Further good news for electric utility fuel buyers comes along with low prices for coal and natural gas. Developments in the uranium market are likely to mean stable and low prices for nuclear fuel for several years. Prices for uranium oxide (U3O8) and for separative work units (SWUs) have been falling gently for some time, according to industry price indices, and new supplies of uranium and enriched fuel are likely to flow from U.S. producers in the future, providing further insulation to price increases.

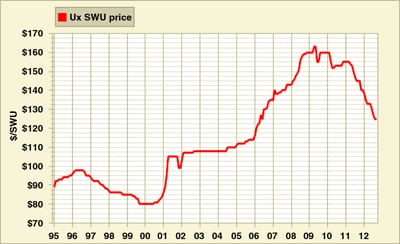

Stability appears to be the key word for uranium markets, a change from boom-and-bust conditions that often peristed in the past. In March 2011—just before the Fukushima disaster in Japan—U3O8 prices tracked by the consultancy UxC were at about $68 per pound. Since then, given a slowdown in the prospects for new nuclear projects and the removal of almost Japan’s entire fleet at least temporarily from the market, prices have fallen to about $52/pound, and have been holding at that level for about the last six months. In the past two years, SWU prices have slumped from over $160/SWU to under $135.

Investment analyst Tony Daltorio, writing in the market-tracking website Seeking Alpha, commented, “The uranium industry is also holding up better than would be expected by a casual observer. When the Fukushima disaster struck…the price of uranium was hovering near the $70 per pound level. Since then prices have fallen, but not off a cliff.”

Spot market activity has been slow. At the end of May, Trade Tech, a uranium and nuclear fuel analysis and consulting firm, reported, “Uranium spot market activity continues to languish with only four transactions reported over the course of this week. Buyers and sellers represented a broad cross-section of the market and included utilities, producers, traders, and financial entities. Buyers have expressed little interest in immediate spot delivery. Instead, the majority of active buyers are seeking material for delivery later in 2012, early in 2013, or beyond. Given the lack of spot market interest on the part of buyers, the primary focus of sellers continues to be on mid- and long-term sales opportunities and those tenders that remain outstanding. Prices in recently concluded transactions were clustered at, or near, today’s Weekly U3O8 Spot Price Indicator, and in spite of the lack of buying interest sellers are not aggressively pursuing sales opportunities.”

The current becalmed market is a clear contrast from what analysts were predicting just five years ago. In 2007, market mavens at MIT warned that a “lack of fuel may limit U.S. nuclear power expansion.” Researcher Thomas Neff issued a hand-wringing assessment of future supply of nuclear fuel: “Just as large numbers of new reactors are being planned, we are only starting to emerge from 20 years underinvestment in the product capacity for nuclear fuel to operate them. There has been a nuclear industry myopia; they didn’t take a long-term view.” At the time, uranium prices had risen from a dismal $10/pound to $85.

In retrospect, Neff’s vision was blurry. The nuclear renaissance that was behind his prognostication was a mirage; as it drew closer, it fizzled. The economy of the developed world slumped dramatically in 2008, taking electricity demand growth down with it and leaving only Asia as a potential growth market. Then Fukushima at least partly pulled the nuclear rug out from under Asian markets. Japan’s nuclear fleet slowed, stalled, and completely stopped. China, long the biggest bull in the Asian market, went into a year-long post-Fukushima building slump, and forecasts that India would be a booming nuclear market proved unfounded. Most recently, both China and India have gone into economic slumps of their own, suggesting that nuclear plant orders will slow even further, keeping downward pressure on fuel prices.

By last year, the fear in nuclear fuel markets was that Japan’s nuclear operators would dump their now-excess fuel into the secondary market, causing a price collapse. That would reprise the 1980s and 1990s when the U.S. nuclear pipeline turned into a mere trickle and utilities unloaded fuel bought under long-term contracts on spot markets. Writing in April, analyst Daltorio said, “Fears persist that Tokyo Electric Power will sell off of their inventory of uranium, the equivalent of a large new uranium mine entering the market.” So far, that has not happened.

Market prices are the result of the tug-of-war between supply and demand. In the case of uranium, demand has not materialized to the extent many observers expected a few years ago. In addition, there appear to be few limits to supply as long as prices hold around current levels. According to many analyses, a price of $50 per pound for U3O8, while well below levels of a few years ago, is still sufficient to provide mining and processing companies with healthy profits. Daltorio cited the case of Uranium Energy Corp., with 24 U.S. uranium mines, mostly in Texas. He said the company produces U3O8 “at an average cash cost of $16 per pound. It then turns around and sells the uranium at an average over the past year of $52 per pound. A profitable operation to say the least.”

There are also no signs that uranium is close to becoming a depleted resource, even in the U.S., where uranium mining has been occurring on a large scale since the 1940s. One of the largest uranium deposits in the world, today completely unexploited, sits in the middle of the Mid-Atlantic region in the state of Virginia. The Coles Hill uranium deposit in Pittsylvania County represents about 119 million pounds, according Virginia Uranium, the firm that owns the mineral rights and wants to mine it. That makes it the world’s seventh largest known deposit and the largest in the U.S. It was unknown 30 years ago. The Virginia General Assembly is considering lifting a uranium-mining ban to permit the company to start operations.

In addition to plentiful raw material, there is also no shortage of uranium enrichment capacity in the world to turn the U3O8 into fuel. A UcX analysis in May 2011 projected worldwide enrichment capacity in 2020 at about 85 million SWU (compared to about 30 million SWU today) and 2020 demand at about 70 million SWU, suggesting that enrichment prices will remain soft.

—Kennedy Maize is MANAGING POWER’s executive editor.