As the oldest renewable energy resource, hydropower is well-established as a reliable source of dispatchable energy. Yet, it is often overlooked and taken for granted. It’s commonly believed that hydro’s potential is tapped out in the U.S., but many opportunities exist to add capacity at non-powered dams and on repowering projects.

Hydropower installations worldwide have been increasingly impacted by drought conditions. The World Economic Forum in a recent report noted that while hydro for many years has provided most of the globe’s renewable energy, its output has slowed due to the effects of climate change, including what the International Energy Agency (IEA) calls “erratic” rainfall. The IEA has said global investment in hydropower generation capacity has fallen in the past few years, and the group expects that trend will continue.

|

|

1. Chinese officials said the Baihetan Hydropower Station, the world’s second-largest hydro dam with 16 GW of generation capacity, represents an investment of about $34 billion. Courtesy: China Three Gorges Corp. |

Despite that, new projects—including large installations—are being built. China and the U.S. in recent years have experienced drops in the percentage of hydro as part of those countries’ generation mix, but China for its part continues to invest in hydroelectricity as part of that country’s strategy to increase all forms of power generation. China is home to most of the largest hydropower dams in the world, led by Three Gorges Dam, a 22.5-GW behemoth that has produced power since 2003. Next is the Baihetan hydropower station (Figure 1), a 16-GW facility that became fully operational in 2021.

Climate Change Impacts Hydro

Chinese officials, though, earlier this year said the country’s hydro generation has been essentially flat for the past three years despite several new large power stations coming online, including the Lijiaxia Hydropower Station No. 5, one of the world’s biggest hydropower plants in a dual-row turbine layout. That facility entered operation in October of last year. Officials in China have acknowledged the need to continue to support hydropower, even as prolonged drought has markedly reduced river flows in the southwestern part of the country.

This article is included in “Coming Together for Clean Energy,” POWER’s publication that is aligned with RE+, the largest renewable energy trade show in North America. RE+ is happening Sept. 9-12, 2024, in Anaheim, California. To continue the conversation around clean energy, plan to attend POWER’s EP Week event in Orlando, Florida, Oct. 9-11, 2024.

In This Issue

Full issue“Hydropower generation critically depends on how much water runs in rivers and hence hydro climatological conditions. In the decades to come, there are likely more frequent and severe droughts globally, threatening sustainable hydropower operations and installations,” said Dr. Hong-Yi Li, associate professor of civil and environmental engineering at the University of Houston. Li told POWER, “To tackle this challenge, other forms of renewable energy such as solar are worthy of more consideration than ever, particularly for those places that already often experience water shortages.” China has certainly recognized this; the country added 226 GW of new power extra generating capacity last year, with 129 GW from solar, 39 GW from thermal, 33 GW from wind, and 8 GW from hydro, according to the National Energy Administration.

Dimitrios Kalliontzis, assistant professor of civil and environmental engineering at the University of Houston, told POWER: “Hydropower accounts for more than 25% of the renewable electricity generation in the United States. The risk hydropower is facing underlines the need to rethink, adapt, and transform. While drought is a threat to hydropower facilities, climate change and the associated sea level rise may create opportunities to adapt existing technologies to the offshore marine environment, harvesting tidal streams, currents, or even waves. While offshore harvesting is still in the early stages, it can potentially compensate or exceed the current hydropower supply.”

Ember, an energy think-tank based in the UK, last year reported that global output of hydropower had a historic drop in the first half of 2023. The group said drought conditions led to an 8.5% decrease in global hydro output during that period; China accounted for about 75% of the worldwide decline. The IEA has said hydropower eventually will be overtaken by solar and wind energy output, though the agency doesn’t expect that to happen for at least another decade. The group said a slowing of the industry’s growth puts global net-zero targets in jeopardy. The International Renewable Energy Agency reported that hydropower generation capacity must double by 2050 for the world to remain on track to limit global warming to 1.5C by mid-century.

John Stranne, research associate, Nordic and Baltic Power Markets at Aurora Energy Research, told POWER: “Increased variation in weather due to climate change, with more frequent droughts and floods, will increase the level of uncertainties for hydropower operations. Mainly, the weekly, monthly, and seasonably valuation of water—which leads to tougher optimization and reduced system efficiency. Storage plants plan their behavior several months or even years in advance, estimating when they should contribute how much to the electricity market and at which hours of the day and periods of the year, where the system benefits the most. If weather patterns, and correspondingly hydro inflows, become harder to predict, it could lead to changed bidding behavior on the market, potentially increasing weekly spreads, or price volatility.”

Investments Flowing to Hydropower Projects

The U.S. Department of Energy (DOE) in a 2023 market report said that incentives authorized in the Bipartisan Infrastructure Law and the Inflation Reduction Act (IRA), including tax credits, “are expected to stimulate investment in upgrades to the existing [U.S.] fleet and construction of new hydropower and PSH [pumped storage hydro] projects in the coming years. However, they may have contributed to the decline in activity in 2021–2022 because of plant owners waiting for full guidance on the implementation of these incentives (e.g., which types of projects would qualify, details on wage, apprenticeship, and domestic content requirements) to make any new capital investment decisions.”

Don Erpenbeck, vice president and global sector leader of Hydropower & Dams at Stantec, an engineering services firm, told POWER: “The U.S. hydropower market continues to be very robust for engineering and for capital projects’ work. However, it is slightly different than people think it is… 90% of the capital spend in the U.S. is around hydropower refurbishment, dam refurbishment, and environmental projects that are the result of ongoing Federal Energy Regulatory Commission license compliance or other environmental improvements.”

Erpenbeck said Stantec is currently working on more than 20 GW of repowering in the U.S. alone. “That is mostly in the powerhouses and the powertrain equipment, but also includes the upgrades to dams, spillways, and other major civil infrastructure elements. It’s a large, multibillion-dollar construction market overall. The U.S. fleet, in general, is being modernized to increase their flexibility of operations with all the different renewables coming onto the power grid. The hydropower fleet has generally gone from operating at a constant power—maybe starting/stopping twice a week—to starting and stopping sometimes eight to 10 times per day on each unit. And within those starts and stops, plants are running from maximum to minimum power swings to regulate the grid. A hydropower plant’s capability to regulate the grid through flexible operations is totally taken for granted. But talk to any operator in a balancing authority control center and they will tell you how valuable the hydro units are. But it is accelerating the aging process of the existing older fleet.”

Lizzie Bonahoom, research associate at Aurora Energy Research, said hydropower still should be considered important to the buildout of renewable energy resources. “Hydro technologies account for just 28% of installed renewables capacity today in the U.S., down from 54% a decade ago,” said Bonahoom, who referenced U.S. totals of 99 GW of hydropower and 184 GW of total renewable energy generation capacity in 2014, levels that are now at 101 GW and 360 GW, respectively.

“These [hydro] projects tend to be older, with only 3% of capacity coming online since 2000. The three different types of large-scale hydropower across the U.S. are conventional hydropower [impoundment] at 79 GW, pumped storage at 22 GW, and run of river [hydrokinetic or diversion] at just under 1 GW. Over half [50 GW out of 79 GW] of existing conventional hydro is located in the West, particularly Washington, California, and Oregon, whereas, most pumped storage is located in the South [10 GW],” she said.

Bonahoom further noted, “Different revenue streams and subsidy structures are available to new build hydropower projects across the U.S. All are supported by federal investment tax credits, which under IRA provisions could reach up to a 50% discount on total project CAPEX [capital expenditure]. Conventional hydropower and run of river are also eligible for the production tax credit, a variable subsidy based on electricity generation. Additional support is available for hydro in the Bipartisan Infrastructure Law, which aims to improve environmental standards and operation of existing facilities, without extending support to new facilities.”

Markets and Competing Technologies Vary by Location

Bonahoom said there are regional differences when it comes to U.S. hydropower. “On a more granular level, all markets in the U.S. have different designs and are influenced by local and state policies in addition to federal policy. For example, hydro would tend to benefit from capacity market payments in markets with capacity payments, such as CAISO’s [California Independent System Operator’s] Resource Adequacy or PJM’s Reliability Pricing Model. In Texas’ market, ERCOT [Electric Reliability Council of Texas], where there is no capacity market, hydro is eligible to participate in smaller ancillary services, such as spinning reserve.”

Bonahoom noted the impact of drought on the hydropower market, and how that can limit investment. “Despite availability of federal tax credits and various other revenue streams, there has only been 3.3 GW of hydro made operational since the year 2010 [all of it conventional], which is small compared to onshore wind [116 GW], solar PV [97 GW], and battery [17 GW] additions in the same time frame,” said Bonahoom.

“Aside from high costs, drought risk presents a significant barrier to development of more hydropower on the system: California’s power market for example is particularly susceptible to drought and a poor water year can reduce hydro output by approximately 10 TWh, approximately 5% of the ISO’s demand in 2023,” she said. “High upfront costs of developing hydro have helped to hamper development. This is reflected in investor interest across competitive ISOs; only 3.1 GW of new pumped storage and 1.7 GW of conventional hydro is currently under development, as opposed to 586 GW of battery storage, 584 GW of solar PV, and 213 GW of onshore wind.”

Bonahoom said that despite lacking investor interest, there is a growing need for dispatchable clean generation in the U.S. to complement rising intermittent renewables generation. “Pumped hydro especially is in a good position to provide value, ‘charging’ when power prices are low and there is sufficient generation on the system, and discharging when the grid is tighter, which will more often coincide with the sun setting,” she noted.

David Pretyman, senior partner of Energy and Utilities at West Monroe, a consultancy group, said, “It’s true that hydropower outputs in the American West have been below average this year and last. However, the variability of a changing climate may also imply that the wet seasons could become wetter, and the dry seasons could become drier. This could potentially destabilize power prices and the overall system makeup in the long term. Dueling proposals and divided allegiances among market participants on the future of a West-wide regional transmission organization could further complicate matters,” he said.

|

|

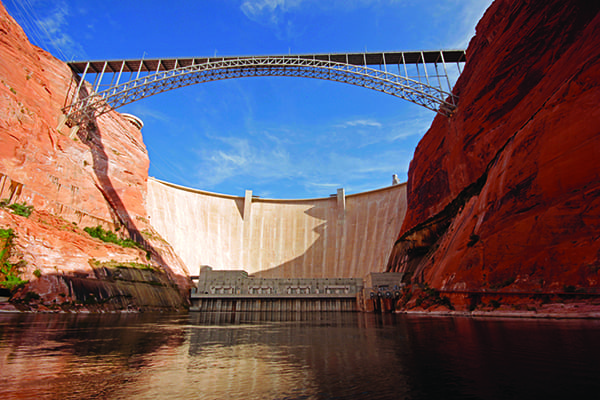

2. The Grand Coulee Dam is the largest hydroelectric facility and largest power plant of any kind in the U.S., with more than 6.8 GW of generation capacity. The dam is located on the Columbia River, about 90 miles west of Spokane, Washington. Source: U.S. Bureau of Reclamation |

Pretyman continued: “For instance, Bonneville Power Administration, which markets wholesale electrical power from many of the large federal hydro facilities in the Northwest [including the Grand Coulee Dam, the largest hydro dam in the U.S. with more than 6.8 GW of generation capacity, Figure 2], supports a day-ahead market proposal from Southwest Power Pool. Meanwhile, California and several surrounding utilities have signed on in support of a proposal to extend California’s market arrangements more broadly to the West. The ultimate framework will have significant implications for how hydropower is valued on the grid.”

Adding New Hydropower Capacity Can Be Difficult

Pretyman also referenced the market dynamics of the U.S. Northeast, telling POWER, “The reality is that the U.S. has largely exhausted its available hydropower resources, with new dam proposals often facing opposition from environmental groups. This opposition is partly driving investor dollars toward transmission solutions. For instance, in the Northeast, the Champlain Hudson Power Express HVDC [high-voltage direct-current] transmission line is set to deliver hydropower from Quebec to serve the New York City load center with substantial amounts of clean energy. This project has been in development for over 20 years. However, another proposed line, intended to bring hydropower to the New England area, was recently canceled despite receiving federal backing. The challenge lies in finding a way to access clean, firm power where solar and wind alone are insufficient.”

The largest hydro project currently planned in the U.S. is the Leslie D. Thatcher pumped storage facility, according to Global Data. The Thatcher PSH project, which would be located in Michigan, is being designed with a total capacity of almost 3.5 GW. Hydropower Highway is the project developer.

Erpenbeck told POWER, “In the U.S., the new hydropower market is going to be focused on pumped storage hydropower. In the energy transition, the value of electricity storage, and particularly long-duration storage, is dominated by pumped storage, where over 90% of the U.S. electricity storage capacity is currently in the existing pumped storage fleet. But it will need to increase and potentially even double to support all the new solar and wind projects. Pumped storage is very dispatchable, but unlike batteries, which are DC power with inverters, these are large synchronous machines that have large amounts of inertia and add stability and reliability to the grid when compared to inverter-based resources. Pumped storage can also run as a synchronous condenser as required by the grid.”

The DOE in a March report wrote: “Hydropower’s longstanding reputation as a reliable source of energy and storage may ironically be one of the reasons people often assume it is ‘tapped out’ of investment opportunities, but this is not the case. Far from being tapped out, hydropower, including pumped storage hydropower, still has enormous potential for growth, particularly for small- and medium-sized projects [or those that produce up to 30 MW of power].”

The DOE noted that less than 3% of the more than 90,000 dams in the U.S. produce power, and said that there are “thousands of non-powered dams offering excellent opportunities for investment. In addition, dams that do currently produce power can often be updated to increase capacity. There are also millions of miles of waterways, including both rivers and canals, that can be utilized for in-stream hydropower.”

“The U.S. should definitely be investing more into new, renewable hydropower development, as well as the existing fleet,” said Erpenbeck. “On the existing plants, the larger plants have been getting investment because they’re so valuable. But the smaller projects have been struggling. Many of these are very old projects—more than 80 years old—that were part of an industrial complex, like a pulp and paper mill, where the megawatts aren’t all that large out of the facility. However, the facility itself and the dams provide recreational lakes and flood control, and the power basically pays for all those public benefits. These are the projects that have been sorely neglected and struggling to find the proper funds to put back into the projects. In terms of new projects, the fact is that many of the best conventional hydro project sites have been built. However, there are many dams in the U.S. that still do not have hydropower on them, over 80,000, and some of these could be developed if we can find sites where there are minimal impacts to powering the dams,” he said.

“I’ve worked in the hydropower industry my entire career and one of the things that I tell people is that every hydropower project is a local tourist attraction, a recreational area, a boating and fishing haven, as well as a tool for flood control, navigation, or water supply—all of that in addition to being a renewable power project,” said Erpenbeck. “Many of the projects have visitors’ centers and museums. I can’t name any other power project that has these things, and they are common on many hydropower projects. We used to say these projects are designed for 100 years, but the reality is that these projects are ‘forever assets’ as one of my clients refers to them.”

Erpenbeck continued: “In addition to long life and local tourist benefits, many of these projects are over 90% efficient. And when designed correctly they can be an environmentally positive force in the community. Yes, hydropower is an older proven technology—but was also the first renewable resource developed in the U.S. The technology has been upgraded over the years, so much so that the new projects are very different than the old historic projects. But, yet, they are taken for granted because they are a legacy asset. We need to look at the future and include what works. We as a power industry need to get back to thinking about multiple bottom-line decision-making and have a longer-term vision than the next five years. Instead, think about the next 50 years, and in the case of hydropower, the next 100-plus years.”

—Darrell Proctor is senior editor for POWER.