The U.S. power industry’s story in 2009 will be all about change, to borrow a now-familiar theme. Though the new administration’s policy specifics hadn’t been revealed as POWER editors prepared this report, it appears that flat load growth in 2009 will give the new administration a unique opportunity to formulate new energy policy without risking that the lights will go out.

Astrange and funny thing happened on the way to a power generation boom last year. Wall Street collapsed under the weight of a mortgage crisis last fall, creating a credit crunch not seen, according to many experts, since the Great Depression of the 1930s. Then the U.S. economy, followed by the rest of the world, went into a free fall. Bye, bye, generating boom.

Fear and loathing in credit markets — to crib from the late, great gonzo journalist Hunter Thompson — quickly replaced optimism and trust. Lenders were reluctant to lend, preferring to sit on their cash. Borrowers were faced with no credit, or credit at rates that would eat the profits of projects they wanted to build. The result? Cancelled or delayed infrastructure projects, retreats on scheduled upgrades, and a hormonally driven urge to merge among financial firms and energy companies.

The across-the-board cramping up of international credit markets last fall quickly dimmed prospects for high-capital energy projects, including new generation and major high-voltage transmission ventures. Despite the $700 billion Bush bank bailout package of October 2008, as well as an extension of renewable energy tax credits in legislation enacting that bailout, the temporary collapse of credit markets in late 2008 rendered doubtful major new projects from nuclear to coal to wind and solar. Pitches for capital-intensive projects were met with the ruling, "You’re out."

How can producers get anything on the scoreboard? Gas generation — requiring less upfront capital, although the fuel costs are unpredictable — looks like the generating resource of last resort. On the plus side for gas, prices have been in major retreat during the economic meltdown. Also, gas generation can be built near load, obviating the need for expensive electric transmission. Other virtues: Gas projects go up quickly, and they can be modular.

Will capital markets rebound in 2009? As we write this in late 2008, the credit constipation appears to be clearing, although how quickly the clog will flush is still unknown.

Managing Expectations

The resounding election of Barack Obama to be president, and expanded Democratic majorities in the House and Senate, portend a somewhat different approach to energy politics in Washington in 2009. Though policy specifics have yet to be revealed, we do know that the president-elect is a fan of renewable power and carbon controls but does not support construction of conventional coal plants or the Yucca Mountain spent nuclear fuel repository. We also know that the prospects for global warming legislation, specifically for a cap-and-trade program (a new tax by any other name, according to some analysts), are greater today than they were four years ago. But John McCain had also supported the idea of legislating control of carbon dioxide emissions, and particularly power plant CO2 emissions.

Ned Helme, president of the Center for Clean Air Policy, a group that advocates climate legislation, said after the Nov. 4 election that his organization "is confident the Obama administration will embrace the very important challenge of collaborating with the new Congress to adopt national climate change legislation that includes a cost-effective cap-and-trade system and work to establish vital green jobs and green technology for the international economy."

Should Congress, where coal-state legislators in both parties remain an important bloc, balk at carbon control legislation, it seems likely that an Obama administration would move administratively. Jason Grumet, Obama’s energy and environmental policy advisor, has said repeatedly that an Obama administration believes it has adequate authority under the 1990 Clean Air Act Amendments to impose a regulatory regime on CO2 emissions. Grumet is rumored to be a leading candidate for energy secretary in the new administration.

But the new administration could also push new energy projects as part of a strategy to invest in infrastructure, loosely defined, as a way to jump-start the sluggish U.S. economy. This could include electric transmission, power plant construction (more likely favoring coal and renewables rather than nuclear), and subsidizing carbon capture and sequestration. Though some will call this pork-barrel spending, the conventional view in Washington is that one legislator’s pork is another’s porterhouse.

New Infrastructure Required

That the U.S. needs major new electricity generating plants and transmission infrastructure — including baseload coal and nuclear — seems indisputable. Almost every examination of U.S. electricity markets — from the Energy Information Agency (EIA) to the North American Electric Reliability Corp. (NERC), to the various state and regional power agencies — finds capacity margins a problem. Although there is no agreement on what is a prudent capacity edge (the 30% to 40% margins of the 1970s and 1980s were clearly excessive and too expensive), most analysts seem to agree that around 15% is reasonable (arrived at by a wet-thumb-to-the-air test, rather than any solid engineering calculations). Some reliability regions in the U.S. could be bumping up against that 15% figure not too far into the future, according to the NERC analysis.

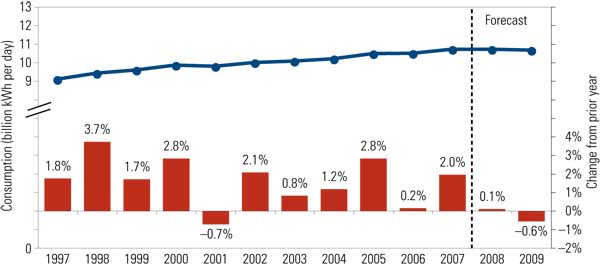

But NERC’s latest forecast provides reason for optimism that blackouts are not in the picture for 2009. "Lowered load forecasts for the coming ten years and new market mechanisms have contributed to generally improved capacity margins for most of North America," said NERC in its late October "2008 Long-Term Reliability Assessment." Slower economic performance is a reason (U.S. gross domestic product dropped 0.03% in the third quarter of 2008 and may also drop in the fourth quarter). As of Dec. 1, the country was officially in a recession, and that will likely mean reduced demand for energy, including electricity. The recession will also reduce the strain on existing electric infrastructure (Figure 1).

1. U.S. total electricity consumption dropping. The economic slowdown will impact consumption in all sectors, particularly the industrial sector, which is now expected to decline by 2.5% in 2009. Source: EIA Short-Term Energy Outlook, November 2008

What is the best way to ensure that U.S. system reliability is robust enough to prevent major blackouts and brownouts in the coming year and years to come? Many experts agree that a combination of new generation and new transmission capacity are necessary, particularly if the nation is to begin integrating major increases in variable renewable resources, located far from electric loads, into the generation and distribution mix.

NERC CEO Rick Sergel said the most pressing problem facing the nation is a dearth of investment in transmission, not generation: "Transmission lines are the critical link between new generation and customers, yet we continue to see transmission development lag behind generation additions. Faster siting, permitting, and construction of transmission resources will be vital to keeping the lights on in the coming years."

As governments of the world scrambled to restore order to financial markets at the end of 2008, it appeared that money needed for energy infrastructure, including generation and transmission, would not be easily available. In the mid-to-late-2008 time frame, oil prices started heading south. So did natural gas prices. Though the retreat of energy prices relieved some political pressure as gasoline prices and the cost of heating homes fell, it left the future of new generation projects in doubt. Why invest new capital in a market where returns look as if they could be shrinking?

Kevin Book, energy analyst for FBR Financial Markets, predicted to a group of reporters in late October that the worldwide financial collapse will lead to vast underinvestment in everything from renewables to coal to transmission because of constrained credit markets and lower energy prices. Investors will be extremely cautious with their bets on the future. That could be foolish in the long run.

The downside of that underinvestment, Book predicted, is that when the next energy price spike occurs — as he confidently said it will — the results will be "really nasty." Having underspent in the wake of the current economic crisis, when higher energy prices hit in the future, said Book, the U.S. will be increasingly unprepared for the results. Those include energy shortages, blackouts, much higher prices, and pain and suffering across the economy.

King Coal Has No Clothes

With over 50% of the market, coal continues to be the king of the U.S. generating hill. But new coal projects, which looked likely just three years ago, are facing increasing difficulties. These obstacles include political opposition, state rate and environmental objections, financial skepticism, and the possibility of reduced short-term demand due to a possibly protracted, worldwide recession.

The past few years have not been particularly good for new coal-fueled projects; 2009 doesn’t look better. An analysis by SourceWatch, a web-based infrastructure tracker, concluded, "Between 2000 and 2006, over 150 coal plants were fielded by utilities in the United States. By the end of 2007, 10 of those proposed plants have been constructed, and an additional 25 plants were under construction. But during 2007, a large number of proposed plants were cancelled, abandoned, or put on hold."

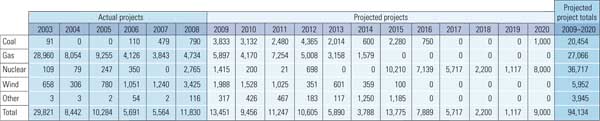

A mid-2008 analysis of coal capacity claims, updating an earlier report by the Department of Energy’s (DOE’s) National Energy Technology Laboratory (NETL), found, "Historically, actual capacity has been seen to be significantly less than proposed capacity. For example, the 2002 report listed 36,161 MW of proposed capacity by the year 2007, when actually only 4,487 MW (12%) were constructed." The NETL analysis concluded (no surprise to those who have followed the industry): "Delays and cancellations have been attributed to regulatory uncertainty (regarding climate change) or strained project economics due to escalating costs in the industry." The Edison Electric Institute projections are a bit more conservative but do not include merchant plant construction (see table).

Planned new units and plant expansions. This table includes only regulated utility assets. Source: Edison Electric Institute Q3 2008 Financial Update

Another factor constraining coal has been that state energy and environmental regulators have eschewed the fuel in favor of projected, and politically favored, renewables, according to SourceWatch. Its analysis noted that in "Delaware, regulators cancelled a coal power plant proposed by NRG Energy in favor of an alternative proposal that combined wind and natural gas." California in 2008 essentially banned any kind of coal-fired power from entering its electricity mix, whether it was generated in the state (long-forbidden) or beyond the state’s borders (long a California staple).

A classic example of the dilemma of new coal-fire generation comes from southern Montana, where generators have access to enormous amounts of low-cost, low-sulfur Powder River Basin coal. Southern Montana Electric Generation & Transmission Cooperative, a rural electric cooperative, has been trying for several years to develop a 250-MW, coal-fired circulating fluidized-bed plant, similar to a recently completed plant at the co-op. The project was designed to balance the co-op’s reliance on power from the federal Bonneville Power Administration’s hydro system.

Under past circumstances, the Highwood Generating Station near Great Falls likely would have been a no-brainer. The generation and transmission co-op would get political support from the distribution co-ops it serves and from the Montana congressional delegation. The U.S. Department of Agriculture’s Rural Utilities Service (RUS) would underwrite financing for the plant, guaranteeing low-interest credit and low consumer rates. The project would move forward without protest. That’s been the model in the rural West for decades. The utility began moving earth in late October, under those expectations.

But the project has run into a green political buzz saw, with the Helena-base Montana Environmental Information Center (MEIC) leading the opposition to the plant. The MEIC fired off a shotgun shell of reasons the plant should not be built: The plant would pollute with CO2 emissions, charged the opponents, violating the state air permit; it would also violate permit requirements for particulates (PM2.5). The opponents also raised zoning and land use objections.

A major blow to the Highwood plant came last February, when the RUS, usually the most generous of public power plant financing sources, turned thumbs down on Highwood and all other pending coal-fired projects. It was allegedly a temporary move. According to the Great Falls Tribune, the RUS policy to back away from baseload coal projects came from the White House’s Office of Management and Budget. In a phone interview, RUS Administrator James Andrew told the newspaper, "The feasibility of [Highwood] made us a little bit nervous."

Rick Sergel, NERC’s CEO, told the New York Times over a year ago, "It’s clear new coal-fired generation is running into roadblocks. I don’t believe we can allow coal-fired generation to become an endangered species. We simply must use all the resources we have."

Good luck. Making that case appears increasingly problematic. The only other obvious baseload generating technology, nuclear, may face equally hard times ahead, despite highly hyped rumors of a nuclear rebound.

Nuclear Renaissance Flounders

No company has more loudly trumpeted the so-called "nuclear renaissance" than Baltimore-based Constellation Energy, owner of two well-run 1,000-MW pressurized water reactors in Maryland’s Calvert County, some 30 miles south of Charm City. Constellation CEO Mayo Shattuck III has aggressively pushed for a third reactor at the Calvert Cliffs site. This enthusiasm comes despite the fact that Constellation is a merchant generator, without any guarantees that it can recover the costs of a new nuclear unit, since it has no captive customers.

Constellation’s two nuclear units at the site on the Chesapeake Bay are fully amortized and generate low-cost electricity, meaning they are successful bidders into regional PJM power supply auctions. That’s no guarantee that a new unit — with a capital cost in excess of $6 billion — would be a successful bidder into a competitive generating auction, according to financial experts following the current interest in new nuclear capacity.

Today, nuclear power generates 20% of U.S. electricity, and does it cheaply, as plant capital costs have mostly been retired. That’s a testimonial to current nuclear power plant management. But financial gurus note that it is not a persuasive argument for new nuclear generation. New nukes would entail very expensive capital costs that would have to be paid by customers.

Constellation also is a major player in commodity energy markets across the country, which almost sunk the company. In late 2008, Constellation’s traders were betting, through derivative contracts, that oil prices would continue rising as they had at the end of 2007 and well into 2008. The traders leveraged those bets, backing them by credit, not cash. So the bids were reliant on credit ratings from agencies such as Standard & Poor’s (S&P) to ensure that the company could pay if its bets proved bad.

Constellation wasn’t putting what it thought was real money at risk, but was speculating on its vision of the future. The company was confident its financial wagers would pay off.

Oops! Oil prices stabilized and then began to fall at the end of 2008. Credit rating agencies, particularly S&P, started looking askance at Constellation’s trading book. As Constellation’s long positions on oil prices began to look dangerous, S&P said it was contemplating a credit downgrade. That would mean a margin call by lenders on Constellation’s market bets.

But Constellation didn’t have the cash to cover the demand for new collateral. The company, according to several published accounts, was 48 hours away from default and bankruptcy when Warren Buffet last September stepped in to rescue Constellation, on very favorable (to Buffet) terms.

Constellation Energy narrowly avoided the financial grim reaper. But it’s possible that the company’s ambitious plan for new nuclear generation will be sidelined as a result. Some industry insiders expect Buffet will unwind Constellation’s trading book, scrap the plans for new nuclear generation at Calvert Cliffs, and focus on Constellation’s regulated utility, Baltimore Gas & Electric. The dreams of Constellation’s Shattuck, a fancy finagling finance man, may have gone up in fiscal smoke.

So, too, may the plans of other would-be nuclear generating enterprises, driven by the radioactive pixie dust of the 2005 Energy Policy Act. To extend the Peter Pan metaphor, the political Tinker Bell of 2005 ("if we just believe") may be replaced by the crocodile of the 2009 financial markets. The year ahead, enmeshed in economic crisis, looks grim for power generation and new transmission, across the board. Nuclear — the most heavily dependent on big, up-front capital — may be the first to feel pain.

The several-year-long nuclear renaissance fever has been driven in part by the fervor for reducing manmade greenhouse gases (mostly CO2) and the irrational exuberance of congressional Republicans for generating electricity from uranium at whatever the cost. In 2005, after many years of legislative failure, the Republican Congress passed the new Energy Policy Act.

Largely due to the efforts of New Mexico Republican Pete Domenici, then-chairman of the Senate Energy and Natural Resources Committee, the new law contained several incentives for nuclear power, an industry that has been stagnant for 30 years. Domenici’s support for nukes was no surprise, given that New Mexico is a major producer of uranium fuel and the home to major DOE nuclear facilities (although there are no nuclear generating plants in the Land of Enchantment).

For the nuclear power industry, the most-coveted of the 2005 law’s atomic goodies was loan guarantees for the next generation of nuclear generating plants. The act provided $18.5 billion in loans; the industry persuaded the Bush administration that the guarantees should cover 80% of the capital costs of a new nuclear generating plant.

At the same time, developers of new nuclear plants were lining up at the U.S. Nuclear Regulatory Commission (NRC) to take advantage of a supposedly streamlined licensing process that combined a construction permit and an operating license into one application. In prior years, utilities needed a construction permit to build a plant and then an operating license before they could run the plant (see sidebar, "Haste May Cost New Nuclear Critical Time").

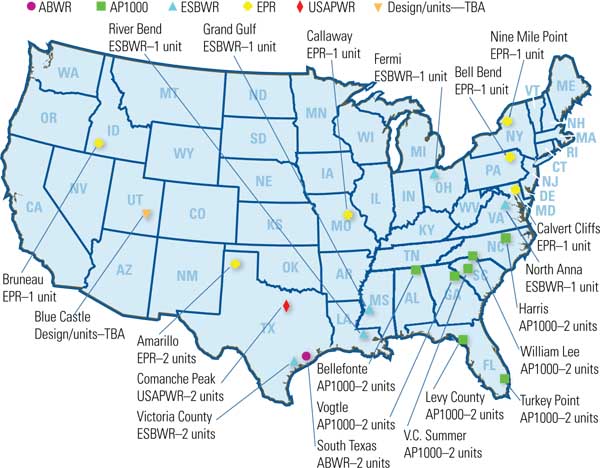

Potential builders and operators queued up at the NRC (Figure 2), knowing that they couldn’t get the loan guarantees, and private-sector financing, without an NRC license. For its part, the NRC laid out a licensing process that would require 42 months for approval (this passes for streamlining in Washington).

2. Location of announced new nuclear plants and their reactor technology. Source: Nuclear Regulatory Commission

The result? Gridlock, at precisely the time that worldwide credit markets collapsed. At last count, some 24 nuclear units were lined up at the DOE for loan guarantees totaling $122 billion, for a total capital cost of $188 billion for new plants. The demand simply swamped the available funding authority. The DOE was wringing its hands and decided to toss the problem to the incoming administration.

What’s the final score for the nuclear efforts of the outgoing Bush administration? A long-time nuclear lobbyist told POWER recently, "This has been the most pro-nuclear administration in the last 30-plus years, and not a spade has turned on new construction during its eight years in power. Don’t bet on any different outcome in a new administration."

Natural Gas’s Future Uncertain

Who wins in a world where coal and nuclear are constrained by finance and politics? It looks as if natural gas, with 20% of the generating market (equal to nukes), may be the winner. The chief attribute of gas, as always, is low capital costs. That’s a major plus in an economy where cash and credit are scarce. On top of that, gas plants can be built close to load, meaning they don’t require a lot of high-cost, high-voltage transmission. They are also a lower emitter of carbon dioxide than coal.

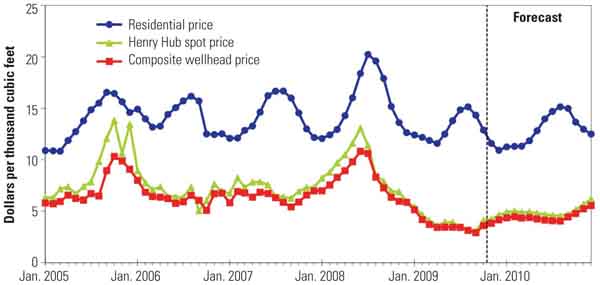

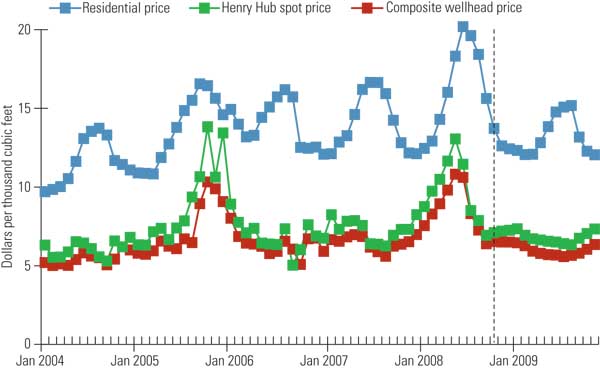

The downside? Natural gas prices are volatile and have swung mightily over the past decade or so. But that’s also the upside, note gas mavens. According to the EIA, since July 2008, wholesale natural gas prices have fallen from nearly $14/million Btu to $6/mmBtu (Figure 3), tracking the fall in crude oil prices (although many experts claim the two price curves are not causally connected).

3. U.S. natural gas prices are dropping. Natural gas prices are expected to remain stable for 2009, reflecting essentially zero growth in the electricity supply. Source: EIA Short-Term Energy Outlook, November 2008

Cambridge Energy Research Associates (CERA) in a recent report notes that natural gas prices have been remarkably stable during recent market upsets, including two major fall 2008 hurricanes that disrupted oil and gas production in the Gulf of Mexico. Says CERA, "The North American natural gas market’s calm in the midst of two hurricanes and financial crises through September and October has been notable," with prices on a general, and gently, falling trend. CERA said it "believes that the gas market has remained steady because it is in balance, with supply equal to demand at a small premium over long-term supply costs, and storage inventories sufficient to withstand short-term disruptions."

The CERA analysis points to another attribute that makes gas attractive to generators: Like coal, it can be easily stored, enabling buyers to lock in prices. The EIA reported in its weekly natural gas report at the end of October, "Working gas in storage increased to 3,347 billion cubic feet." That’s up significantly from the same period a year ago, the EIA noted.

At the same time, gas used for power generation dipped in price, along with consumers’ use of electrical power. The dip in gas usage for generation suggests that pressures on gas prices could lead to decreases, rather than increases, in electric rates. That’s good news for gas-fired power customers. The Fort Worth Star-Telegram reported in late October that lower natural gas prices are already translating into lower local electricity prices, reversing trends earlier last year, particularly in the summer of 2008. Lower bills could encourage higher electricity usage, providing an opportunity for new gas-fired generation.

If electricity usage slides on an economy in recession, gas prices could also decline. That would make running intermediate and peaking gas-fired units more economical. The spark spread — the difference between the financial yields from selling gas to generate power or to heat homes — could favor generation.

That’s the short-term outlook — for 2009.

What’s the longer view? CERA says, "The long-term effects on gas — and energy — are uncertain. Although the physical natural gas market remains in balance and prices are relatively stable, CERA believes that the wholesale restructuring of financial markets, the disappearance of major players from the trading floor, and the global credit squeeze will have long-term effects on natural gas investment and demand. Oil and gas companies with sound balance sheets will have an advantage in financing new projects or acquisitions."

Expect Stagnant LNG Growth

Three years ago, with U.S. natural gas prices in what seemed an inexorable ascent, liquefied natural gas (LNG) became the fuel flavor of the moment. Long a sleeper technology, LNG suddenly looked like an economic winner. Applications for LNG terminals flowed into the Federal Energy Regulatory Commission (FERC), which regulates on-shore LNG facilities and gas pipelines. Projects also appeared at the U.S. Maritime Administration, which governs off-shore projects.

The flood of proposed projects predictably kicked off protests by folks living and working near the planned terminals. Locals raised the specter of terrorism, explosions, fires, and the like. It began to look like a reprise of the anti-nuclear movement of the 1970s and 1980s.

Since then, with domestic U.S. gas prices falling and demand for LNG in Europe growing, and drawing investment away from the U.S., LNG has largely dropped off of the U.S. energy debate agenda. LNG is unlikely to be a major player in 2009, although local protests against LNG projects will continue.

Last February, before the collapse of credit markets and the fall in oil and natural gas prices, CERA, which has been consistently bullish on LNG, scaled back its estimate for U.S. LNG imports. CERA’s Robert Ineson told an industry conference in Houston that the consultancy was cutting its prospects for U.S. LNG imports "from 3.2 billion cubic feet per day as of last fall to 2.6 bcfd now," a nearly 19% reduction. That was close to a contemporaneous EIA forecast of a 16% reduction in LNG imports for the year.

According to the EIA, some 40 LNG terminals planned for North America are now before FERC. Five terminals are now operating in the U.S., with one in Alaska exporting gas, according to the EIA, and four more likely to be operational by the start of 2009. This EIA forecast came in July 2008, when crude oil prices were over $140/barrel.

The EIA had yet to offer its wisdom on LNG while this story was coming together at the end of 2008, when crude prices fell below $47/barrel on Dec. 3. Few in the industry expect that the EIA estimate of four more new LNG terminals in service during 2008 is credible.

Renewable Projects Get a Second Wind

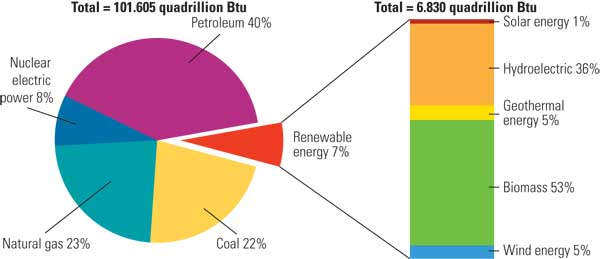

Renewable energy, particularly wind, has been the fastest growing electricity-generating technology in the past five years or so. Environmentalists and advocates for technologies to displace fossil fuels have long pushed wind and other renewables (but not politically incorrect hydro) as the answer to the question of how to cut U.S. greenhouse gas emissions while ensuring low-cost electricity (Figure 4).

4. Renewables are a growth industry. Renewable energy contributed 7% of total U.S. energy demand (and 8.4% of total U.S. electricity generation) in 2007, the last full year data is available from the EIA. The sum of components may not equal 100% due to independent rounding Source: Energy Information Administration

According to the American Wind Energy Association, the wind industry installed 1,389 MW of nameplate capacity in the third quarter of 2008, "bringing to 4,204 MW the total of wind power projects completed in what is expected to be another record year." With congressional wind production credits once again renewed (as part of the $700 billion bank bailout), 2009 looks to be another good year for wind.

But there’s a downside. Congress renewed the tax credits for another year only. That sets up a battle in the new Congress and creates uncertainty on the part of investors in renewable energy projects, which are mostly wind projects. It also reflects a concern that wind and solar, which drive up overall electricity prices, aren’t an economically sustainable answer to the need for new generation (see sidebar, "Wind Power Goes Mainstream").

The exponential growth in wind capacity seen in the U.S. comes from a tiny base, and wind remains a miniscule contributor to U.S. electricity supplies. The claims of wind and solar advocates that renewables can effectively replace baseload or even peak generation are overblown, according to many experts. Wind and solar are not dependable replacements for fossil-fueled generation, according to these critics.

A recent article by Carnegie Mellon University researchers Jay Apt, Lester B. Lave, and graduate student Sompop Pattanariynkool, in Issues in Science and Technology, lays out a powerful critique of renewables in general and the specific trend toward state (and potentially federal) renewable portfolio mandates. The summary of "A National Renewable Portfolio Standard? Not Practical," states, "Legislation that mandates specific electricity production from renewable sources paves a path to costly mistakes because it excludes other sources that can meet the country’s goals."

Renewable energy, say the article’s authors, "seems to addle the brains of many sensible people, leading them to propose policies that are bad engineering and science or have a foundation in a yearning for utopia."

A national renewable generating mandate, a goal of the incoming administration in Washington, they argue, is a bad idea for three reasons. First, "renewable" and "low greenhouse gas emissions" are not synonymous, as "there are several other practical and often less expensive ways to generate electricity with low CO 2 emissions." This is a veiled reference to "generating" what’s known as "negawatts" (a term coined by Amory Lovins) through energy conservation and energy efficiency. In fact, some utilities are negotiating with their regulators to add energy conservation project investments (such as projects that subsidize the replacement of older refrigerators with Energy Star models) to their rate base in order to earn a guaranteed rate of return. Whether regulators will put investments that promote end user conservation on the same footing as major generation construction projects remains to be seen.

Also, locations for wind and solar generation are generally far from the loads they must supply, leading to "unpopular and expensive transmission lines" to move the power to the market. Transmission lines that cross states but confer no local benefits have historically drawn intense opposition.

Finally, the Carnegie Mellon team argues, because it’s unlikely developers would build the needed transmission lines, a national market to allocate carbon reductions through trading would mean supply disruptions and cascading grid blackouts. "Renewable energy resources," says the report, "are a key part of the nation’s future, but wishful thinking does not provide an adequate foundation for public policy." A national renewable portfolio standard, says the report, "could cause a backlash that might doom renewable energy even in the areas where it is abundant and economical."

FBR Capital Markets analyst Kevin Book predicts that the 111th Congress, probably in 2010, will approve some form of carbon dioxide regulation. The legislation, he told reporters recently, will be enacted not because the carbon restraint will change behavior. Rather, he argued, it will be enacted because the regulation — cap-and-trade, carbon tax, or whatever one choose to call the surcharge on fossil-fueled energy — will be a way for the federal government to raise money. It will be, in short, a new tax.

What do all these indicators mean for U.S. electricity supply? As in the recent past, it looks as if the industry will continue muddling through. It may see advancement in infrastructure investment, significant new generation, or new technology development. But it also faces the possibility that the policies necessary to achieving those goals will not materialize, for political and economic reasons. In the words of the 1970s disco group the Bee Gees, in the splendid film Saturday Night Fever, it’s likely to be a case of "Stayin’ alive, stayin’ alive."