Coal generation, as a percentage of total power output in the U.S., declined steadily to 39% at the end of 2011 from about 51% in 2002, while generation from natural gas–fired combined cycle plants grew to more than 20% from 10% over the same period, the Federal Energy Regulatory Commission (FERC) said on Friday as it released its annual assessment for U.S. energy markets.

The reasons for this are well-known, the State of the Markets Report says: new gas generation is cheaper to build, has shorter construction times, and offers more flexible operations with fewer environmental restrictions. However, coal plant construction "has not come to a halt," notes the report. "Coal still maintains a fuel-cost advantage for large base-load plants in certain locations, particularly where delivered coal costs are low."

Natural Gas Production Sees Record Highs

Driven primarily by robust onshore shale gas production, natural gas production reached "an all time record" in 2011, growing 7% in 2011 to 65 billion cubic feet per day (bcfd), and surpassing levels seen last in the 1970s, the report says.

Several key developments have occurred as a result of growing supply, which outpaced demand. The first was that the U.S. had record high natural gas storage going into the 2011/2012 winter. By the end of March, natural gas in storage was 50% higher than the five-year average.

Second, natural gas prices plunged to lows not seen since the early 2000s, falling from the mid-$4/MMBtu at the beginning of the year to under $3/MMBtu, and reaching parity with Central Appalachian coal. The fall in gas prices has not been wholly welcome, notes FERC, however: "Some natural gas producers have voiced concerns that declining revenues due to low natural gas prices will affect their ability to explore for and produce natural gas," the report says. "We have already seen some producers announce plans to cut back natural gas production and drilling in gas only shales while increasing drilling in shales rich in natural gas liquids."

Third, discussions are ongoing to develop new domestic and foreign markets for natural gas. Already, seven liquefied natural gas (LNG) export projects are being proposed in the U.S. with almost 14 Bcfd of capacity.

Finally, "Changes in the pricing relationship between natural gas and coal-fired generators caused a fundamental shift in the utilization of these plants, with natural gas plant production increasing and coal plant output falling," staff said in the report.

Dry gas shales, such as the Haynesville in North Louisiana, the Fayetteville in Arkansas, and the Barnett in the Dallas/Fort Worth area, remained the largest producing shales in 2011. However, the fastest growing shales were found in the liquids-rich shale basins, such as the Marcellus Shale in the Northeast and Eagle Ford Shale in South Texas.

Concerns about hydraulic fracturing remained at the forefront in 2011 as the Environmental Protection Agency continued its study of the relationship between fracking and drinking water (the agency released its final study plan in November 2011, but results are not expected until 2014). "At the state level, actions on fracking range from outright bans, such as the one in the New York City watershed, to the reassessment of current regulations in Ohio, as that state prepares for oil and natural gas development in the Utica Shale," the report says.

While supply soared, natural gas consumption in 2011 rose only 1% compared to 2010, and most growth came from natural gas–fired generation. The report notes that natural gas generators are seeing increased importance in coordination with natural gas pipeline companies, and concerns about coordination have been particularly strong in the Northeast, which is heavily dependent on natural gas and has experienced coincident peaks in both electric and natural gas demand during the winter season. It can also be a concern in parts of the Southwest that "lack robust storage infrastructure." Upcoming coal plant outages for emission retrofits are also expected to lead to greater use of natural gas–fired plants.

Depressed Power Prices, Crawling Demand Growth

In 2011, power prices were depressed throughout the U.S., with the exception of the Electric Reliability Council of Texas (ERCOT) region and the Cinergy trading hub, largely owing to a drop in natural gas prices. Whereas prices in the East were between 3% and 12% lower, and prices in the West fell between 7% and 19% (supported by heightened hydro output in the Pacific Northwest that was 27% above the five-year average), ERCOT prices rose by a stunning 40% as summertime heat resulted in a record-breaking 41 straight days above 100 degrees. "As a result, in August, there were 9 days in which ERCOT’s energy-only market saw day-ahead prices rise to the $3,000/MWh price cap," the report says.

Around the country in 2011, meanwhile, electricity demand climbed slowly, the report says. Industrial demand was up by less than 1% from 2010; commercial sales, driven by a combination of weather and economic activity, also rose slightly in 2011. Residential sector consumption fell 1.5% in 2011, despite record peak loads in many areas of the country during the summer.

Grid congestion was meanwhile alleviated by the new 218-mile, 500-kV TrAIL power line in grid operator PJM’s region that went into service in May 2011. The line begins in southwestern Pennsylvania, crosses northern West Virginia, and terminates in Loudon County, Virginia. “It increased west-to-east transfer capability by over 2,600 MW and has helped reduce congestion bringing prices in eastern and western PJM closer together,” the report says.

A PV, Hydropower Surge

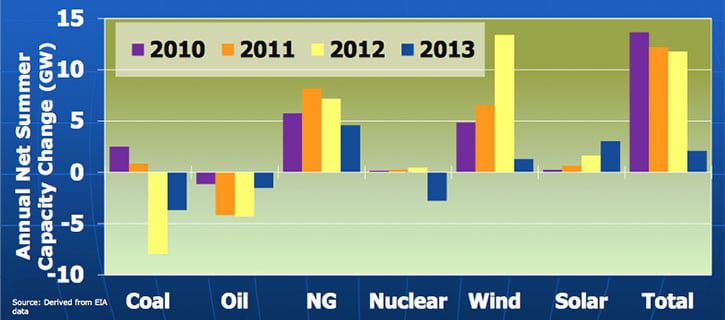

Last year saw a marked rush by renewables developers to connect photovoltaic (PV) solar capacity to the grid before the Treasury Department’s cash-grant program expired. About 1.9 GW in new PV capacity was installed, representing a 109% increase from 2010 levels, led by California and New Jersey. At year-end, total capacity reached 4 GW. "In each of the top states, solar investment was encouraged through policies such as solar set-asides in their renewable standards," the report says. "Additionally, photovoltaic construction costs fell 20% last year, after an 18% drop in 2010."

U.S. wind generation capacity grew 6.8 GW, a third of which came online in the Midwest ISO and Southwest Power Pool. Among the new tools to manage the output of variable energy resources more effectively was MISO’s voluntary tariff category, the report notes. "By allowing registered resources to be dispatched economically in real-time, ‘DIR’ provides more efficient curtailment through market software to manage congestion, a common need in Minnesota, Iowa and other parts of MISO’s western region. Previously, wind resources might be manually curtailed as often as three times daily, with the system instructing wind generators to turn off large blocks of production for long periods of time. By December, 19% of MISO’s 10.6 GW of wind had registered as DIR resources."

Record hydropower generation across the West displaced natural gas–fired generation in 2011. The Pacific Northwest generated roughly 161 TWh last year, while California hydro generation reached 40 TWh—60% above the five-year average. According to the report, California burned 23% less natural gas in its power plants than the five-year average, while Washington State burned 43% less.

Sources: POWERnews, FERC