In 2010, U.S. wind power development has slowed, coal-fired power development remained stalled, and the much-awaited renaissance of nuclear power took a few tentative steps forward. That left natural gas power development as the last man standing.

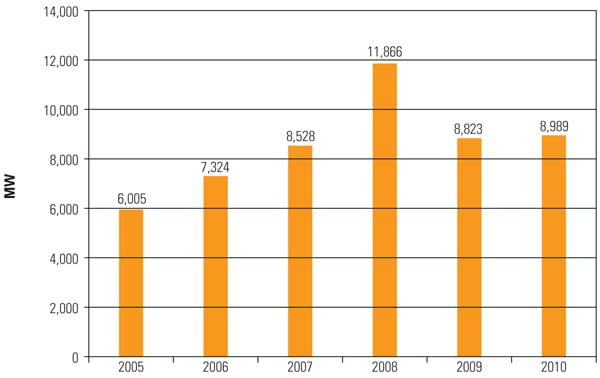

U.S. natural gas power development continued at a healthy pace during the first half of 2010: Industrial Info Resources was tracking a total of nearly 9,000 MW of new gas-fired generating capacity that had a scheduled 2010 kickoff date. That sum includes about 3,800 MW that was actually under construction as of July, another 2,700 MW that was in the engineering phase, and about 2,400 MW that was planned. In addition, 5,369 MW of new capacity became operational during the first seven months of 2010 (see figure).

|

| U.S. natural gas development by construction kickoff year. Nearly 9,000 MW of new gas-fired generation capacity is scheduled to begin construction in 2010. That’s about even with 2009 levels and less than 2008 but significantly ahead of 2005 and 2006 levels. Source: Industrial Info Resources |

Moreover, during 2010 construction continued on more than 13,000 MW of U.S. gas-fired generation that had broken ground during 2007–2009. We expect that construction will finish on several hundred megawatts of those projects during the second half of this year. By contrast, for all of 2009 dirt was turned on roughly 8,000 MW of gas-fired generation in the U.S., and another 8,480 MW became operational.

Although 2010 is not expected to be a banner year for the construction of gas-fired generating capacity in the U.S., this year does compare favorably with gas power construction starts in 2005, 2006, and 2007. And given the historic surge in gas-fired construction that took place at the start of this decade, the kick-off of nearly 9,000 MW of gas-fired generation projects should be regarded as a respectable year.

Why Gas Held Ground

Several factors drove this year’s continued dash to gas. Natural gas for electricity generation continues to be reasonably priced—in the $3 to $4 per million Btu price range for much of the past 12 months. Lower capital costs and faster construction times continued to work to the benefit of gas-fired power developers. Each installed kilowatt of gas-fired generating capacity costs about $750 to $1,000. Wind power, by contrast, costs about twice that, and coal is at least three times that. On average, siting and building a new combined-cycle gas generator takes 18 to 24 months; siting and constructing a new coal-fired generator, by contrast, takes a minimum of three to four years and requires an extremely high tolerance for the risks associated with pending environmental legislation.

Siting issues are another important reason behind this year’s continued gas buildout. Gas-fired generators could be easily sited on existing power plant footprints or located close to existing transmission lines, thus obviating the need to site and construct transmission lines to connect generators to the grid. Baseload coal generation or wind farms, by contrast, require large footprints and often require the construction of transmission lines to get power to the grid.

Development of gas-fired generation in the U.S. also benefited from increased regulatory and legislative efforts to limit emissions of carbon dioxide, mercury, and oxides of sulfur and nitrogen. Several energy and climate change bills were introduced in Congress this year. Although they took different approaches and included different timelines, none of the proposed bills was good news for the coal industry and developers of coal-fired power. In many cases, the only unresolved questions in these draft bills were: How many older, less-efficient, high-emitting coal-fired generators would have to be retired, and over what time frame, to meet increasingly stringent U.S. environmental standards?

The lower risk profile offered by gas-fired generation has been particularly important during 2010, because rate-based assets made a significant comeback. The majority of the capacity being built in 2010 is being developed by utilities or developers for the purpose of placing those assets in a utility’s ratebase so the utility can earn a guaranteed rate of return on the new assets. As rate-regulated assets, utilities had a strong incentive to choose generation options carrying the lowest risk profile. By contrast, in previous years, the majority of new capacity consisted of merchant power plants built so that their owners could sell the output at market prices.

Facing rising environmental risks and soft near-term demand growth for electricity, electric utilities increasingly pushed the button marked “natural gas,” which continued to increase gas’s share of the market.

The Future Favors Gas

Beyond 2010, there is a healthy book of gas-fired generation construction slated for kick-off over the next few years. Industrial Info is tracking 44,500 MW of U.S. gas-fired power plant construction scheduled to begin between 2011 and 2015. Not all of these projects will move forward, of course, but the sheer volume of planned power projects is another sign that gas-fired power development has a bright future.

In recent years a number of coal-burning utilities—including Progress Energy, Duke Energy, Exelon, and Portland General Electric—have announced that they will close more than 4,500 MW of operating coal-fired plants and replace at least some of the shuttered output with new gas-fired generation. Most, if not all, of their utility brethren are said to be running complex financial, operational, and environmental calculations to determine which of their coal plants will be closed and how that shuttered capacity will be replaced.

We see little on the horizon that would reduce the positive outlook for gas-fired generation compared to other fuels, for these reasons:

- If Congress fails to enact comprehensive energy and climate change legislation this year, the administrator of the U.S. Environmental Protection Agency (EPA) has vowed to enact limits on greenhouse gas emissions under the agency’s authority in the Clean Air Act.

- The EPA issued its proposed Clean Air Transport Rule in mid-July and is scheduled to release a draft Clean Air Mercury Rule in early 2011, both of which are expected to push up the price of electricity generated from coal due to the required installation of environmental retrofits. The Clean Air Transport Rule replaces the rejected Clean Air Interstate Rule.

- The aforementioned expected congressional and EPA actions likely will force the closure of dozens, if not hundreds, of older, less-efficient, and higher-emitting coal-fired power plants, located mainly in Midwestern states.

- The recent surge in construction of renewable generation such as wind and solar has led to a corresponding increase in the use of gas-fired power and, occasionally, the construction of new gas-fired capacity to back up these intermittent resources and provide grid stability.

- Carbon capture and sequestration projects continue to demonstrate that the technical ability to remove and store carbon dioxide from a coal-fired generator’s flue gas stream exists. But these processes are enormously expensive. In addition, the underground injection of carbon dioxide raises significant legal and policy issues.

- U.S. natural gas discoveries and reserves continue to grow, helping to limit price increases. Notably, large gas discoveries from unconventional sources, such as shales, continue to be brought online. Gas from the Barnett Shale, which lies under Dallas–Fort Worth and the surrounding area, provides nearly 10% of U.S. natural gas demand. Even larger shale formations, such as Haynesville and Marcellus, contribute to a positive resource outlook that keeps gas prices low.

- Opinion leaders and elected officials increasingly view natural gas as an environmentally preferred fuel—a bridge to a clean-energy future, in the words of a recent assessment of the future of natural gas from the Massachusetts Institute of Technology.

- Nuclear power remains a “bet the company” proposition, despite the availability of billions of dollars of federal construction loan guarantees.

As we write this in July, the U.S. economy appears to be slowly emerging from the recession that began in December 2007. It has been the longest economic downturn in 75 years, resulting in two years of reduced demand for electricity, which in turn has allowed utilities to defer the start of construction on new generation. We expect that the U.S. economy will continue to gain strength during the remainder of 2010 and into 2011, which will have a positive effect on power plant development for all fuels.

There is a tremendous amount of financial, intellectual, and operational capital sitting on the sidelines now, waiting for strategic changes in the industry to unfold. We expect the power industry to continue to be highly dynamic, particularly as the 2010 mid-term election cycle heats up. Although the BP oil spill in the Gulf of Mexico has nothing to do with electric power generation, more than a few analysts believe that the BP spill will eventually seep into—and possibly foul—the nation’s electoral and regulatory treatment of the power industry.

— Britt Burt (bburt@industrialinfo.com) is vice president of research and Shane Mullins (smullins@industrialinfo.com) is vice president of product development for the power industry at Industrial Info Resources (http://www.industrialinfo.com) in Sugar Land, Texas.