The U.S. Energy Information Administration (EIA) earlier this year reported that the power sector was poised to add 11.2 GW of new natural gas–fired capacity in 2017. If that forecast proves accurate, it will be the largest addition in any year since 2005. What’s more, the EIA said another 25.4 GW of gas-fired capacity would be added in 2018. The combined additions would increase gas-fired capacity by 8% from the 2016 year-end total.

It’s no secret that natural gas has been gaining market share for some time. In April 2015, gas-fired generation exceeded coal power generation in the U.S. for the first time ever in a calendar month. Since then, gas has beaten coal 18 out of the 24 months for which reports are available. Gas has provided about 33.1% of the total power generated in the U.S. compared to coal’s 31.1% during the two-year period.

Market Drives Gas Generation Increases

Expanded natural gas production from shale formations is one of the main reasons that gas-fired generation has developed a competitive advantage. As more gas has been produced, gas prices have decreased and remained low in recent years. It’s also generally recognized that less manpower is required to operate a gas-fired facility compared to a coal power plant. Fuel and labor costs are often the two largest expenses a power plant has. Cheap fuel and less labor means cheaper power.

Gas-fired power plants have other cost advantages too, especially in the age of strict environmental regulations. Most coal-fired stations have had to retrofit units with expensive air quality control systems, increasing capital and operating costs.

Many of the gas power plants currently under construction are located in Mid-Atlantic states and Texas. That’s not surprising because two of the nation’s major shale plays are located in those areas, but pipeline networks are also being expanded to accommodate growth elsewhere.

Gas Price Volatility Remains

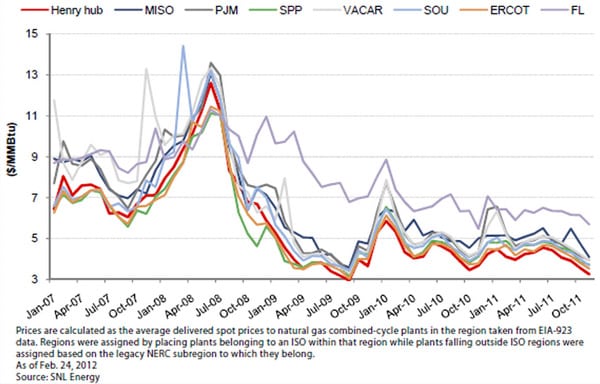

In its January 2017 Short-Term Energy Outlook, the EIA projected that natural gas prices would increase this year and next. The Henry Hub natural gas spot price (the Henry Hub is a distribution hub located in Erath, La., that interconnects with nine interstate and four intrastate pipelines, making it an important pricing point for futures contracts traded on the New York Mercantile Exchange) averaged $2.51/MMBtu in 2016. The EIA in January expected prices to increase to an average of $3.55/MMBtu in 2017 and $3.73/MMBtu in 2018.

The dollar-plus price increases haven’t materialized so far this year. The average Henry Hub spot price through mid-June was about $3.06/MMBtu. That’s a 22% price increase compared to last year, but it’s still less than in 2014, when the Henry Hub average was $4.39/MMBtu, and it’s far below the $8.89/MMBtu gas averaged in 2008.

|

However, power plants don’t typically procure gas for the price quoted at the Henry Hub or any other wholesale hub for that matter. The price actually paid by a plant includes what is called a basis differential. The basis differential factors in such things as supply and demand dynamics specific to a given location, pipeline delivery costs, possible short- and long-term constraints, and other influences. Basis from any wholesale hub can be positive or negative depending on the situation.

“Probably the bigger issue for generators, in my mind, is the changing basis differentials and the potential for increased volatility in those basis differentials,” Charlie Palmer, managing director at Opportune and head of its Power and Gas sector, told POWER during an exclusive interview. Opportune is an energy-only consulting firm.

Palmer believes there are four major drivers for changing basis differentials: changes in supply from shale gas development, the potential growth in liquefied natural gas shipments, planned Gulf Coast chemical plant investments, and swelling exports to Mexico. “Those potentially big swings in volumes can create significant volatility in the natural gas price basis differentials,” Palmer said.

Most generating companies have energy trading risk management systems and hedging tools, but that hasn’t prevented some pretty efficient combined cycle units from facing financial distress. In the end, owners must exercise caution when leveraging assets because low prices and low margins often make covering fixed expenses difficult.

“The risk of being in this business is probably going up, not going down,” Palmer said. ■

—Aaron Larson is POWER’s executive editor.