"It’s déjà vu all over again," said Yogi Berra. The Hall of Fame catcher could easily have been predicting the coming resurgence of natural gas – fired generation. Yes, a few more coal plants will be completed this year, but don’t expect any new plant announcements. A couple of nuclear plants may actually break ground, but don’t hold your breath. Many more wind turbines will dot the landscape as renewable portfolio standards dictate resource planning, but their peak generation contribution will be small. The dash for gas in the U.S. has begun, again.

"Holy cow, there’s a lot of gas."

That was the reaction of Penn State geologist Terry Engelder, as reported in the Massachusetts Institute of Technology’s Technology Review last October. Three years ago, Engelder was asked to assess the natural gas potential of Marcellus shale deposits in the U.S. Midwest and Mid-Atlantic regions. It now appears that deep shale beds — the Carboniferous (350 million years ago) Barnett shale deposits in the Texas and the enormous Devonian (400 million years ago) Marcellus shale deposits in the East — could be game-changers in the U.S. energy and power generation markets for years to come.

Shale formed in those deposits contained methane bound so tightly into the rock formations that conventional drilling technology could not get at it, according to the geologists. That’s changed. Deep drilling, horizontal drilling, and hydraulic fracturing (pumping water down the borehole at great pressures to shatter the shale strata, releasing the methane from the rock) make the gas accessible. Both shale finds are providing drillers with gas bonanzas.

Record Gas Reserves Discovered

Last June, the U.S. Potential Gas Committee (PGC) issued a report (links to this and other resources are provided in the sidebar at the end of this article) that estimated total U.S. natural gas reserves at over 1,800 trillion cubic feet, the highest in the committee’s 44-year history, and 40% above its 2006 estimate. John Curtis of the Colorado School of Mines, head of the PGC, said that the estimate "reaffirms the committee’s conviction that abundant, recoverable natural gas resources exist within our borders, both onshore and offshore, in all types of reservoirs." Prices fell, reflecting the optimistic supply predictions. Exploration in shale deposits continued growing.

The PGC is an independent, industry-funded technical group that examines natural gas reserves in the U.S. Said Curtis, "Our knowledge of the geological endowment of technically recoverable gas continues to improve with each assessment. Furthermore, new and advanced exploration, well drilling, and completion technologies are allowing us increasingly better access to domestic gas resources — especially ‘unconventional’ gas — which, not all that long ago, were considered impractical or uneconomical to pursue." That’s a reference to shale gas, as well as gas in deep deposits.

Significantly, the shale gas deposits are close to, and in some cases, directly underneath, natural gas pipelines and gathering hubs and near large markets. Bringing the gas to market could be easy and cheap (see the sidebar, "Say Goodbye, LNG?").

In a press release, the PGC noted, "When the PGC’s results are combined with the U.S. Department of Energy’s latest available determination of proved gas reserves, 238 Tcf [trillion cubic feet] as of year-end 2007, the United States has a total available future supply of 2,074 Tcf, an increase of 542 Tcf over the previous evaluation."

That’s a stunning figure — an increase of over 25% above previous estimates. The Energy Information Administration (EIA) defines "proved reserves" as "those volumes of oil and natural gas that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions." In other words, they are real.

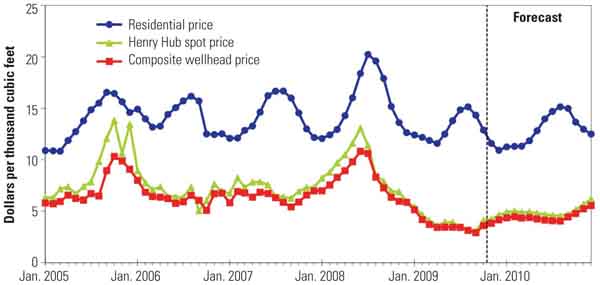

The supply optimism is good news for existing and potential electric generators, as the projections, bolstered by successful drilling in shale, have resulted in dramatically lower natural gas prices. The most recent reports from the EIA found natural gas prices at the Henry Hub at $2.76 per million Btu (mmBtu). Futures prices at the New York Mercantile Exchange for September 2009 contracts were at $2.91 per mmBtu. A couple of years ago, the NYMEX price was in the $9 range for short forward contracts (Figure 1).

1. Gas prices expected to stabilize in 2010. The U.S. Energy Information Administration (EIA) predicts natural gas prices will fluctuate less and be more predictable in the future given the significant increase in gas reserves. Source: EIA November 2009 Short-Term Energy Outlook

Favorite Fuel Returns

For 2010, gas sees its prospects gaining in the power market, bolstered by new technology and large new supplies. The leader of the generating pack in the 1980s and early 1990s, gas went into a deep decline on high prices and diminishing reserves in the first part of the 21st century. Many analysts said the days of gas as a major generating fuel were over.

No more. Given that gas is less polluting than coal (by any measure), produces half as much carbon dioxide (CO2) per unit of energy output, and requires plants that are quick to build and not capital-intensive, new gas reserves appear to position the fuel as a winner in generating markets. The U.S., once seen as a declining gas producer, may be a world leader in gas.

In November, The Energy Daily (a sister publication of POWER) reported that the North American Electric Reliability Corp. (NERC) has found that "Electric utilities are increasingly showing an ‘overwhelming’ preference for building natural gas – fueled plants, a trend that is expected to drive gas past coal as the dominant North American fuel for on-peak power production by 2011." According to the newsletter, "NERC said both regulated utilities and merchant generators are increasingly favoring gas plants because the fuel has been discovered in more abundance and is cheaper than in the past. In addition, gas plants are easy to site, can be built quickly and produce less carbon emissions than other types of traditional generation."

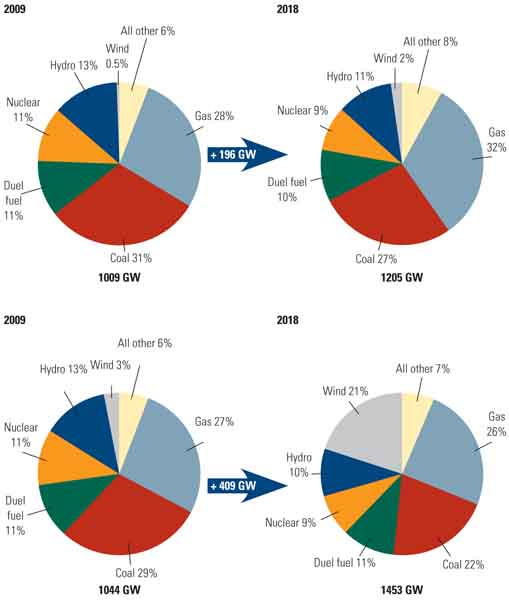

This overabundance of natural gas reserves may also have a downside, according to a report released by NERC on October 29. NERC’s "2009 Long-Term Reliability Assessment 2009 – 2018" notes that natural gas – fired on-peak power production may push past coal-fired generation by 2011, portending system reliability problems. NERC also cited cyber-security concerns, the integration of fast-growing renewable resources into the grid, and uncertainties created by the economic slowdown as emerging reliability worries that it faces (Figure 2).

2. Demand for electricity will rise in 2010. The top pie charts describe the expected growth of capacity that will be available during peak hours. The bottom pair describe the expected growth of installed capacity. Coal and gas will continue to be the fuels of choice during peak generating hours. Wind generation will continue to grow faster than any other type but will contribute little to peak supplies. Source: NERC

NERC recognized that existing reserve margins are adequate across the U.S. for the next few years, but the first priority must be to expand the grid and increase the capacity of existing transmission and distribution systems to handle the expected growth of renewable generation. The report concluded, "More than 11,000 miles (or 35%) of transmission (200 kV and above) proposed and projected in this report must be developed on time to ensure reliability over the next 5 years. 32,000 miles of transmission (200 kV and above) are projected for construction from 2009 to 2013 overall." NERC strongly believes that transmission siting and construction is the most urgent issue for the power generation industry, now and well into the future.

Electricity growth has stalled over the past two years, given the chaos in the global economy. However, NERC projects that demand will increase 15% between 2009 and 2018, compared to its 17% forecast in last year’s report. The projected demand increase has steadily decreased over the past several years. Once again, NERC underlined the need for grid expansion and new transmission capacity to handle renewables and ensure reliability, with particular urgency seen in areas of the Southwest.

"These competitive advantages have resulted in an overwhelming preference for [gas] over the ten-year period, as installed natural gas capacity is projected to increase 38 percent over the ten-year period, while coal is projected to increase by only 6 percent," NERC’s assessment said. Its predictions of demand for new generation have been overly generous in the past but now appear to be more realistic (see table). The EIA predictions of electricity demand growth do not include peak demand growth as a separate category, but rather predict energy consumption will grow 8.2% through 2018. Together, the NERC and EIA data clearly show that the need for additional, dispatchable load during on-peak hours will be a primary focus for electricity system planners. Expect more gas-fired reciprocating engine and combined-cycle plants designed for intermediate peaking service to be announced in the coming year.

Electricity use increases, slowly. The North American Electric Reliability Corp. (NERC) expects the rate of peak demand and energy consumption growth to slow in coming years. Source: NERC

Further, NERC said that "on-peak natural gas capacity is projected to grow by more than double the amount of any other resource, and by more than five times any other resource when dual fuel resources (primarily fired by natural gas and another, alternate fuel) are excluded." NERC said a "plausible" future scenario involves flat or negative power demand growth for the next seven or eight years, followed by an "abrupt change to normal or high demand growth."

From NERC’s perspective, however, that trend is not all good. NERC said the growing reliance on gas could create grid problems if gas usage strains the infrastructure that delivers gas to power plants. "The projected growing reliance on natural gas increases the potential for adverse reliability impacts due to fuel supply and storage and delivery infrastructure adequacy issues," NERC said.

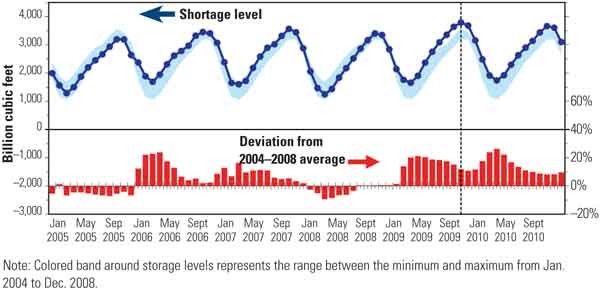

Increased gas demand this past summer already put a strain on existing gas transmission infrastructure. Chesapeake Energy Corp. admitted that it briefly slowed production because natural gas pipelines and gathering systems were already operating at maximum capacity (Figure 3).

3. Gas storage and pipelines full in 2010. An excess of natural gas is packing gas lines and storage facilities. Shown is the predicted rate of natural gas storage for 2010 compared to historic amounts. Source: EIA November 2009 Short-Term Energy Outlook

I Told You So

"I used to say we were awash in gas," crows Oklahoma petroleum geologist and gas guru Bob Hefner. "Now I say we are drowning in it." The ebullient Hefner, 74, with a long tradition of gambling big on gas, is now a bastion of the eastern energy establishment. He is associated with the Belfer Center for Science and International Affairs at Harvard’s Kennedy School of Government. He wears bow ties and tuxedo jackets with his Levis and cowboy boots, and underwrites Asian cultural projects with his Singaporean wife, Meili.

In the 1960s, Hefner, a technological optimist of the first degree, proposed deep drilling for natural gas, arguing that the gas resources in the U.S. had barely been touched. In 1969, according to Oklahoma State University, Hefner’s "Number One Green well, drilled to a depth of 24,454 feet in Beckham County, blew in at the highest pressure ever recorded."

Since then, oil and gas exploration and drilling technology have evolved so that seismic analysis can provide a clearer view of the subterranean landscape. Directional drilling technology and hydro fracturing can reach and exploit the most promising strata. There’s a stunning amount of gas down there, say the experts, and it’s getting easier to develop.

Gas-rich shale deposits are not confined to North America. A recent New York Times article noted that petroleum engineers from around the world have come to the U.S. to learn about exploiting natural gas from shale. Amy Myers Jaffe, an energy expert at Rice University in Texas, told the newspaper, "It’s a breakout play that is going to identify gigantic resources around the world. That will change the geopolitics of natural gas."

Little Will Be Built in 2010

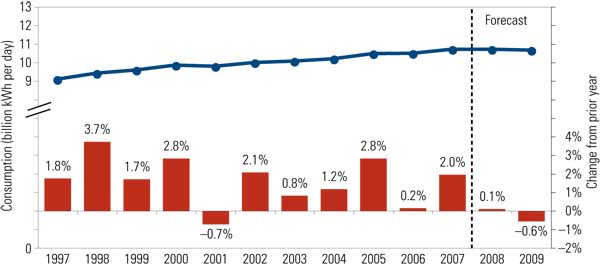

As we enter the second decade of the 21st century and a second year of avoiding an economic collapse, the U.S. business climate seems to have become more positive. A growing sense of cautious optimism is appearing. A mid-October survey by the National Association for Business Economics concluded that the largest recession since the 1930s Great Depression is over, and economic growth is likely for the U.S. economy in 2010. The government announced that third-quarter 2009 economic growth hit 3.5%, the first positive growth in five quarters, suggesting an end to the recession (Figure 4).

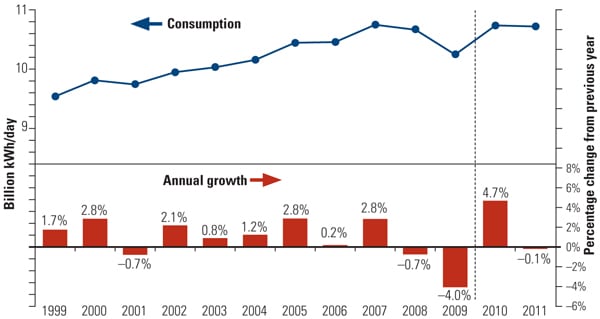

4. Electricity growth resumes in 2010. After a two-year contracting market, total electricity consumption in the U.S. in 2010 is expected to increase. Source: EIA, November 2009 Short-Term Energy Outlook

The implications for electric generation are mixed. What gets built depends on a complex stew of credit markets, regulatory responses, economic growth, technology, and national politics. Some of those are leading economic indicators, some lagging, some not clear at all.

Advocates of renewable generation appear not to have made a convincing economic case in the market. But they have politically. Coal and nuclear continue to take a political battering at the hands of the renewables advocates. The politics of energy appear not to have factored in to the new implications of natural gas. The political and regulatory landscape is a dog’s dinner (a Britishism for an undigested mess).

The need for new generation to supply load appears less urgent than in previous years. According to the EIA, demand for electricity has fallen since the economy tanked in 2008. The demand down-tick is the first since the EIA has accumulated these statistics, when it was created in 1977.

Facing a sluggish economy, consumers have lowered thermostats, cut off air conditioning, and dialed down appliances, leading to the decline in electricity demand. A cool 2009 summer in most of the U.S. helped to reduce air conditioning load. Net electric generation dropped 6.8% from June 2008 to June 2009. That was the 11th consecutive month that electric generation slid downward, compared to the same month in the prior year.

Analysts say they expect the declining demand trend to reverse when economic growth shows up at the beginning of 2010 or thereabouts. But they have been wrong before and may be wrong again. The EIA, the U.S. Department of Energy’s statistical agency, says it suspects the decline in demand will continue into early 2010, despite what appears to be a bottoming-out of the recession.

Many electric power company long-term capital spending plans have been built on the dire forecasts of the past decade, particularly from NERC. For years, the conventional wisdom in the generating industry was that the U.S. was running out of generating capacity. Year after year NERC had the same message: It’s time to build baseload, particularly nuclear and coal, and make major investments in high-voltage transmission.

Maybe not. Intermediate-load and peaking units, suggesting new gas plants, may be the ways to hedge big investment bets on future baseload units. A recent Washington Post article quoted anonymous sources as saying that new nuclear plants aren’t economical until natural gas prices are above $7/mmBtu. That’s more than double the current price.

The urgency for long-distance, high-voltage electric transmission investment, premised on optimistic estimates of growth in demand, also seems to have declined. Capital requirements for the big transmission projects, along with the political risks, have scared off investors, including conventional utilities and free-standing investment companies. Those who want to build large transmission systems linking areas of surplus power generation (West Virginia, for example) to big markets in New Jersey and New York are facing not only citizen opposition but also indifference from Wall Street investors, who don’t see an acceptable market return on investment (Figure 5).

5. New transmission is key in future years. The North American Electric Reliability Corp. predicts that expanding critical transmission capacity will be a national priority over the next five years. Source: NERC

The bullish generating market in late 2008 — despite signals of a worldwide economic crisis — turned into a financial quagmire. Today, lenders are unwilling to pony up cash for new generation and transmission without guaranteed returns, regulators are reluctant to bless projects without iron-clad promises of stable prices, and customers are unwilling to support new projects that threaten rate hikes and environmental impairment. Governments at the federal and state level are demonstrating distinct ambiguity about generation and transmission projects.

Where does that land us? Overall, the generating market has slowed. Raising credit has become difficult for major projects of any kind, from new nuclear reactors to petroleum refineries to coal mines. Money wasn’t a problem a decade ago. Today, it’s a big problem. Tomorrow, meaning 2010 and beyond, that may change. But don’t bet the company. It’s a jungle out there.

The Nuclear Godot

Nuclear power remains the last best hope for zero-carbon emissions from baseload generating plants and was many analysts’ early pick for a generating revival in the first decade of the 21st century. If one accepts the conventional view of climate change, the rational case for nukes appears unassailable. If you want low-carbon generation, you must go nuclear.

The first decade of our new century has passed. After years of waiting for the nuclear renaissance, it doesn’t look as if the second decade will bring the nuclear industry closer to revival. Indeed, the horizon may be receding. Literature Nobel laureate Samuel Becket could not have had U.S. nukes in mind when he wrote his iconic 1953 play Waiting for Godot. But some of its dialog is eerily on target. The character Vladimir in the second act comments, "What are we doing here, that is the question. And we are blessed in this, that we happen to know the answer. Yes, in this immense confusion one thing alone is clear. We are waiting for Godot to come."

In the U.S., we are into the second decade of the 21s century, waiting for the nuclear renaissance, after the market collapsed in the 1970s. Waiting and waiting.

Nuclear power plants won’t pick up U.S. generating market share in 2010, by all accounts. That’s despite prior federal government policy aimed at jump-starting new nuclear generation, including allegedly streamlined federal regulations and a longed-for candy jar of additional subsidies, such as major loan guarantees, pledged in the Republicans’ Energy Policy Act of 2005. Those have yet to materialize.

Some in the Obama administration and Congress are contemplating additional loan guarantees and other nuclear subsidies, to be included in pending climate change legislation. Arguing for $50 billion in additional federal loan guarantees, Exelon CEO John Rowe told a Senate committee in late October, "Deployment of new nuclear plants simply will not happen, given the large up-front capital costs, without a much more robust federal loan guarantee program than currently exists." There doesn’t seem to be much enthusiasm on either side of the partisan aisle for committing that kind of money to nuclear power.

The 2005 congressional vision (perhaps a hallucination) was of a modest new fleet of nukes — a dozen or so — that would come into the U.S. market and revitalize the stagnant industry. New reactor designs from U.S., Japanese, and French companies; interest from multiple utilities; applications for more than 30 units under the streamlined approach of the Nuclear Regulatory Commission’s (NRC) licensing reforms of the 1990s; and the Energy Policy Act of 2005 all led to irrational exuberance among nuclear power developers. The 2005 loan guarantees would jump-start the market, the legislation assumed and the industry agreed.

More than four years later, the presumably vibrant market for new nukes in the U.S. is becalmed at best. That’s a factor of the worldwide economic collapse of 2007 – 2009, combined with U.S. regulatory and technical difficulties afflicting the new, putatively safer and more efficient nuclear reactors, plus the industry’s inability to deliver on promises of new reactor designs that will be easier, quicker, and cheaper to build. Then there is the unwillingness of anyone with real money to finance new plants.

The NRC has been unable to certify the latest new reactor designs under its "combined operating license" reform, for reasons indicting both the industry and the regulators. The French AREVA evolutionary design is facing its first round of NRC scrutiny while experiencing major cost overruns and schedule delays in construction of a new unit in Finland. U.S. regulators at the end of the year rejected a modified advanced reactor design from Westinghouse for the AP1000 that they had earlier approved. Westinghouse made changes in the shield building to protect the reactor from airline strikes, earthquakes, hurricanes, and tornadoes. The NRC said those changes raised new licensing issues. General Electric, according to the NRC, never provided design details for its advanced boiling water reactor sufficient to judge the safety of the machine (Figure 6).

6. New nuclear queue grows. The location of planned new nuclear plants in the U.S. Source: U.S. Nuclear Regulatory Commission

Given regulatory uncertainty and the conditions of current capital markets, no rational investor is likely to commit major private-sector resources to building new nuclear plants, according to several investment bankers who talked to POWER on background. If new nukes are to be built, they argued, the effort will require large commitments of federal dollars, probably in the form of loan guarantees vastly exceeding those in the 2005 act. That’s an unlikely prospect. Even with much larger federal loan guarantees, it isn’t clear that Wall Street will commit the capital necessary to build units at $8 billion to $10 billion a pop, the latest estimates.

In Congress, feckless Republicans are calling for a fleet of 100 new nukes within 20 years, at a $700 billion price tag. That’s pure politics, or else they are smoking some powerfully atomic wacky-weed that induces weird policy visions. There is no U.S. capacity to license or build that many plants. Maybe the system could support three, or six, new nukes, but that’s a guess. A hundred? Fugetaboutit.

Waste Storage Discussions: A Waste of Time. Another blow to the prospects for U.S. nukes was the White House decision last year — no surprise — to euthanize the Yucca Mountain, Nev., project for permanent underground storage of spent nuclear fuel and other high-level nuclear wastes. The Obama administration, fulfilling a deal with Senate Democratic Majority Leader Harry Reid of Nevada, zeroed out Yucca in its budget submission early in 2009. The funding decision will stick. Sic transit gloria Yucca.

The U.S. finds itself in the embarrassing position, not for the first time, of having no practical idea about nuclear waste storage. Spent fuel rods will remain at reactor sites for the unforeseeable future, probably past the lifetime of anyone reading this article. In the wake of the administration’s decision, the NRC last September began a rulemaking that would give regulators the authority to approve at-reactor waste storage for 40 years, up from the current limit of 20 years.

The administration says it will appoint a "blue-ribbon" commission to study options for nuclear waste disposal. That’s classic D.C. talk for, "We are clueless."

Nuclear Merger. The only positive glow for nukes was the NRC decision last October to allow Electricité de France (EDF) to buy a major share of Constellation Energy’s two-unit Calvert Cliffs nuclear plant. Baltimore-based Constellation, swimming upstream against most energy analyses, and burdened with a heavy load of debt, wants to build new (merchant) nuclear capacity at its existing Calvert Cliffs, Md., site. The only way that can happen, Constellation admits, is if it has access to EDF’s deep financial pockets, which reach into the French government’s endless treasury.

The Constellation-EDF deal won Maryland Public Service Commission approval at the end of October, but with caveats, including a commitment to invest $250 million in the company’s distribution company, Baltimore Gas and Electric (BG&E), and a $100 rate rebate to every BG&E customer, a one-time, $110 million hit for the merged company. Constellation has agreed to those conditions.

Other than the Constellation-EDF parlay, U.S. nuclear projects appear to be waiting for the nuclear Godot that will lead them into a new day of robust construction and profitable prospects. We’ve seen that play before. As Becket’s Vladimir says to Estragon, "On the other hand what’s the good of losing heart now, that’s what I say. We should have thought of it a million years ago, in the nineties."

Skyrocketing Costs Dampen Enthusiasm. At the end of October, the San Antonio City Council was stunned to learn that the price tag of the two new reactors at the existing South Texas Project (STP) had increased by $4 billion. The two existing reactors at STP are owned by NRG Energy (44%); CPS Energy (40%); and Austin Energy, the municipal utility of Austin, Texas (16%), although the San Antonio municipal utility had recently reduced its share in the two new nuclear projects to 20%, effectively leaving 20% of the plant unsold. CPS Energy is responsible for finding a buyer for that 20% slice of the project.

According to a knowledgeable source, the new cost estimate from the project’s primary contractor, Toshiba, is up to $4 billion higher than estimates made public by CPS in late July, which predicted a project cost of $10 billion, or $13 billion including financing.

The fate of the new units at STP is being closely followed by the industry as the STP new addition is one of only three nuclear projects that the Energy Department selected in 2009 to receive a federal loan guarantee, which will cover a good portion of the plant financing costs. NRG Energy has said it also will seek financing help from Japanese export agencies due to the role of Toshiba and other Japanese firms in the project.

The STP project would also benefit from a legislative change that the Nuclear Energy Institute (NEI) is pushing to Congress. That change would let municipal nuclear plant owners (like CPS) transfer nuclear production tax credits to private sector partners (like NRG Energy). Because munis are tax-exempt, the credits would otherwise go to waste.

The San Antonio City Council isn’t the only prospective plant owner struggling with jaw-dropping cost estimate increases. Florida Power & Light’s Turkey Point addition of two new 1,100-MW units is said to cost between $12 billion and $18 billion, Duke Energy’s Lee Nuclear Plant was last estimated at $11 billion for two 1,100-MW units at a "greenfield" plant (the estimate, by Duke in June 2009, was quoted in 2008 dollars), and Georgia Power’s two new units at Plant Vogtle are estimated at $14 billion.

The rising construction costs for new nuclear power do not necessarily translate into rates that are uncompetitive with other technologies in the future. In a commentary published in The Energy Daily, Richard J. Myers, vice president of policy development at the NEI, made the case that new nuclear plants can be cost competitive:

The National Research Council’s recent analysis shows a 6 – 13¢/kilowatt-hour (kWh) cost range for new nuclear plants. The low end represents a nuclear plant financed through the DOE’s loan guarantee program. This is better than coal-fired capacity with carbon capture and storage (CCS) at 9 – 15¢/kWh, and significantly more stable than gas-fired combined-cycle generation, which could be the lowest- or the highest-cost option, with a range from 4¢/kWh (unrealistically low gas prices, no carbon controls) up to 21¢/kWh with high gas prices and CCS.

Using the capital cost assumptions built into its annual energy outlook, the Energy Information Administration calculates that new nuclear will have a levelized capital cost of $107.30/MWh in 2016. Advanced coal with CCS is at $122.60/MWh; gas-fired combined cycle at $115.70/MWh; onshore wind at $141.50/MWh (cost of gas-fired back-up power not included).

In the 2009 update to its 2003 report, The Future of Nuclear Power, the Massachusetts Institute of Technology shows nuclear energy at 6.6¢/kWh absent the "technology risk premium" (i.e., when the first few plants have been built). Coal-fired and gas-fired plants are at 6.2¢/kWh and 6.5¢/kWh without CCS, 8.3¢/kWh and 7.5¢/kWh with carbon controls, respectively.

Slow but Steady: King Coal Keeps on Keepin’ on

Then there is coal, the Rodney Dangerfield of generation: It just doesn’t get any respect. Surprise: New coal-fired projects, unlike the nukes, are actually under construction in the U.S., and some are likely to start pushing out power soon. Despite deep political opposition from environmentalists and competing technologies, coal still generates more than half of all U.S. electricity. It’s a reminder of Billy Joe Shaver’s 1950s bluegrass hit, "I’m just an old lump of coal (but I’m going to be a diamond someday)."

According to the Department of Energy’s National Energy Technology Laboratory, in June 2009, 36 coal-fired plants were either under construction (23), near construction (4), or permitted (9), for a total of 19.4 GW of new capacity. That’s in the face of a heavy assault on coal by environmental groups concerned with carbon dioxide emissions. Also joining the no-coal chorus in Appalachia are local opponents of mountain-top mining and others challenging coal ash waste disposal at power plants, in light of the Tennessee Valley Authority’s 2008 major ash dam collapse.

Not all of those coal plants the EIA identified will actually join the grid. It’s not a walk in the generating park. For example, in November, MDU Resources Group Inc. announced it was canceling its planned 600-MW Big Stone II coal project in South Dakota. The reason was that its partners in the project were unwilling to pony up the cash for the plant. But some new coal projects will succeed, as coal continues to be the pragmatic least-cost approach to baseload power.

Financial results demonstrate coal’s staying power. West Virginia – based Massey Energy Co., the fifth-largest U.S. coal producer, and the largest producer of central Appalachian coal, at the end of October reported profits for the third quarter of 2009 of $16.5 billion (19 cents per share) on revenues of $536 million, a bit below third quarter 2008 figures. For the first nine months of 2009, Massey’s EBITDA (earnings before interest, taxes, depreciation, and amortization) was $374 million, compared to $242 million for the first three quarters of 2008. This is not the picture of a dying industry.

Coal has many overt enemies but also lots of grassroots support. Miners and other union workers in the industry support the dusky diamonds ("dirt that burns," as some have described the mineral). Coal mining, both underground and on the surface, creates high-paying jobs in places where there often are few other opportunities for work. Those jobs translate into economically viable communities, as miners and their families support local businesses from grocery stores to car dealers to dentists. In southwestern West Virginia and eastern Kentucky, flat land is hard to find, and mountain-top removal has plenty of friends, not just miners but also business folks and local consumers. That translates into political power for coal-state politicians.

Will generating and anti-pollution technologies impact the coal equation? Industry hype about coal claims it can be "clean," citing as-yet-unproven technologies for gasification, carbon capture, and CO2 sequestration. At the same time, environmentalists claim that "clean coal" is an oxymoron, akin to "military intelligence." Neither side has made its case. Nor is it likely the verdict will come in 2010.

The coal industry and the DOE are subsidizing projects to strip CO2 out of coal-fired plants and stuff the greenhouse gas into places yet untested. Carbon dioxide, of course, was once thought to be a beneficial byproduct of burning coal. Now, quite the opposite.

So far, nothing in the world of capturing CO2 from coal and storing it somewhere else approaches commercial scale. Indeed, some analysts are suggesting that coal plants should not be the major focus of attempts to reduce U.S. CO2 emissions. Instead, they argue, as reported in a fine New York Times article, there are more emissions bangs for the buck in working on capturing CO2 at "oil refineries, chemical plants, cement factories and ethanol plants, which emit a far purer stream of it than a coal smokestack does."

Look for further carbon capture technology research in 2010. This technology is a long way from commercial development and may slow investment in further large-scale coal plant projects in the year ahead.

Congressional energy legislation in 2010 could pressure coal, as Congress searches for ways to reduce greenhouse gases. Those political moves against coal may prove quixotic. Coal is too powerful in Congress to take a major hit. In addition to generating 55% of U.S. electricity, coal is found (although not necessarily mined) in more than half of the U.S. states and used to generate electricity in far more than those. Coal has major political muscle in both business and labor camps.

The new head of the AFL-CIO, Rich Trumka, former chief of the United Mine Workers of America, is a western Pennsylvania coal miner who worked his way through college and law school with a miner’s helmet and lamp on his head. It’s unlikely coal will see its business or political position eroded in the year ahead if the savvy Trumka has anything to do with it. There’s a good bet he will be behind the political stage and helping to direct the drama.

The Green Machines

It isn’t clear these days which technologies — coal or nukes or water — are the environmental movement’s true bête noir (dark beast). Nukes are out of the question for some because of waste. Coal attracts loathing because of conventional pollution, CO2 emissions, and land-use issues. Hydro kills trout and smaller fish you have never heard of.

What’s left are wind, solar, biomass, geothermal, and conservation (and who can argue with conservation?).

Niche generation, widely known as "renewable energy," a term without a rigorous definition, accounted for about 8% of U.S. energy consumption in 2008, according to the EIA. That portion of the market should grow in 2010. Renewables may be able to increase their market share through state renewable energy portfolio standards and various state and federal subsidies. Any federal legislation mandating a renewable standard would be unlikely to have any impact in 2010 or 2011.

The self-proclaimed "green" generating technologies will continue to occupy small market opportunities, not supplanting conventional baseload generation such as coal and nuclear, or dispatchable generation such as coal, hydro, and gas. That’s clear from government statistics.

What is renewable? The definition is important. Many environmentalists conveniently ignore large hydropower as "renewable," an omission that makes some political-correctness sense (the opponents of hydro don’t like turbine blades that kill fish). Historically, some of the environmental movement’s deepest roots — those connected to John Muir and David Brower — are intimately bound to opposition to hydroelectricity dams. Hydro is, for these folks, out of the question when it comes to substantial energy generation.

Eschewing water power is nonsense in terms of renewable electric capacity. The EIA says that of the 372 billion kWh of generation from renewables in 2008, 248 billion kWh came from "conventional" hydroelectricity, meaning big water such as Hoover Dam, Glen Canyon, the Missouri River system, the Columbia River system, the Lower Colorado River Authority, and others. By contrast, wind, the next-largest contributor to renewable generation, provided only 52 billion kWh. Solar checked in at a tiny 843 million kWh, last place among the EIA renewable technologies.

Wind and solar will continue to grow exponentially in 2010. That’s easy. They start from a very low base, so exponential growth remains trivial. Will wind and solar make major contributions to electric generation and electric supply in 2010 and displace statistically significant amounts of fossil generation? The chances are slim and none. Slim just left the room.

Which Way Is Wind Blowing? The American Wind Energy Association (AWEA), the Washington lobby for wind power, reported that its industry installed some 1,200 MW of new capacity in the U.S. in the second quarter of 2009. That’s a solid performance, bringing the wind total for the first six months of 2009 to 4,000 MW, well ahead of the first six months of 2008. In a press release, AWEA acknowledged that it is "seeing a reduced number of orders and lower level of activity in manufacturing of wind turbines and their components." AWEA said this is "troubling in view of the fact that the U.S. industry was previously on track for much larger growth."

However, translating pure installed capacity into useful generation leaves much to be desired. The Electric Reliability Council of Texas (ERCOT), where wind turbine construction leads the world, now sports 10% of its installed capacity as wind against 65% natural gas. ERCOT’s annual summer assessment noted that there are 8,135 MW of installed wind capacity. However, when calculating the portion of that capacity that is available to help manage peak demand, ERCOT takes a very pragmatic view: "For summer peak capacity, ERCOT counts 8.7 percent of wind nameplate capacity as dependable capacity at peak in accordance with ERCOT’s stakeholder-adopted methodology." So for every 1,000 MW of wind power installed, only 87 MW are predicted as available to trim the summer peak. ERCOT’s installed generation capability is 72,700 MW. A summer peak demand of 64,056 MW is predicted for 2010.

The wind supply chain, noted AWEA, is experiencing troubles as companies "have stopped hiring or have furloughed employees due to the slowdown in contracts for wind turbines. Wind turbine component manufacturing investment was one of the bright spots in the economy in 2008, with over 55 facilities added, expanded or announced that year." No more, it appears.

Denise Bode, AWEA’s CEO, said, "Manufacturing investment is the canary in the mine, and shows that the future of wind power in this country is very bright but still far from certain. The reality is that if the nation doesn’t have a firm, long-term renewable energy policy in place, large global companies and small businesses alike will hold back on their manufacturing investment decisions or invest overseas, in countries like China that are soaring ahead."

Deconstructing Bode’s canary metaphor, if the future of the U.S industry is bright, the canary must be doing quite well, and singing gleefully. It doesn’t appear that the canary is gasping for air in her scenario, although the implication of her statement is that Tweety Bird has a raspy cough. The windy canary, it seems, is neither a positive nor a negative indicator.

One of Bode’s previous jobs was serving as head of a lobbying group promoting natural gas, a product that will kill canaries quite quickly (and people, too, under the right circumstances). Her AWEA statement is further evidence that Washington lobby-speak is often incoherent.

Scoping out wind’s prospects, Shane Mullins of Industrial Info Resources (IIR) said in late September, "After a record-setting year in 2008, wind power is on target for a mediocre 2009, but prospects for 2010 and beyond are extremely bright. Last year was a great year for wind power installations, so good, in fact, that a lot of projects scheduled for construction in 2009 were pulled into 2008. But last year’s collapse of the tax equity market cut new wind construction in half."

In 2008, said Mullins, construction began on more than 9,000 MW of new wind power capacity in the U.S., but through mid-September 2009, construction had begun on only 4,162 MW of new wind projects, according to data collected by IIR. "For all of 2009, we’ll be lucky if we see construction begin on a total of 4,500 MW of new wind projects," said Mullins. For 2010, who knows?

Slow Slog on the Solar Road. Solar electric generation has become the stepchild of politically correct renewables. While wind has boomed, relative to its starting position, solar has seen a much slower path to gaining market share and much less attention in the news media. Solar’s consistent problem has been cost. With generous subsidies and tax benefits, wind has reduced its nominal (including subsidies) upfront costs to below those of coal and nuclear. No so for sun power.

Solar energy, both photovoltaic (PV) and thermal, has seen capital cost reductions. A recent Lawrence Berkeley National Laboratory study of grid-connected solar PV technology found a substantial trend of cost reductions, averaging over 3% per year for a decade, mostly driven by government subsidies. But the starting point was so high that the solar generating technologies remain uneconomical for most uses.

A McKinsey and Co. analysis of solar’s prospects is cautiously bullish about the sun. Says the review, "A new era for solar power is approaching. Long derided as uneconomic, it is gaining ground as technologies improve and the cost of traditional energy sources rises. Within three to seven years, unsubsidized solar power could cost no more to end customers in many markets, such as California and Italy, than electricity generated by fossil fuels or by renewable alternatives to solar. By 2020, global installed solar capacity could be 20 to 40 times its level today."

But the McKinsey report, featuring its conditional verb — "could" — notes that the technology is starting from a tiny base and "is still in its infancy. Even if all of the forecast growth occurs, solar energy will represent only about 3 to 6 percent of installed electricity generation capacity, or 1.5 to 3 percent of output in 2020." The places that McKinsey projects solar could be competitive are already extremely high-priced markets.

Unexpected Trend: Fuel Switching

When the Acid Rain Program under the Clean Air Act took effect in 1995, utilities searched for ways to avoid installing expensive flue gas desulfurization systems. One approach much favored by plants in the eastern U.S. was to perform a boiler fuel switch from high-sulfur eastern bituminous coal to low-sulfur Powder River Basin coal. A side benefit was that the coal was significantly less expensive to purchase, even if the delivery charges were much higher given where the coal is mined. Today, with the nation expected to be awash in natural gas, several utilities have announced plans to, in essence, fuel switch from coal to natural gas.

A good example is Progress Energy Carolinas’ August announcement of its plans to permanently shut down three coal-fired power plants near Goldsboro and, in exchange, construct a new, high-efficiency, gas-fired 950-MW combined-cycle power plant. The business case for the fuel switch is compelling. The utility gets bragging rights, not to mention emissions credits, for shuttering three coal plants totaling almost 400 MW at the H.F. Lee Plant in Wayne County. The utility makes a compelling case that its plan will reduce overall emissions (including those of CO2, should carbon controls eventually become law), increase the efficiency of electricity production in its system, and, if natural gas prices remain low, lower the cost of electricity production. The cost of the new intermediate-load plant, expected to be in service by 2013, is estimated to be around $900 million.

A final advantage to Progress Energy: Adding a natural gas – fired plant will broaden the company’s fuel resource base away from coal and nuclear. As a side benefit, shuttering the older three plants sidesteps the requirements of North Carolina’s Clean Smokestacks Act, which established very aggressive emission-reduction targets in 2013. Instead of cleaning up the old plant, Progress Energy decided it was wiser to invest the money in a new plant.

"This is an important milestone for our company and for our state," said Lloyd Yates, president and CEO of Progress Energy Carolinas. "The Lee Plant has been producing electricity reliably and cost-effectively for our customers for more than 50 years, but as emission targets continue to change, and as legislation to reduce carbon emissions appears likely, we believe in this case, it’s in the best interest of our customers to invest in advanced-design, cleaner-burning generation for the future."

Yates went on to say, "Our objective is to maintain the right balance of resources — nuclear, natural gas, coal, hydroelectric, solar, biomass, and energy efficiency — to make our company and state more energy independent and to minimize the risk of customer price spikes due to volatility in cost or supply of any single fuel source."

The economic advantage to Progress Energy is apparent, but in an unusual display of hegemony, North Carolina regulators have disarmed all the explosives in the usual regulatory minefield encountered when permitting a new gas plant. The North Carolina General Assembly recently approved legislation to fast-track a fuel or technology replacement project as Progress Energy has proposed. Senate Bill 1004 established a streamlined certificate process (45 days versus the standard six months or more) to enable Progress Energy to shut down the coal units and replace them with natural gas – fueled technology. The shorter certification period was needed to enable the company to replace the coal-fired plants by 2013, when the stricter statewide emission targets come into effect.

Expect additional state legislatures to quickly open an express lane for permitting gas-fired combined-cycle plants that replace older, less-efficient ones. Utilities will respond to this economic carrot much faster than to a swing of the regulatory stick.

The second emerging fuel-switching trend is retooling a coal plant to burn other fuels in order to help meet state renewable portfolio standards and to avoid costly emissions equipment retrofits.

The most interesting project in this genre of plant makeovers is FirstEnergy Corp.’s plan, announced in April, to repower two units at its R.E. Burger coal-fired power plant to burn biomass. Those two coal-fired units, totaling 312 MW, would become the largest biomass power plants in the U.S.

Burger Units 4 and 5 were targeted by the Environmental Protection Agency for alleged violations of the Clean Air Act’s New Source Review provisions. A consent decree signed in 2005 settled those charges but gave FirstEnergy until midnight March 31 to decide whether to shut down the units or agree to retrofit with expensive air emission control equipment estimated to cost $330 million. Instead, the utility decided to invest $200 million to convert the two units to burn biomass. The fuel switch also furthers FirstEnergy progress toward meeting Ohio’s standard that requires utilities to obtain 25% of their power from renewable resources — at least half of which must be generated within Ohio.

According to First Energy, the two Burger units will use wood wastes and other biomass to fuel the facility. FirstEnergy’s goal, however, is to operate the plant as a "closed loop" or carbon-neutral biomass plant, which means it will use fuel derived from trees grown to serve as feedstock for the biomass plant. The energy crop trees would act as a carbon sink, storing carbon in the trees’ tissues and roots. When harvested and burned, the stored carbon would be released, but the net carbon footprint would be zero. Fast-growing, bioengineered cottonwood trees and grasses grown in Ohio will be harvested and pressed into cubes before delivery to the plant. The plant will then pulverize and blow the biomass fuel into the boiler in much the same way as coal plants burn pulverized coal.

A number of other utilities have announced similar plans to retrofit fossil-fueled plants to burn biomass fuels. Over the past three years, Southern Co., Northeast Utilities, Dynegy, Xcel Energy, and DTE Energy have either converted plants or are in the process of doing so.

The Bottom Line: What You See Is What You Get

Where does all that leave generating markets in 2010? Looking not very different than they did in 2009, with the exception that natural gas has jumped onto the fuel stage in a big way. Coal perks along, with new plants under construction and some likely to come online. New nukes are ephemeral. Renewables can nicely fill generating niches but won’t dent the big generating market. They will make money but won’t change the U.S. generating mix.

Only gas looks likes a game-changer, given the emphasis on drilling in shale in the U.S. and elsewhere. The new exploration and production technologies and new gas reserves in shale probably won’t make a big impact in 2010, given lead times. They might in 2011. If they do, gas could alter the way the world looks at energy and electric generation. Stay on board for what could be a wild ride.

—Kennedy Maize is a contributing editor and Dr. Robert Peltier, PE is editor-in-chief of POWER.

Editor’s note: Professor Terry Engelder’s name was misspelled in the print version and an earlier web version of this story but has been corrected.