A recent Washington Post article attacks coal as a fuel with a dim future. The author points to the large number of plant retirements as evidence of its impending demise. Checking the actual data reveals a much different story.

The January 2 article, “Coal’s Burnout,” presents a view of the future of coal plants that is more wishful than factual. The article cites the number of coal plant retirements—“power generating companies… would retire 48 aging, inefficient [plants]”—and the Sierra Club trumpets those statistics as a sign that “coal is a fuel of the past.” Surprisingly, the number of plant retirements cited is much too low. Not surprisingly, those retirements will have no significant impact on the future of coal-fired generation in the U.S.

Predicting Plant Retirements

A number of recent studies have examined the magnitude and duration of coal-fired plant retirements. For example, The Brattle Group released a study, “Potential Coal Plant Retirements under Emerging Environmental Regulations,” in December last year. As part of that study, the consulting group developed a coal plant retirement screening model that considered economic and environmental drivers to various scenarios that predict when existing coal-fired plants will retire.

The Brattle analysis found that the rate of retirements accelerates by 2015 (when many new boiler and other environmental regulations are assumed to become effective). Bottom line: Brattle estimates that 50 GW to 65 GW (up to about 20% of today’s coal-fired generation) will retire or will be “at risk” by 2020, and gas-fired assets will be constructed to backfill reserve shortfalls. The two controlling assumptions in the analysis are the date when new environmental rules (maximum achievable control technology, cooling water, ash, and so on) become effective and the future price of natural gas.

|

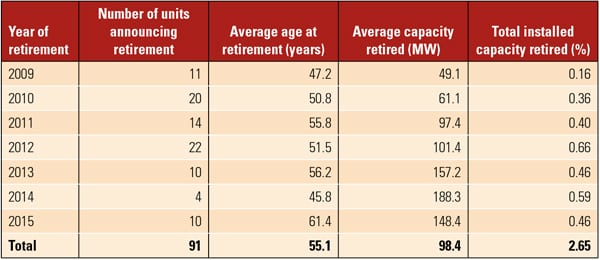

| Predicted coal-fired plant retirements through 2015. The total nameplate of retiring plants is just under 9 GW. The Total averages are calculated over seven years. Source: SourceWatch |

Little Loss in Generation

Let’s put these numbers into the proper perspective. The nameplate capacity of the existing coal-fired fleet (1,436 plants) is roughly 338.7 GW (about 30.1% of the nation’s entire installed power capacity) yet those plants produced more than 45% of the electricity consumed in the U.S. in 2010. The average capacity factor of coal plants in the U.S. was 65% in 2009 (the last year for which I could find data), illustrating that there are many coal plants that operate very few hours each year. It’s no secret that many of those assets are past their prime and are overdue for retirement.

Real and predicted plant retirement data through 2015 best tell the retirement story. SourceWatch, no fan of coal-fired plants, maintains a database of coal plants that have retired or will retire by 2015. I used its data to prepare the table. The nameplate capacity of plants on the retirement list totals just under 9 GW through 2015 (there are very few announced retirements post-2015). On the whole, the number of retirements through 2015 is quite modest and includes very old plants that are uneconomic to operate or upgrade. Also, given the very low capacity factors of these plants, the 2.65% loss of nameplate (MW) is, in my estimate, less than 1% of generation (MWh) spread over seven years.

Economics Rule

Power generators are in the business of providing low-cost, reliable electricity to their customers while (if it’s a public company) earning a reasonable rate of return for shareholders. The modest number of plant retirements is no surprise and certainly not an indicator that the industry is turning away from coal-fired generation. In fact, the last National Energy Technology Laboratory coal-fired plant database lists 17 GW of new coal plants either under construction, near construction, or permitted—much more than the 9 GW lost through retirement of the 91 plants listed by SourceWatch.

I expect industry average capacity factors will slowly increase over the next few years, and plant retirements will allow executives to focus limited capital on life-extension upgrades of the remaining plants. In the long term, trimming these underperforming assets is just good business.

— Dr. Robert Peltier, PE is POWER’s editor-in-chief.