According to the report by the international accounting and consulting firm PwC, 68% of those surveyed in 71 companies in 42 countries say they are making “major or very major investments in upgrades and replacement generation” by 2030. But 78% report that the long-running economic downturn has hurt their ability to raise investment capital. “Overall,” says the report, more than twice as many survey participants say obtaining finance for generation and transmission is tough compared to those who are finding it relatively easy.”

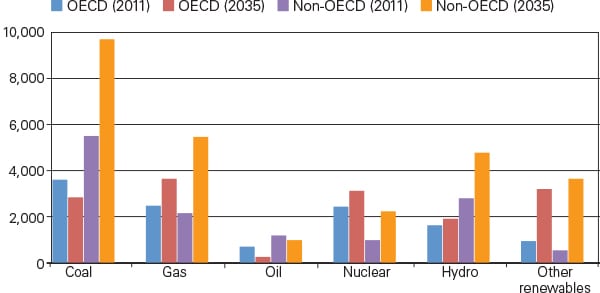

PwC’s report—The Shape of Power to Come—estimates that worldwide energy demand will rise from 17,200 terawatt hours (TWh) in 2009 to over 31,700 TWh in 2035. Natural gas will be the leader of the pack in supplying new demand, although, says PwC, gas “will not be a game changer.” New gas generation will come on at double the rate of new coal or nuclear electric capacity, according to the report. The gas share of the fuel mix will rise from 29% today to 33% in 2030.

According to the PwC analysis, power companies expect to see their fuel mix change from 66% fossil/34% non-fossil (nuclear and renewables) today to 57% fossil/43% non-fossil in 2030. Most of the non-fossil growth will come from non-hydro renewables, while nuclear will grow only enough to keep pace with demand increases. Despite the overall shift toward technologies that don’t generate carbon dioxide, the new generation mix, says PwC, “falls well short of what is needed by 2030 to limit global warming to an average of 2 degrees C.”

Will carbon capture and sequestration (CCS) be an atmospheric savior? So far, the technology has gotten off to a slow start, despite government attempts, particularly in the U.S. and the U.K., to jump-start it. Those companies that PwC survey remain somewhat bullish about capturing carbon dioxide and storing it. Survey respondents said they “expect over a third (35%) of their coal-fired generation and around a fifth (21%) of gas-fired generation to be equipped with CCS by 2030.”

High cost continues to be the barrier to greater market penetration by renewables, according to 75% of those surveyed. “Two thirds (66%) highlight the unwillingness of consumers to pay, and 62% stress the cost and difficulty of grid connections.”

Firms in Europe and North America, says PwC, “are now more concerned about the risk of blackouts than those in developing markets. In Europe and North America close to half (46%) predict an increased risk of blackouts until 2030, while in developing markets where cuts are currently more commonplace, 53% expect them to reduce.”

Smart grid technologies, seen by many in the industry as an important way to improve the efficiency of the electric system and empower customers, are having trouble getting traction, says PwC. The report notes, “Views on smart grids and metering highlight the gap to be bridged between domestic consumers and the industry. This is particularly notable in North America and Europe, where 80% and 74% respondents respectively are worried about customer engagement being an obstacle to realizing the full potential of these technologies.”

Looking at smart grid technologies, Steven Jennings, who leads PwC’s power program in the U.K., said, “Smart grids and smart metering are high on the list of investment priorities and yet a mix of customer apathy and concerns about data usage are already seen as constraints which could limit the potential for these new technologies. It will come down to building trust and transparency with customers to encourage and incentivize behavior change.”

What message is the industry sending to governments in the PwC report? The report says the policy message “is a clear one….” Three issues are policy priorities, according to the survey:

-

A regulatory environment that encourages network investment” (highlight by 80%)

-

Removal of strategic infrastructure bottlenecks (76%)

-

Increased interconnection between different electricity systems (76%)

Manfred Wiegand, PwC’s global power and utilities leader, said that industry and government face a need to find “the balance between affordability, security and sustainability. The outcome for key issues such as climate change and energy availability remains on top of the agenda. Investment has become more difficult and a majority report concerns about a shortage of capital for infrastructure projects. Reduced demand during the economic downturn has brought some breathing space in the race to meet global warming and power the infrastructure challenges. But our survey highlights a considerable degree of concern that outcomes may not be good by 2030 if investment availability and policy issues are not resolved.”

—Kennedy Maize is MANAGING POWER’s executive editor