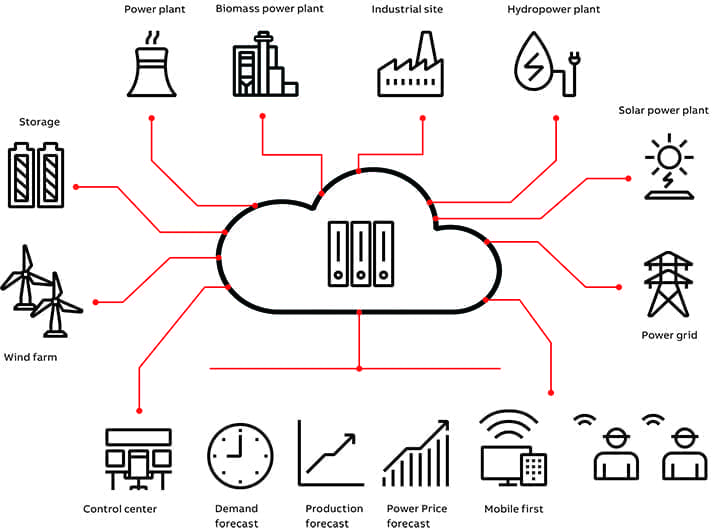

Blockchain—a distributed database technology that allows a network of parties to securely transact with each other—has been hailed as a game-changing innovation in the power sector for its potential to host transactive energy markets and boost decentralization (Figure 1). In one much-touted application, for example, residential and commercial actors could use blockchain to bypass existing electricity markets and electric utilities, and directly buy and sell energy with each other and other entities via a digital platform. And, as IBM experts noted in October, the technology may offer intelligence, transparency, and automation to existing systems—attributes they noted could help “mitigate the massive capital investments that would be required to re-architect the physical grid.”

|

|

1. Some experts believe blockchain promises great things for power and utility companies, but a report titled “Assessing Blockchain’s Future in Transactive Energy” suggests it may not be the panacea for all energy challenges. Source: Shutterstock |

But according to a September 2019 report from American think-tank Atlantic Council, blockchain isn’t currently well-suited to host any of the primary functions of a real-time transactive energy market, including for energy data transmission, financial bids, trades, settlement, price formation, and grid service provision to the utility. “While blockchain has many other potential energy-relevant applications for which it may be a far more logical and valuable tool, this does not currently extend to serving as the key platform for transactive energy markets,” concludes the report, “Assessing Blockchain’s Future in Transactive Energy.”

The report stems from a scrutiny of the technology’s costs and benefits against specific power sector needs in a real-time transactive energy market. “Rather than paint a straw man perspective of first-iteration blockchain systems that would inevitably be easy to critique, the analysis takes account of advances in blockchain consensus, on- and off-chain scaling, governance models, privacy enhancements, and other extant and prospective innovations,” said its authors, Ben Hertz-Shargel, an executive at EnergyHub, a distributed energy resource (DER) management platform for utilities, and David Livingston, deputy director for climate and advanced energy at the Atlantic Council’s Global Energy Center.

The concept is alluring for the power sector, which like so many other industries—from media, disease control, and fishing—has sought to leverage its “energy eBay” potential to reimagine and transform the way traditional business is done. Today, several utilities and energy firms, as well as startups are exploring blockchain ventures with applications that range from green attribute certificate tracking to financial settlement for grid services.

However, efforts are still in the nascent stages. As a July 2019-published survey conducted by the Electric Power Research Institute suggests, most utilities in the U.S. are in the early pilot stages or in the research phase, while European utilities are a year or so ahead. Meanwhile, policymakers, and federal entities are also taking notice. Public utility commissions in Arizona and Nevada, for example, have opened dockets to explore blockchain-related issues, and the Department of Energy’s November 2019-issued grid modernization blueprint prioritizes development of cross-sector guidance and standards for novel blockchain-based concepts.

But criticism has also accompanied industry’s “breathless proclamations” about blockchain, the report notes. Among prominent concerns are that blockchain demands vast amounts of computation—and therefore energy use—“to guard against malfeasance in the network,” as well as over the instability of cryptocurrencies. “As second-generation blockchains have begun to move away from proof of work, more nuanced criticism has taken aim at blockchain’s suitability for broader applications, questioning its scalability, cost-effectiveness, potential lack of data privacy, and cybersecurity,” the report notes.

Compounding the issue is that industry lacks a technical understanding of blockchain’s limitations. “Common examples are claims that, as a distributed ledger technology, blockchain makes it faster or easier for distributed resources to submit transactions to the network than traditional centralized platforms, or that blockchain relates to the distributed control often proposed for smart grids,” it says. “In fact, blockchains today can support an order of magnitude fewer transactions than other modern platforms, and their distributed ledger control has little relation or contribution to the kind of intelligent grid and energy market management required for transactive energy. Blockchain, though offering a number of significant benefits, is not a panacea.”

The report’s conclusions result from what the authors call a “fundamental tradeoff,” which is essentially an evaluation of how well blockchain’s disintermediation of a central authority can be achieved in the context of six “costs”: efficiency, scalability, certainty, reversibility, privacy, and governance.

When considered as a transactive energy tool, the costs of blockchain are “steep,” it says. One reason is, “The duplication of data hosting and processing across every node in the blockchain network dramatically limits both capital efficiency and scalability to real-world data and transaction volumes.” To agree upon the shared transaction ledger, participants must rely upon economic incentives, but that poses risks to settlement finality as well as security of the network. “Perhaps most problematic, blockchain faces the opposing obligations of keeping mission-critical electrical and financial data confidential, while making it visible to its fleet of validator servers, which operate outside of a corporate firewall. Moving this confidential data off-chain would eliminate the issue, but significantly reduce blockchain’s role in primary transactive market functions.” And so far, cryptographic techniques that could address these core issues—such as zero-knowledge proofs, multi-party computation, and secure hardware enclaves—“are in an early stage of research and development” and they present limitations, including that they have not been yet attempted in energy-related applications.

However, the report offers several policy recommendations that could encourage and focus the development of transactive energy platforms—blockchain-based or not—and help invert the six “costs.” These include direct financial incentives, such as agency funding and prize-based awards, as well as indirect incentives that clarify the regulatory and commercial landscape for these platforms. Also recommended is the formation of working groups and regulatory proceedings to study the value of transactive energy in light of state-specific policy objectives, such as distribution infrastructure deferral, grid resilience, renewable portfolio standards, and retail market animation.

“In sum, this report finds that blockchain should neither be dismissed outright, nor be viewed as a comprehensively disruptive technology or panacea for all energy challenges,” the authors wrote. Even if it isn’t well-suited for real-time transactive energy market applications, it shows better viability for applications that require less frequent transactions and non-confidential data, such as renewable energy credit tracking and energy asset onboarding. Which means that for now, blockchain will “likely continue to evolve as an increasingly useful tool for specific applications, building upon (rather than replacing) legacy systems to bring improvements to the function of energy markets as they become increasingly distributed and transactive in the years to come,” the authors predicted.

—Sonal Patel is a POWER senior associate editor.