amorphous cores. China and India have similarly exhibited large upticks in amorphous transformer sales,” the rule says.

The rule maintains that amorphous core transformers “can be reasonably interchanged with GOES transformers without impacting performance.” But, it concedes that “for modest reductions in transformer losses (generally through EL2 for liquid immersed distribution transformers and EL 3 for dry-type distribution transformers), the difference in first cost is not substantial enough to warrant the considerable investment in amorphous core production that is needed to meet efficiency standards.”

Amorphous cores, however, may be a better choice for liquid-immersed transformers between EL2 and EL4 and EL3 and EL5 for dry-type distribution transformers if the “size and weight increase associated with GOES cores become substantial, and it generally become economically infeasible to continue producing GOES transformers unless consumers ignore product cost (e.g., if shortages have forced consumers to purchase any transformer they can access, regardless of product costs),” it says.

The new TSL 3, specifically, “is intended to reflect stakeholder concerns that standards requiring substantial amorphous core production are not economically justified,” it says. “Accordingly, DOE has determined that this TSL ensures that manufacturers will not have to scrap existing production equipment. Rather, manufacturers of distribution transformers, amorphous ribbon, and GOES steel can all focus on and invest in increased production.”

Overwhelming Initial Relief

For the most part, industry responses to the rule were overwhelmingly positive—though in the early days after the final rule’s publication, many trade groups noted they were still perusing the rule’s massive scope of documentation.

Scott Aaronson, senior vice president of Security & Preparedness at the Edison Electric Institute (EEI), in a statement sent to POWER on Friday, said the trade group that represents all U.S. investor-owned electric companies appreciated that the DOE “improvements that were responsive to concerns raised by electric companies, transformer manufacturers, steel producers, and numerous members of Congress.”

Aaronson said EEI shares the government’s goals “of enhancing energy efficiency, ensuring energy grid reliability and resilience, and growing domestic production of highly efficient transformers.” The revised rule marks a “positive step forward,” because it “helps to preserve the availability of both GOES and amorphous steel, and it provides the additional time needed to protect and expand domestic manufacturing capacity,” he noted. However, “electric companies today still are facing unprecedented lead times for transformers,” he said. “We will continue to work with all stakeholders to identify opportunities to shorten the lead times for these essential grid components, which are critical to efforts to meet growing electricity demand using resilient clean energy.”

Louis Finkel, senior vice president of government relations at the National Rural Electric Cooperative Association (NRECA), also stressed the need for a “stable distribution transformer supply chain,” noting it is “essential to maintaining reliability and meeting growing demand.” The final rule, he said, “is much improved over its proposal, which would have upended the entire market for distribution transformers at a time when manufacturers could not keep up with demand for this critical equipment.” It will provide “stability for most of the market while affording a more gradual shift toward tighter efficiency standards for transformers used to meet larger commercial and certain electrification loads,” he said.

The APPA, in a statement, also lauded the DOE for listening to industry stakeholders. “Electric utilities continue to struggle to source and obtain distribution transformers to properly maintain their systems,” it noted. “In relaxing the materials standards and extending the implementation timeline in its final rule, DOE has demonstrated that it has listened to industry stakeholders and understands the challenge before us.”

The starkest criticism of the measure, perhaps, came from Metglas CEO Rob Reed, who has worked to dispel misinformation about amorphous steel. He said the DOE’s final rule “is a missed opportunity” for U.S.-based manufacturers and for a stronger U.S.-based supply chain. “While we are still reviewing the details of the final rule, we know that a 5-year delay effectively makes the U.S. a dumping ground for cheap electrical steel, eliminates any opportunity to re-shore U.S. jobs, and makes the U.S. electrical grid even more reliant on foreign-sourced electrical steel from countries like China,” he said.

“Additionally, the vast majority of transformers will not be built to a higher efficiency standard,” Reed predicted. “The DOE had enough information from stakeholders on how they could structure a rule that would eliminate all foreign steel imports, protect jobs in Ohio and Pennsylvania, grow jobs in South Carolina, lower the cost of power to every hard-working American in the U.S., reduce greenhouse gasses, and chose not to.” Reed said Metglas will share more once its full review of the rule is complete.

—Sonal Patel is a POWER senior editor (@sonalcpatel, @POWERmagazine).