Many consumer magazines make their annual forecasts at this time of year on a variety of topics, such as politics or celebrity shenanigans. The prognostications, though seldom correct, are entertaining but not to be taken seriously. POWER’s purpose here is to gauge where we as an industry have positioned ourselves for future growth, to define the characteristics of that growth in generation resources, and to suggest a few key indicators to watch during 2007. We always strive to give readers the best data available. In this case, we’ll also give you our opinions, with a reminder that your own careful consideration of the data should guide your decisions.

The power industry’s spectrum of interests is wide and its information needs divergent. In preparing this 2007 industry forecast, we chose to explore a few hot topics that have seized center stage in the debate over America’s energy future. We delve into the details of these debates in every issue of POWER. But in this article we take a "helicopter view," to define the direction and speed of progress on a front—and to comment on whether both are appropriate.

I don’t expect every reader to agree with our studied perceptions of the industry. If you have a different perspective, we want to hear from you. Make your case with facts and statistics, and we’ll publish the best comments in a future issue. Remember, this industry is unique for its users’ expectations (instant gratification with a flip of a switch), the inability to store the manufactured product, and the industry’s reality-based stance on issues shaping short- and long-term national energy policy.

The future is now

The Edison Electric Institute (EEI) has made the industry’s growth priorities, and the obstacles to them, abundantly clear:

- Strengthen and expand the delivery system (with 12,500 miles of new transmission by 2014) to lessen congestion costs and meet reliability requirements and market realities.

- Build more than 50 GW of new supply by 2014 (and 347 GW by 2025) to meet growing demand, which is expected to increase 2% annually until then.

- Promote energy conservation.

- Cover environmental mandates ($50 billion worth for air emissions alone by 2025).

Speed of response lagging need for change. Transmission and distribution (T&D) upgrades happen slowly. T&D system constraints are slowly being unraveled, but action on major improvements had to wait for the August 8, 2006, release of the DOE’s National Electric Transmission Congestion Study, mandated by the Energy Policy Act (EPAct) of 2005. The study provides analysis of generation and transmission capacity across the U.S. and identifies critical areas that need attention to meet growing demand.

"Completion of the National Electric Transmission Congestion Study is an important step on the path to modernizing our nation’s aging electric power infrastructure and is a crucial step toward realizing President Bush’s goal of a modern, more efficient electric power delivery system," Energy Secretary Samuel Bodman said. "I am confident the Department’s actions will help facilitate the infrastructure growth necessary to meet the demands of our growing economy."

The report identifies three groups of congestion areas that merit further federal attention. The most severely congested areas—called "Critical Congestion Areas"—are Southern California and the Atlantic seaboard from the New York City area to northern Virginia.

Comments on the study were accepted from the public through mid-October, and volumes were submitted. The DOE is now working with the North American Electric Reliability Council (NERC), transmission operators, and others to improve the quality of the data required for their detailed analysis and decision-making. It appears that when sufficiently persuasive data are accumulated and all the stakeholders have been given time to make their case (one way or the other), then the DOE makes some decisions. Naturally, any decision made by the department is bound to offend more than one special interest and will undoubtedly end up in federal court. What happens next is anyone’s guess.

An official statement from the DOE notes that it "will designate a National Corridor when the information needed to shape a Corridor appropriately in relation to a known congestion problem is available. DOE recognizes that designation of National Corridors is intended to facilitate construction of new transmission capacity where it is needed, so DOE is not looking for ways to prolong the process." But don’t look for a quick solution, as the meal has so many cooks that it’s not clear what’s going to come out of the oven.

The DOE is on the hook to give an update to Congress one year from the report date, or in August 2007. Don’t expect much in the way of firm decisions until that deadline draws near.

Will generation growth keep pace with demand? Two percent growth in electricity consumption per year doesn’t sound like much, but when capacity numbers and compounding come into play, the number of new plants needed is staggering. EEI’s 2% annual growth rate—which, by the way, is consistent with the latest Energy Information Administration (EIA) projections—translates into a nearly 50% increase in demand over the next 20 years.

If annual growth is indeed 2%, then over 20,000 MW a year of new supply (net of retirements and mothballed plants) will be required. That’s daunting, but doable, given the industry’s capability.

Industrial Info Resources (IIR, www.industrialinfo.com) contributed to this report by providing POWER with an exclusive summary of industry data covering the past decade that you’d be hard-pressed to find elsewhere. Table 1 is our industry report card detailing how the U.S. industry has kept up with demand growth over the past decade. The data, organized by market region, give a pretty good picture of where assets have been and are being developed. The rest of the picture can be gotten from an examination of regional capacity margins, addressed in the next section.

Table 1. Actual and planned U.S. regional power generation resource growth (1998–2007), by state. Source: Industrial Info Resources

Because it contains a wealth of information, Table 1 is well worth your study time. The "Plants under construction" category is current through November 2006. The number of plants with "Announced construction kick-off 2007" is based on direct customer feedback. The numbers prove that developers are perpetual optimists: History suggests that only about 25% of the reported plants will actually break ground during 2007, for a total of 19,000 new megawatts.

Slicing and dicing the IIR data gives other insights into what technologies are being selected (Table 2) and what the favorite fuels are (Table 3). Here, too, developers seem to be very ambitious when reporting project starts for 2007. For example, it’s obvious from the bottom right corner of Table 2 that wind project developers are irrationally exuberant about the coming year, when they anticipate starting construction of 22,389 MW of turbines, with 3,500 MW reaching commercial operation in 2007. The American Wind Energy Association (AWEA) is also predicting that between 3,000 MW and 3,500 MW will be deployed.

Table 2. U.S. power generation resource growth (2000–2007), by generation technology. Source: Industrial Info Resources

Table 3. U.S. power generation resource growth (2000–2007), by fuel type. Source: Industrial Info Resources

IIR projects a sharp increase in project investment for 2007 over the past several years (Table 4). A good portion of that investment could be attributed to the large number of selective catalytic reduction and scrubber projects now under way as a result of the new Clean Air Interstate Rule and other environmental mandates. Again, historically, actual investment has only been about one-fourth of the predicted level.

Table 4. Total installed cost (2006 dollars) by fuel type, in millions of dollars. Source: Industrial Info Resources

NERC: Long-term reliability not so reliable

Every year, NERC looks into the future and judges what needs to be done to improve the reliability and adequacy of the continent’s bulk power systems. NERC’s "2006 Long-Term Reliability Assessment," released this past October, presents a troubling view of what’s ahead. (NERC President and CEO Rick Sergel discusses the subject in this month’s Commentary)

Margins falling fast. The bottom line of the NERC view: "Electric capacity margins will decline over the 2006–2015 period in most regions." This trend, according to NERC, is a product of the "short-term resource acquisition strategy" that has dominated for the past decade. Over the next 10 years, says NERC, U.S. electric demand is likely to increase by 19% (141,000 MW), while Canada’s demand will grow by 13%. Yet the council says the projected level of committed resources over this period (Figure 1) will be a mere 6% (57,000 MW) in the U.S. and 9% (9,000 MW) in Canada.

1. Downhill slide. Expect U.S. capacity margins to decline over the next decade, although uncommitted resources may help reduce the shortfall. Source: NERC

It’s also a near-term problem, according to NERC. Capacity margins look as if they will drop below NERC’s regional target levels in ERCOT, MRO, New England, RFC, and the Rocky Mountain and Canadian areas of WECC "in the next two to three years, with other portions of the Northeastern U.S., Southwest, and Western U.S. reaching minimum levels later in the 10-year period." Only the Southeast looks like it will have adequate capacity margins through 2015 (Figure 2).

2. Working without a net. Electricity supply margins are projected to fall below minimum target levels in the next few years. For those regions with tight supplies, the first year is when additional generating resources are required; the second year is when additional generating resources, beyond uncommitted resources, are required. Source: NERC

Over 50,000 MW of what NERC calls "uncommitted resources" exist today. NERC describes these as generating projects "that either do not have firm contracts or a legal or regulatory requirement to serve load, lack firm transmission service or a transmission study to determine availability for delivery, are designated or classified as energy-only resources, or are in mothballed status because of economic considerations." Over the next 10 years, says NERC, uncommitted resources "will more than double." The commission says these resources "represent a viable source of incremental resources that can be used to meet minimum regional target levels."

Transmission trials. Then there’s transmission. Given the predicted increase in demand, will the grid be able to deliver the goods? NERC is pessimistic. "Expansion and strengthening of the transmission system continues to lag demand growth and expansion of generating resources in most areas," says the electric reliability organization.

Total transmission miles in the U.S. and Canada, says the report, "are projected to increase by less than 7% in the U.S. and 3.5% in Canada." Without more transmission investment, says NERC, "grid congestion will increase, making it more difficult for available supply to meet demands and to allow full utilization of capacity/demand diversity; in some situations, this can lead to supply shortages and involuntary customer interruptions."

The same short-term focus that has retarded development of new generation afflicts transmission, says NERC. "With a few exceptions, the present transmission planning horizon is five years or less. Proposed solutions tend to address short-term problems without looking to longer lead-time facility requirements." NERC adds that the provisions in EPAct that give the DOE the authority to streamline transmission projects may help ease transmission problems, although the department has yet to complete its designation of "national interest electric transmission corridors."

The human factor. The NERC report also cites the aging U.S. workforce as an obstacle to reliability, as the grid rests on "the accumulated experience and technical expertise of those who design and operate the system. As the rapidly aging workforce leaves the industry over the next five-to-ten years, the challenge to the electric utility industry will be to fill this void." NERC says utilities need to "identify key personnel approaching retirement and establish mentoring programs to impart the experience realized by these individuals."

Utilities, says NERC, also need to "reassess compensation and benefits packages" so that they might be able to retain aging personnel full time or part time. Finally, says the report, the industry "as a whole needs to establish cooperative programs with academia to reinvigorate the power engineering education in North America."

Coal: Still a necessary evil

Will cheap Btus trump expensive CO2? That’s what appears to be driving power plant decisions on coal as a fuel for future generation. Differing guesses about the timing of CO2 controls appear to be what differentiates gencos planning to build a new generation of pulverized coal (PC)-fired plants (all of which seem to be supercritical designs) from those that advocate integrated gasification combined-cycle (IGCC) plants.

There’s no doubt that coal plants will dominate new baseload generation for many years to come. The DOE’s National Energy Technology Laboratory says U.S. gencos plan to build 154 GW of new coal plants during the next 24 years, and 50 GW of that over the next five. During the past five years, 6 GW of new coal capacity came on-line.

To PC, or not to PC? It all boils down to what you need and when you need it. If you need lots of new baseload capacity fairly soon but presume that CO2 controls are still several years away, you’ll opt for PC generation and hope to break ground on the new plants so they can be grandfathered in before the new rules take effect. If your planning horizon is farther out and you want to take advantage of some hefty subsidies in the 2005 Energy Policy Act, IGCC may be a better way to go.

Title XVII of EPAct establishes a DOE loan guarantee program (which means that if you default, the taxpayers eat it) to cover 85% of "eligible" projects at a favorable interest rate (another subsidy). So far, the DOE is being cautious, largely driven by the White House Office of Management and Budget. The DOE has capped its exposure in the loan program at $2 billion. This could set off a dispute with the 110th Congress, which is likely to push for accelerated IGCC projects as a greenhouse gas–curbing initiative.

My bet for 2007 is PC coal, even if that’s not politically correct. Conventional coal plants will begin construction, and others will get quickly into the pipeline.

I base my wager on TXU’s stunning November 2006 announcement that it is investing a whopping $10 billion in 11 new supercritical PC plants that will add 9 GW in Texas alone by 2010. Some have called it "environmental brinksmanship." Hedging its bets, TXU said its reference design for the plants would include "ductwork to provide ample access for the addition of a future system" to capture carbon. The giant Texas utility also said its new plants will provide opportunities for storing CO2 and injecting it into wells to enhance oil recovery. That makes a lot of sense because Texas has a lot of elderly oil wells whose life could be economically extended by CO2 flooding.

TXU’s forecasts are even more bullish than the DOE’s. In a November 2006 press release, TXU said it believes that "consumer needs for reliable, secure, affordable, and environmentally-superior power supplies will drive the construction of almost 300 GW of advanced coal power generation facilities across the U.S. over the next 15 years."

To that end, Dallas-based TXU is also looking to develop new coal-fired generation across the country. It starts in the PJM market, with prospects for others to come.

TXU says the "first pillar" of its business plan is "a profitable entry strategy outside Texas." The company sees three major opportunities: 45 GW of "new advanced coal" to displace existing gas-fired generation, "taking advantage of the advanced coal-gas spread and the more efficient TXU development and construction model." Next, says TXU, is "a 78-GW opportunity" to displace old coal plants with new ones (although many old coal-fired plants never die—they just get retrofitted). Finally, says TXU, there is 160 GW of demand for new generation.

At the practical level, Texas is booming, with growth in demand forecast at 25% over the next decade. Nationally, the projection is 19%. The Lone Star State’s peak jumped 5% in the summer of 2006. But we are also hearing proposals for new capacity in the Midwest (from Peabody Energy) and in the Middle Atlantic region.

Grandfather Time. TXU’s plans are more than bullish. Several web sites have been established solely to take the utility to task for its decision. To defend itself, the company explains that its baseload supply needs are so urgent that it had no choice but to reject IGCC as too unproven in favor of supercritical PC technology.

Environmentalists aren’t buying that. They believe the company just wants to avoid paying the coming carbon tax by having its new plants come in under the wire. The more realistic environmentalists—those who understand one tenet of TXU’s argument: that clean wind and sun won’t keep everyone’s air conditioners running full-blast in July—are skeptical of TXU’s gambit. One of those realists, Ralph Cavanagh of the Natural Resources Defense Council, said of TXU’s announcement, "Either it is plain old denial, or they think they can be grandfathered."

That’s the crux of the politics of coal power. Both the industry and the greens are aware of what happened in the various iterations of the Clean Air Act, beginning in 1970 and concluding in 1990. The greens assumed from passage of the law that—eventually—the big, old dirties (FirstEnergy’s Eastlake plant, for example) would be shut down and replaced by newer plants. So they allowed older plants to be exempted from rules for new units unless they were upgraded significantly.

That didn’t happen. From the standpoint of the greens, it was the worst air pollution decision they ever made, and they were unable to repair the damage in the 1977 and 1990 rewrites. The old dirties got upgraded again and again (just short of the magic capacity-increase level) and still were grandfathered from the most stringent elements of the Clean Air Act.

Now the grandfathering issue is alive again, in the contest of carbon dioxide regulation. TXU denies this, of course. Mike McCall, the planner of the company’s construction campaign, told The New York Times, "There’s not some game theory here around carbon."

I think there is, and so do others with experience in the industry. For example, Granger Morgan, head of the engineering and public policy department at Carnegie Mellon University, recently argued in Science magazine against the grandfathering of new coal plants from future carbon regulations. He wrote that any federal carbon laws should stipulate "that when CO2 controls are imposed, no plant built after 2006 will be exempted from coverage (that is, grandfathered), no matter what form future controls on emissions may take. Such a law would not prevent the construction of new coal plants but would strongly encourage builders of conventional plants to design them so as to achieve amine-based CO2 ‘scrubbers’ to be added later. It would also provide an incentive for those building new plants to adopt advanced ‘clean coal’ technology such as [IGCC] or oxyfuel plants that can capture and sequester CO2 in deep geological formations."

Change will be a long time coming. Clearly, carbon regulation will be a driver at both the state and federal levels. It looks unlikely that Congress will do anything on this matter before 2009 at the earliest, and probably for years after that. The body is built for comfort, not speed. Case in point: The 1974 Clean Air Act amendments to the 1970 organic law weren’t approved in the House until 1977 due to bipartisan wrangling led by Rep. John Dingell (D-Mich.), an auto industry champion. The 1977 update took until 1990, again because of Dingell, who is now chairman of the House Energy and Commerce Committee.

Because Dingell will again chair the committee in the 110th Congress, CO2 legislation—which must include cars to be serious—seems unlikely for a while. To my mind, that means near-term bets on PC coal, however un-PC, are going to clear the table.

As for coal gasification, I’ve been hearing that song since the mid-1980s, when American Electric Power led the push for pressurized fluidized-bed combustion (PFBC), IGCC’s forerunner. The DOE has put a lot of money into precommercial plants over the past 25 years with few positive results. IGCC may be technically elegant, but can it be a reliable baseload workhorse and make money for its practitioners? As long as PC plants can be grandfathered from carbon caps, and cost 15% to 20% less than IGCC plants, I have my doubts about the latter.

Natural gas: Under the thumb of the invisible hand

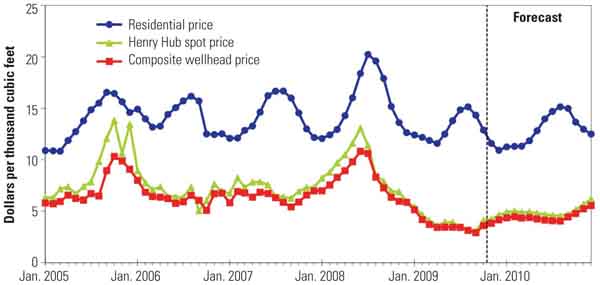

For understanding natural gas in 2007, a refresher course in Economics 101 might not be a bad idea. No generation fuel so completely reflects the vagaries of market economics. When they hear the term "price volatility," most plant fuel buyers these days immediately think of gas.

Over the past 18 months or so, the price of natural gas has yo-yoed from under $5/mmBtu, to $9, to around $7 today. The EIA says it expects natural gas prices—at least the Henry Hub spot price—to average about $7.80 this year. A review of the history of U.S. gas regulation and prices helps explain where we are today.

In the past 30 years, gas has escaped heavy-handed federal regulation and become a commodity whose price is set by a free-wheeling, intense futures market. Unlike coal, most gas for fueling generation is bought on a short-term basis on a national market, where it also is in demand from local gas distribution utilities serving the home heating market and large industrial consumers. It’s a jungle out there.

Controlling gas. Prior to 1978, the Federal Energy Regulatory Commission (FERC), which was then known as the Federal Power Commission, regulated both gas production and gas pipeline prices. This arrangement was an artifact of the 1930s, when Congress and the executive branch were crafting laws governing energy supply—including the 1936 Public Utilities Holding Company Act and the 1938 Natural Gas Act—based on the assumption that gas and electricity were natural monopolies that required heavy government regulation to protect consumers from price gouging.

For the next 40 years, interstate gas prices were regulated, but intrastate prices were not. Nobody paid much attention. Then several extremely cold winters in the 1970s (some of the same scientists who now warn of global warming were then warning of global cooling) resulted in shortages of gas for home heating in the interstate market, where prices were regulated. At the same time, gas flowed freely to the intrastate market, where prices rose and fell to reflect the balance of supply and demand.

Congress reacted with typically contradictory approaches. The 1978 Powerplant and Industrial Fuel Use Act (PIFUA) essentially banned the burning of gas in new utility generating plants. As a result, nuclear plants were built in the middle of gas-rich areas such as Texas, Oklahoma, and Louisiana, and construction of coal plants was encouraged nationwide. The notion behind this, articulated by environmental guru Amory Lovins, was that gas was too important to be allowed to generate electricity.

Loosening control. But at the same time, Congress passed the 1978 Natural Gas Policy Act, which decontrolled some categories of gas and began a policy movement toward complete decontrol. As some gas became subject to market prices, and other supplies did not, a "gas bubble"—a large amount of gas supply in excess of demand—developed.

When Congress and FERC in the mid-1980s completed the decontrol of natural gas prices (Congress killed PIFUA in 1987), a blossoming of gas-to-electric plants ensued. Gas plants are much less capital-intensive than coal or nuclear plants, they’re better at following load, and their modularity makes them more flexible for service reconfiguration. And (this wasn’t as big a deal back then as it is today) gas is inherently less polluting than coal. In short, gas is a marvelous fuel—as long as the price is right.

By the 1990s and early 2000s, gas was the flavor of the month for new generation. Last year, according to EIA figures, natural gas fired nearly 19% of U.S. generating capacity, behind nuclear (but not by much) and coal. How things changed from 30 years prior, when gas was too valuable to homes to be burned in a power plant.

Market correction. But by the middle of this decade, the consequences of deregulation and capitalism came home to roost. The boom in gas-fired generation soaked up the excess gas, prices rose, and gas-fired projects not well under way got scrapped. The bubble burst.

High prices reduce demand, and EIA predictions reflect that. The DOE’s current short-term energy outlook pegs 2007 gas demand for electric generation at 5.95 trillion cubic feet, down from an estimated 6.22 tcf in 2006.

In theory, and almost always in practice, free markets are self-correcting. Sustained high gas prices should increase supplies from fields previously considered uneconomic. And with the federal government’s backing, high prices make it more likely that a gas pipeline will be built to bring Alaska’s large gas reserves to the lower 48. Much of that gas is now flared, although some is liquefied and sent by tankers to world markets.

Nuclear: Changing pros and cons

Last year featured a lot of optimism about the prospects for a new generation of nuclear plants in the U.S. Yet no American utility has ordered a new reactor for 30 years, and every order since 1974 has been cancelled.

Why the optimism? The U.S. Nuclear Regulatory Commission (NRC) approved new, advanced reactor designs and streamlined its cumbersome two-step licensing process. Congress put substantial goodies into EPAct for the nuclear family of utilities and reactor vendors: production tax credits worth about $3 billion, insurance against regulatory delay, and loan guarantees.

Concerns about global warming also helped and have made even some environmentalists more sanguine about nuclear power (even if they’re unhappy about the absence of a solution to the waste problem). Nuclear is the baseload generation technology that does not generate greenhouse gases. Anyone serious about global warming has to at least give nukes another look.

So why aren’t new plants jumping off the shelf? Three years ago, MIT professors John Deutch and Ernest Moniz, both veterans of the Clinton administration (Deutch was also a highly ranked DOE official in the Carter administration), organized an interdisciplinary study of "The Future of Nuclear Power."

The Deutch-Moniz report said, "The nuclear option should be retained precisely because it is an important carbon-free source of power." But the report identified four major obstacles to a nuclear revival, at least in the U.S. Those are: "high relative costs; perceived adverse safety, environmental, and health effects; potential security risks stemming from proliferation; and unresolved challenges in long-term management of nuclear wastes."

All are daunting, but the cost issue seems to be uppermost in the minds of anyone in the private sector who’s considering stepping onto the long regulatory path to building a nuclear plant. My prediction is that 2007 will not see any significant movement toward new nuclear plants, although there are rumors that both Constellation Energy and Dominion are contemplating filing combined construction and operating license (COL) applications at the NRC this year.

Financing challenges. Last summer, The New York Times’ veteran energy reporter Matt Wald looked at nuclear plants as part of a series of stories examining the prospects for various energy technologies. He focused on two utility executives, both of whom run companies with nuclear plants.

One was Mayo Shattuck III, CEO of Baltimore-based Constellation Energy, an enthusiastic member of the NuStart Energy consortium. NuStart’s members include nuclear utilities and the reactor vendors General Electric and Westinghouse. NuSTART is investing its own and taxpayer money (through the DOE) to test whether the NRC’s new COL process will work.

Shattuck told Wald that his company hopes to apply for a COL by the end of 2007. At the time of the interview, Constellation was working with the French-German reactor vendor AREVA for a new European pressurized water reactor (PWR) design at the existing Calvert Cliffs two-unit plant in Maryland. But that was before Constellation’s merger with FPL Group (another NuStart member) collapsed.

Now, NuStart says it does not expect to apply for a COL, which would be for the GE or Westinghouse advanced reactors, until 2008. My sources tell me that NuStart and the DOE are wrangling about additional government funding, with the consortium saying it needs $120 million, versus the $80 million approved by the government.

Then Wald talked to William P. Hecht, CEO of PPL Corp. in Allentown, Pa., which owns two operating nuclear units. Hecht doesn’t think the business case for a new nuke can be made today. In fact, he said he wouldn’t build any big plant without the assurance of a power-purchase agreement that could be taken to project financiers. "I’m not going to build any large generation unhedged," Hecht said. "If you build 1,000 megawatts, how are you going to find someone to buy it 10 years after it is finished?"

We’re talking big money here. Most estimates of the capital cost of a new, 1,000-MW nuke run from $2 billion to $4 billion. On top of that, the NRC-approved GE and Westinghouse advanced reactors have not yet been built, so a construction project could face significant risks. According to MIT’s Ernie Moniz, "There is no question that the up-front costs associated with making nuclear power competitive are higher than those associated with fossil fuels." Dan Reicher—a former DOE assistant secretary for energy efficiency and renewables in the Clinton administration, a lawyer for the Natural Resources Defense Council, and now president of New Energy Capital—said, "There is some interest [in nuclear power] on Wall Street, but I would not consider it deep and broad."

Waste, security still concerns. Another issue that clouds the future of U.S. nuclear power is spent fuel. Specifically, Yucca Mountain in Nevada seems to many observers no closer to actually storing waste from commercial reactors than it was when Congress passed the 1982 Energy Policy Act.

Today, after years of delay and nasty political wrangling, the DOE says the earliest it can expect to open Yucca Mountain is 2017. It has yet to file an application for a license to the NRC. Many in the industry believe 2017 is wildly optimistic, particularly now that Sen. Harry Reid (D-Nev.), a dedicated opponent of the project, is the Senate majority leader. An official at Entergy told me, "We aren’t counting on Yucca to ever open, so we are planning for on-site storage at all our reactors."

Another bugaboo is plant security, an issue that wasn’t even on the radar prior to 9/11. There’s no doubt that nuclear power plants are among the most secure, most robust industrial facilities that could be a target of a terrorist attack. But anti-nuke groups have been assailing the NRC on the issue, and the agency has taken note. In early November, the NRC told its staff to study whether the new reactor designs, including the three it has already approved—the GE advanced boiling water reactor, the Westinghouse AP-1000 and AP-600 PWRs, and the AREVA design—are vulnerable to attack by a terrorist crashing a jetliner into them. Some industry experts believe the AREVA plant is less vulnerable to attack than the U.S. designs.

This issue has divided the NRC. Commissioner Gregory Jacko, regarded as less sympathetic to the nuclear industry than the other commissioners, has been pushing for NRC action that would order reactor vendors to design new plants to withstand an airplane attack before the NRC allows concrete to be poured. The other four commissioners don’t agree, so the commission has ordered a staff study.

Nuclear politics. What happens in Washington doesn’t stay in Washington, and that’s particularly true for nuclear power. The November 2006 elections could hardly have been more unfavorable for the nuclear industry’s lobbying efforts. The Nuclear Energy Institute (NEI), the industrywide lobby, made a big bet that Karl Rove’s plan for a "permanent Republican majority" would work. At the behest of then-Senate Energy and Natural Resources Committee Chairman Pete Domenici (R-N.M.), the NEI hired retired Admiral Skip Bowman, a Republican, to head the institute and Alex Flint, a former Domenici staffer, as head lobbyist.

In the 110th Congress, both the House and Senate will be run by Democrats. Domenici will be in the minority. In the House, Rep. John Dingell, a frequent political thorn in the side of the nuclear industry, will chair the House Energy and Commerce Committee, where he ran the show from the early 1980s to 1994. During that time, he forced the Tennessee Valley Authority to shut down its entire nuclear fleet for years. Rep. Edward Markey (D-Mass.), the nuclear industry’s worst political nightmare, likely will chair a committee that will subject the NRC, the DOE, and the nuclear industry to oversight scrutiny they haven’t seen in a dozen years.

Washington energy consultant Roger Gale, a former DOE official in the Reagan and first Bush administrations, surveys electric utility officials yearly for their views of the future. He says those who responded to his latest survey (more than 100) predicted that a new nuke will be ordered soon, but they don’t expect "a future where nuclear generation represents a larger share of generation."

Renewables: Strong, steady performance

How do you make major increases in market share year after year? The trick is to start small, which is the route that renewable generation has been taking and is likely to continue taking in 2007. As the EIA says in its most recent Annual Energy Outlook, "The expected rapid growth in the use of biofuels and other non-hydropower renewable energy sources begins from a very low current share of total energy use; hydroelectric power production, which accounts for the bulk of current renewable electricity supply, is nearly stagnant."

According to the EIA, nonhydro renewables accounted for only 2.3% of U.S. electric generation in 2005. Hydro had a 6.5% market share. With hydro out of the picture, that largely leaves wind, solar, geothermal, and biomass. Each has certain inherent geographic limits: solar needs sunshine (utility-scale solar is still largely a pipe dream); wind seems to be strongest and most reliable in remote spots, such as mountain ridges and offshore; geothermal requires access to geologic steam or hot rocks; biomass—almost entirely wood waste—depends on killing trees.

Wind is soaring. Most of the buzz in recent years has been around wind, with many major energy companies, such as FPL and BP, making large investments in utility-scale wind projects. According to the American Wind Energy Association, 2006 probably closed out with over 2,700 MW of new capacity, a new annual record. Total U.S. wind capacity now likely exceeds 11,000 MW.

AWEA estimates that new capacity in 2007 will be in the 3,000 MW to 3,500 MW range. But remember that the wind trade group estimated early last year that 2006 would see 3,000 MW of new capacity, and additions fell short. The group now says that "it is now clear that a few projects originally slated for completion in 2006 will not be finalized until 2007 because of various delays." That’s a veiled reference to the shortage of wind turbines; blade manufacturers can’t keep up with demand.

Since 1992 the wind boom has been driven by production tax credits, which now amount to 1.9 cents per kWh. Without these tax incentives, investment in new wind projects would quickly stall. The tax credits, which Congress has repeatedly renewed, run out at the end of 2008, so the industry will be lobbying heavily this year for another extension.

One development in early December may have portents for wind. Goldman Sachs, which 18 months earlier bought Zilkha Renewable Energy for an undisclosed sum and renamed it Horizon Wind Energy, has put the wind business on the market. According to Sparkspread.com, Goldman Sachs could get $1.5 billion from the sale. A Sparkspread editor said, "Lots of bankers look at Goldman Sachs as the weathercock of the energy industry and so many are assuming that it is now calling the top of the market." A HypoVereinsbank banker in New York told The Times of London, "There is a large amount of uncertainty surrounding the industry . . . and this is causing a good deal of concern among its leading players."

Geothermal joins the funded club. When Congress extended the production tax credit in EPAct, it added new geothermal facilities to its list of qualifiers. The result, says the Geothermal Energy Association (GEA), is "the U.S. geothermal industry’s most dramatic wave of expansion since the 1980s." The GEA says some 58 new geothermal energy projects are now under development, with up to 2,250 MW of capacity. This would nearly double U.S. installed geothermal capacity to over 5,000 MW.

"The good news," said Karl Gawell, GEA’s executive director, "is that federal and state incentives to promote geothermal energy are paying off. We are seeing a geothermal power renaissance in the U.S. The bad news is that some projects are already being put on hold because of the impending deadline for the federal production tax credit." He noted that large plants running in baseload—geothermal’s best service mode—take several years to build. "The deadline urgently needs to be extended."

LNG: The other gas

There were Halle Berry, Pierce Brosnan, and Cindy Crawford on the beach in Malibu last October. Offshore on a pink surfboard was Daryl Hannah. They were all part of a protest, organized by Brosnan, calling on California Governor Arnold Schwarzenegger to reject a liquefied natural gas (LNG) terminal planned for 14 miles off the Malibu coast. Australian energy company BHP Billiton wants to build the regasification plant to help supply the region’s hefty appetite for gas. Four other LNG terminals are planned for various locations in the state. All have proven very unpopular.

The key to the future of LNG is NIMBY (Not In My Back Yard), NOPE (Not On Planet Earth), LULU (Locally Undesirable Land Use), and BANANA (Build Absolutely Nothing Anywhere Near Anything). Opponents of LNG projects trot out a litany of fears: explosions, fires, terrorism, and pollution. All are overstated, but all have a basis in fact, and that makes persuading the populace to support the projects very difficult.

Growing interest. Given sustained high domestic natural gas prices, LNG could become a solid niche business in the U.S., particularly in cases where the owner of the gas can play the spark spread between gas and electricity prices. In 2004, Cambridge Energy Research Associates (CERA) predicted that the global LNG industry would grow in the eight years to 2012 "by the same amount as in the first 40 years of its history." By last summer, that prediction looked gloomy. Still, CERA predicts that LNG will become a $65 billion market meeting 15% of the world’s gas demand by 2012.

Most of the attention is on one country and one site: Ras Laffan in Qatar. CERA said, "The combined capacity of Qatari LNG investments focused just on the United States is broadly equivalent to the proposed capacity of the Alaskan pipeline." The analysis adds that once the capital costs of an LNG project are sunk—and they are heavy—"the variable costs are minimal, at less than $2 per mmBtu."

LNG projects face a relatively benign regulatory environment at the federal level, although that is generally not the case at the state or local level. FERC regulates on-shore facilities. The U.S. Maritime Administration regulates offshore terminals. Neither has ever denied an application. A project also must also get Coastal Zone Management Act, Section 404 water quality certification and Section 404 dredging permits.

Today, six LNG terminals operate in the U.S. (Figure 3): in Everett, Mass.; Cove Point, Md.; Elba Island, Ga.; Lake Charles, La.; Peñuelas, Puerto Rico; and Kenai, Alaska. FERC says there are about 40 project proposals before the commission or being discussed in the industry.

3. LNG options grow. Many LNG terminals are under development. But few have been approved and only five are operational in the continental U.S. Source: FERC Office of Energy Projects

The commission notes, "The market ultimately determines whether an approved LNG terminal is ever built. Even if an LNG terminal project receives all of the federal and state approvals, it still must meet complicated global issues surrounding financing, gas supply and market conditions. Many industry analysts predict that only 12 of the 40 LNG terminals being considered will ever be built."

But it’s not only the business market that will decide the fate of these projects. It’s the larger marketplace of ideas, including the politics of energy project siting.

Fears may foil approvals. That’s where the scare tactics come in. Richard Clarke, former Clinton and Bush administration antiterrorism chief, noted in a recent book, Against All Enemies, that two terrorists got into the U.S. from an Algerian LNG tanker unloading in Boston. In January 2004, an Algerian gas compressing plant exploded, killing 27 workers.

A Sandia National Laboratory safety report published in December 2004 said that a major accident on a tanker could cause a fire that would melt steel half a mile away. Three lawyers for the Washington law firm of Sutherland, Asbill and Brennen, writing in LNG Observer, said that "all governmental and private stakeholders in the LNG debate quickly realized that the Sandia study changed the landscape for evaluating public safety issues surrounding LNG terminals."

What will we see with LNG in 2007? FERC will approve some of the projects now before it, including the proposed expansion of the storage and sendout capacities of the Elba Island facility, near Savannah. But it’s reasonable to suggest that more projects will be cancelled than approved.

And if we get to see more of Halle Berry on the beach at Malibu, well, that’s not a bad thing.