Southeast Asia offers rich renewable sector opportunities, recently exemplified by Chevron’s multibillion-dollar sale of its Indonesian and Philippines geothermal projects, and the purchase of Equis Energy for $5 billion. However, industry players and their lawyers face several challenges in developing a responsive and bankable legal regime for renewable projects.

Renewable Technologies in the Region

Hydropower and geothermal projects have historically dominated in Southeast Asia. Thailand, Laos, Cambodia, and Vietnam have developed a series of bankable Mekong region hydropower projects, to the point where the multi-country Mekong River Commission was formed to address growing concerns around riparian usage. Myanmar, with 100 GW of potential hydropower capacity, is the likely next frontier. Indonesia and the Philippines have used their abundant (and still mostly under-exploited) geothermal reserves to develop major power and steam projects.

Outside these technologies, the region has an increasing interest in intermittent power. The plummeting price of solar panels, partly driven by Chinese price competition, has led to a greater appreciation of the solar resource in the region (Thailand being a key example) and the potential returns to be derived from solar and wind projects. The other technology of significant interest is biomass, given the region’s abundant agri-business sector.

Macro Factors Affecting a Renewable-Friendly Legal Regime

At a high level, a number of factors should support a regional renewables drive, including low electrification levels, a growing appreciation of the environmental impact of fossil fuel independent power producers (IPPs) and the increasing difficulties a number of banks face in financing them, and a growing recognition of the depth and breadth of renewable resources in the region.

However, Southeast Asia also has a history of fossil fuel dependence, legal frameworks that cater to these as the primary fuel source, and a strong (and potentially competing) current focus on liquefied natural gas-to-power projects. In addition to these factors, the region faces the twin challenges of price competitiveness and off-taker/country risks.

Price Competitiveness

Southeast Asia needs, above all else, cheap and reliable electricity to bridge the electrification gap. Increased electrification at an overall cheaper price is a recognised regional vote winner and provides a powerful structural incentive for conventional IPPs. Renewable projects are unlikely to benefit from the sort of sophisticated price preference or renewable credit mechanisms that have characterised the European market. Offtakers in Southeast Asia have a limited ability to pass on renewable price hikes to their consumers.

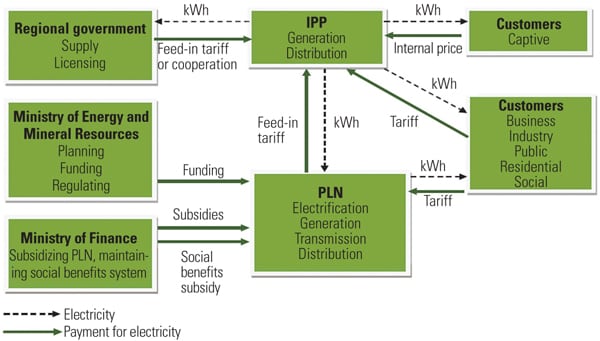

Indonesia provided an interesting example of this in 2017. Having previously successfully developed large-scale hydro and geothermal IPPs using conventional legal agreements (such as geothermal concessions modeled on oil and gas production sharing contracts), Indonesia was also developing smaller renewable projects through regulated feed-in tariffs. The government then passed a regulation in early 2017, which essentially capped the tariff for any renewable project at either 85% or 100% of the relevant region’s average electricity supply cost. The regulation has been softened since but still operates to push renewable projects to more remote areas where they can compete with high-cost fuel like diesel, and makes them uncompetitive in areas like Java where they compete with low-cost, abundant coal. This has chilled renewable investment but makes economic and political sense for the government. Indonesia is the clearest example, but this tension generally is a feature of the entire region.

Offtaker and Country Risks

Renewable energy projects (outside of the specific earlier examples) are more likely to be pioneer projects in Southeast Asia compared to conventional IPPs, and will have to deal with the same power sector challenges as their conventional competitors. The challenges include:

■ Restrictions on foreign ownership of IPPs or supporting services.

■ Tariffs denominated in local currency without always having bankable exchange rate or currency availability protection.

■ Newly formed offtakers (such as Electric Power Generation Enterprise in Myanmar) or offtakers dependent on government support (for example, Perusahaan Listrik Negara in Indonesia), and a reluctance to provide government guarantees.

■ Long lead times and uncertainty associated with land acquisition.

■ Multiple, difficult to predict regulatory changes.

Governments in Southeast Asia clearly want to develop renewable projects in principle and understand the wider benefits of the technologies. However, in certain cases the legal regime, including pricing and government support, would need significant overhaul to properly incentivize a surge in renewable development across the board. In the absence of this, the onus will be on developers, financiers, and their lawyers to maximize realistic opportunities and seek to develop creative and robust structures within existing constraints. ■

—Sean Prior is a counsel and Benjamin Thompson is a partner in the Singapore office of Mayer Brown JSM.