ELECTRIC POWER 2010

At the opening ELECTRIC POWER 2010 plenary session, both the keynote speaker’s address and discussion among the Power Industry Executive Roundtable participants pointed to the renewed appeal of natural gas and proposed cap-and-trade legislation as being potential game-changers for the U.S. power industry.

The keynote address at May’s ELECTRIC POWER 2010 in Baltimore, and comments by the panel of industry executives at this session, revealed the key but subtle role that natural gas will play in the coming years. Meanwhile, everyone loves cap and trade as it now stands before Congress, even if it’s because something is better than nothing, or because it beats the regulatory drum being pounded at the Environmental Protection Agency (EPA). The appeal of “unfettered” electricity markets continues to recede, while coal, in the figurative sense, is staring at the chassis of the bus.

When I was part of a public equities investment fund focused on the electricity production and delivery value chain, I developed a “dashboard” that would reflect the state of the industry. In the center, the speedometer, if you will, was the forward price of natural gas. Everything on the supply side of the business pivots around it, I coached my colleagues.

Industry Revelations

You didn’t hear that directly, if you were among the approximately one thousand industry professionals who gathered for the keynote session. But that’s what the underlying message was. Sure, there was handicapping of the American Power Act (APA), recently reported out of committee in the Congress; nods to the smart grid; nearly unanimous agreement that cap and trade as currently stipulated in the APA is a good thing; tips of the hat to more renewable energy; recognition that real electricity rates will keep escalating, despite the recessionary blow to demand; and polite discussion about the rock and hard place between which the coal industry finds itself today. But so many of these discussion threads, implicitly or explicitly, seemed to weave together and lead back to gas.

Before we get to all that, let me share with you some true revelations made by the keynote speaker, Richard F. McMahon, executive director of the Edison Electric Institute (EEI) (Figure 1), and the Power Industry Executive Roundtable panelists (Figure 2) during the session:

|

| 1. Keynote speaker Richard McMahon. McMahon is the executive director of Energy Supply and Finance for the Edison Electric Institute. Source: POWER |

|

| 2. The 2010 Power Industry Executive Roundtable panelists. From left to right: PJM Interconnection Senior Vice President Operations Mike Kormos; Calpine Corp. Senior Vice President Power Operations John Adams; Duke Energy Group Executive and President Commercial Businesses Keith Trent; NRG Energy President Northeast Region Drew Murphy; Constellation Energy Group Executive Vice President, Corporate Affairs, Public and Environment James Connaughton; and Moderator Dr. Robert Peltier, PE, editor-in-chief of POWER. Source: POWER

|

- If the derivatives regulation piece of the financial overhaul bill passes Congress, the typical investor-owned utility would need to tie up from $250 million to $400 million in cash for margin calls. –McMahon

- The world spends $8 billion on climate science a year. –James Connaughton, executive VP, Corporate Affairs, Constellation Energy

- Sixty million U.S. electricity consumers are expected to have smart meters by 2019. –McMahon

- Only 6% of ratepayers have smart meters today. Some electricity bills are going up because these meters are much more accurate, making consumer acceptance a challenge. –McMahon

- Power prices at PJM International LLC (PJM), a regional transmission organization (RTO), were down to $27 per MWh on peak on May 17, a day before the session. –Andrew Murphy, regional VP, NRG Energy

- Wind energy can afford to stay on PJM’s system until prices go below –$30 per MWh in the market because of the production tax credit. –Michael Kormos, senior VP, Services, PJM

- If the EPA regulates carbon, we will get one-fourth of the benefits for four times the cost, compared to cap and trade. –Connaughton

- We can replace 43% of the cars in this country without building a new power plant, simply by exploiting the disparity between peak and off-peak economics. –John Adams, senior VP of operations, Calpine Corp.

- Most utilities barely have an investment grade rating on which to finance their capital expenditures (capex). –McMahon

Gas Is King

The first tip-off regarding gas came in McMahon’s opening address. Of the six “game-changers” he presented, the first was an explanation of the industry’s capex hurdles. The second was the role of unconventional natural gas, which McMahon labeled a “huge game-changer,” noting that it “overtakes LNG” [liquefied natural gas] as a new source of this premium fuel.

Electricity is the key driver for unconventional gas, he continued. Unconventional gas sources (a designation that implies this natural gas is more difficult to extract) represented 1% of the market in year 2000, represents 20% today, and McMahon thinks it could be 50% by 2035, as long as potential environmental issues are worked out. The ecological disaster unfolding in the Gulf of Mexico as I write probably makes this point loom larger than usual. The fact that unconventional gas reserves are a domestic resource and are so vast, however, could keep a lid on price volatility as well.

The upshot of these remarks, along with much other evidence in the industry, is that we may be in for another “gas bubble” not unlike the one that affected the industry from 1986 through the late 1990s.

The second indication was when Adams observed that Calpine (which has almost exclusively gas-fired power assets plus a few geothermal units) “sold more power in 2009” than in 2008, as well as in the first quarter of 2010, an unusual claim from the depths of the economic recession. This was in response to a question about the impact of declining electricity sales posed by Dr. Robert Peltier, POWER’ s editor-in-chief, who presided over the panel. Adams credited low heat rates and low natural gas prices, which combined to push many of his plants first in the dispatch queue. Kormos noted that “older coal plants operated at a loss” and that load declines make PJM nervous.

In a historical context, this is an interesting comment by Adams. More than 10 years ago, during the heyday of merchant generation and competition, Calpine’s executives predicted that their plants would knock inefficient, dirty fossil capacity out of the market even for baseload service. It may have taken a decade, but that prediction is now apparently coming true, probably for vastly different reasons. It’s like I tell my kids: Wait long enough and any prediction will come true. Indeed, Keith Trent, executive VP, Commercial Business, Duke Energy, said that his company will likely retire more older coal plants to avoid running the “environmental gauntlet.”

Later, Adams made the gut-check observation that you can build 10 gas-fired plants for the price of one nuclear plant. Trent told the audience to consider gas and wind as an integrated unit.

Finally, when Peltier asked what resources were coming online, four out of the five executives mentioned gas-fired assets.

Coal under the Bus

The forces arrayed against coal right now are like an armada at the coast line. That’s alarming, given that coal is, on balance, our least expensive source of baseload electricity. Climate change is only part of the story; the rest of it pertains to new regulations focused on coal combustion by-products and reuse, particulate matter 2.5, mercury and the other hazardous air pollutants, ozone, water use and the Clean Water Act, the Clean Air Interstate Rule, and additional regulations around SO2 and NOx. All of these rules are likely to force existing coal plants off the grid and prevent new ones from being installed.

The way in which the panel addressed a question from the audience related to carbon capture and sequestration (CCS)—coal’s technological knight in shining armor—didn’t seem to make the bus chassis look any farther away. Trent noted that commercializing CCS would probably happen first in China. (See the section on CCS in China in this issue’s special report.) He also stated that coal looks “really difficult without CCS,” silently posing the question, “What happens if CCS fails or doesn’t prove to be economic?” Connaughton, who was previously chairman of President George W. Bush’s Council on Environmental Quality, said that “we can get to the policy goals [of climate change] without CCS” by installing twice as much nuclear and gas as we have today. Later, he asked, “How much coal can we really use in the future?”

Ten years ago, my last editorial for POWER magazine when I was its editor-in-chief, which was for the first issue of the new millennium, was entitled “Bet on Nuclear for the Next Century.” As with the Calpine executive, my prediction might be right 20 years from now. Brighter prospects for nuclear, the other baseload option, dampen long-term prospects for coal.

Responding to a question from the audience, McMahon said that the “outlook for nuclear was extremely positive,” but he acknowledged that it is the most capital-intensive option. Peltier noted that such projects represent a “bet the farm” strategy, but Trent countered that the risk can be mitigated through regional partnerships. Murphy’s firm, NRG, is building two new units at the South Texas Project nuclear plant. Constellation is also exploring the nuke option and, according to Connaughton, is “hoping to be next on the loan guarantees.”

The one positive note on coal came when Trent reported that Duke Energy’s integrated gasification combined-cycle (IGCC) plant in Indiana at its Edwardsport power station was under construction, although he acknowledged that it was supported as much by policy as economics. “Coal is important to Indiana,” he said, and “rates go up significantly because of the IGCC.”

Renewables Dominate Today

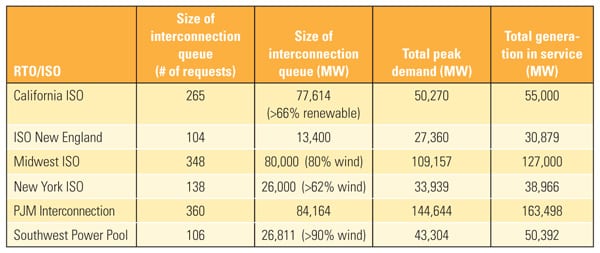

Although wind energy faces its own challenges, including the collapse of tax-benefit financing by Wall Street firms and the general effects of the recession, it remains the darling of the political class and, as a result, appears to be the one option that can run the gauntlet. The electricity industry—as it has done several times in recent history with supercritical coal, nuclear, and gas-fired combined cycles—has converged on this option to expand capacity. Want evidence? Just consider an eye-popping slide McMahon put up (see table), which showed that wind (or renewable energy) represents from 60% to 90% of the interconnection queue in three independent system operators (ISOs) (CAISO, MISO, and NY-ISO) and one RTO (Southwest Power Pool).

|

| The new reign of renewables. Currently, wind, solar, and other renewable resources dominate the interconnection queues, particularly in the Midwestern and Western regions and New York. Source: Edison Electric Institute |

Consider now that Kormos, in responding to a question regarding wind energy and grid stability, said that the 3,000 MW of wind on PJM’s 140,000+ MW system gets credit for only 13% of its capacity value during peak periods. Given that figure, and the fact that wind farms typically achieve an overall annual capacity factor of 30%, guess which type of plant is going to fill in over the long term to match the daily, weekly, and seasonal load demand curves with supply? Not nuclear units, because they aren’t allowed to cycle. Not coal, because running the environmental gauntlet is probably going to force more and more of those plants off the grid. That leaves gas, especially under the new forward price and supply regime implied by the growing unconventional reserves.

One option that could compete with gas-fired assets for this duty, however, is energy storage. McMahon called storage a “step factor” that “enables” more and more renewable energy. Kormos called storage a “big innovative thing that is coming.” He added that compressed air energy storage is being considered along with new pumped hydroelectric storage, and battery facilities that are under test in PJM’s system.

All Hail Cap and Trade

Rarely does unanimity strike a power industry panel, but the APA and its “conservative” cap and trade provisions, according to Connaughton, received a resounding vote of approval from the panel. Connaughton called it a major step forward and said that it “adds creative thinking from the power sector.” Murphy said his firm was pushing for cap and trade and that it has to happen sooner rather than later. Trent supported the legislation and noted that the EPA will regulate carbon without it. Adams was favorable toward the bill because it nicely positions efficient gas-fired capacity. The slightest waver came from Kormos, who said he was supportive of any legislation at this point just for the certainty of it.

The conclusion, perhaps, is not so much support for cap and trade but that anything is better than the EPA regulating carbon.

—Jason Makansi (jmakansi@ pearlstreetinc.com) is president, Pearl Street Inc.; principal of Pearl Street Liquidity Advisors LLC; and executive director of the Coalition to Advance Renewable Energy through Bulk Storage (CAREBS).