Renewable energy technologies, including solar, wind, hydro, and battery energy storage systems (BESS), are at the forefront of the global energy transition. The U.S. and Latin America (LATAM) are witnessing significant advancements in these technologies, driven by geopolitical and economic trends. The International Energy Agency (IEA) projects a growth of electricity demand from 1,295 TWh in 2020 to 2,282 TWh in 2040. The projected demand is almost double the installed capacity and poses challenges for some regions. This article explores the latest developments in solar, wind, hydro, and BESS technologies, while addressing insurability and risk perception within the renewable energy environment.

Onshore and Offshore Wind

The global offshore wind market is growing at an almost exponential pace. Offshore wind projects along the East Coast of the U.S. have gained momentum, with streamlined permitting processes and grid integration improvements. James Anderson, a wind energy expert, emphasized the significance of offshore wind, “Offshore wind farms are attracting substantial investments, thanks to advancements in turbine technology and grid integration.”

Latin American countries, including Brazil, Argentina, and Mexico, are also harnessing their wind resources through government auctions and private investments, while community wind projects and hybrid installations are gaining traction. In 2020 alone, 5.5 GW was installed globally, resulting in a total installed capacity of 39 GW. Current trends move wind turbine generator capacities toward 15 MW, and wind farms are beginning to be developed further offshore.

In the LATAM region, though, offshore wind is still in the very early developing stage. Europe and Asia are leading the global development. Although, major LATAM economies, such as Brazil, Mexico, and Chile, had seen a period of rapid expansion, just like North America, the group is falling behind with offshore wind developments. Three decades after the first ever offshore wind farm was built there still aren’t any existing facilities in Latin America.

Energy policy and consistency will be a key indicator to track in the medium term across the region, since this could have a direct impact on how quick LATAM economies transition to net-zero. Taking Brazil´s current election as an example, now that Lula has returned for a third term, future climate and energy policy in Brazil could shape up quite different than that of former president Jair Bolsonaro. The plans for recently privatized power company Electrobras, and the state oil company Petrobras, could come to a halt or shape up quite different under Lula.

This is a tendency that has been seen in the region over the last decade. Latin American regulations and governments could benefit from more consistent medium- and long-term policies, independent of which political party remains in power as we move toward a net-zero economy in 2050. In addition, Latin America generally lacks transmission infrastructure. It is not just a matter of creating new installed capacity in offshore wind, it is also a matter of bringing that capacity from remote areas into the most densely populated cities within the region—something that requires a good amount of capital injection. The opportunity is certainly there for Latin America to exploit offshore wind, but there are still administrative and technical challenges that need resolving before the region can fully explore its potential.

Solar

Solar power has become a cornerstone of the renewable energy landscape, driven by falling costs and favorable policies. In the U.S., utility-scale installations, community solar initiatives, and commercial rooftop systems have fueled substantial growth. Solar power is revolutionizing the energy sector, providing affordable and clean electricity solutions.

LATAM countries like Chile, Mexico, and Brazil are also witnessing remarkable solar capacity additions, supported by favorable regulatory frameworks and programs like auctions and net metering. Data from Global Energy Monitor shows that with roughly 20 GW of solar projects currently in construction, the LATAM region is currently constructing four times more capacity than in Europe and is only behind North America (22 GW) and Asia (110 GW). With another 100 GW in preconstruction or announcement phase, the region is booming.

The key risk for solar farms is related to the weather, especially hail or hurricane damage. Violent hailstorms are not uncommon in Latin America. In 2022, a LATAM airline flight had to make an emergency landing due to substantial damage, which occurred to the plane after it flew straight through a hailstorm. Whether or not climate change is bringing larger and more frequent hailstorms may still be under debate, but the threat is there and cannot be ignored. The World Meteorological Organization registered 16 large hail events in Peru in 2021, and 10 in Chile.

As mentioned above, the infrastructure dilemma applies to solar as it does to offshore (and onshore for that matter) wind. Transmission infrastructure desperately needs development to satisfy the growing energy demand and not compromise energy security, especially with the significant population increase expected in Latin America over the next 15 to 20 years.

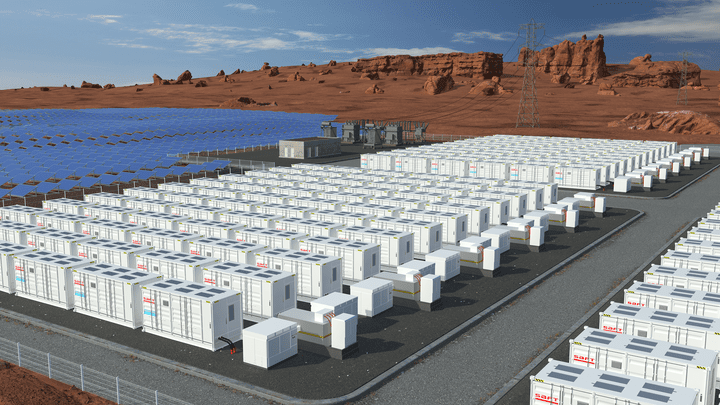

Battery Energy Storage Systems (BESSs)

Battery energy storage systems (BESSs) are instrumental in addressing intermittency and enabling renewable energy integration. The U.S. is witnessing a surge in utility-scale BESS installations, driven by falling costs and energy storage mandates at the state level. LATAM countries, such as Chile, Mexico, and Argentina, are also implementing energy storage projects to enhance grid stability, support renewable integration, and improve energy access in remote areas. Grid-scale battery storage still has a long way to go to catch up with the leading energy storage solution, pumped storage.

Li-ion batteries are still the dominating battery technology applied. Other non-explosive technologies, such as flow battery solutions, exist, but are not yet competitive enough to be competing with Li-ion technologies. The biggest problem with Li-ion batteries is the high risk of thermal runaway, a phenomenon that has caused severe headaches to the insurance industry, in line with current hail-related losses at solar farms in the U.S. Statistics from the Electric Power Research Institute’s (EPRI’s) BESS failure database show 12 global BESS events in 2022, with none of these installations having an age more than 5 years. This presents a huge challenge for developers, original equipment manufacturers (OEMs), and, of course, the insurance market.

And what about Latin America? Chile is still the only country in the region with large-scale storage projects in place, and there is an overall worry in the region that the Inflation Reduction Act implemented by the Biden administration in the U.S. will have a negative effect on BESS development in Latin American.

Hydroelectric Power

Global net hydropower growth expectancy in Latin America is still relatively low and is slowing down compared to other major regions of the world. The projected additions in the region between 2021 and 2030 is 15 GW, a 64% reduction in development compared to the period 2011–2020. This is a large reduction, compared to the global average of 23%.

Risks and Trends in Insurance Coverage

The rapid expansion of renewable energy projects requires careful assessment of associated risks and tailored insurance solutions. “The growth of renewable energy presents unique risks that require specialized insurance coverage. Insurance companies consider factors such as technology risks, natural catastrophe exposure, business interruption, liability concerns, cybersecurity threats, and regulatory changes while assessing renewable energy risks. Insurance companies are evolving their approaches to manage the risks associated with renewable energy projects,” said Stephene Ashikwe, global head of Strategic Risk Advisory at Aon.

To quantify the site-specific asset risk, the estimated maximum loss (EML) or maximum foreseeable loss (MFL) need to be determined. These can be described as the largest, low-probability loss that is foreseen for a specific power generation asset. This is an important parameter for the insurance industry, as it specifies the estimated highest potential insurance claim events expected, which does not necessarily have to be the full value of the power generation asset.

The difference between the EML and the full asset value will determine the savings with respect to insurance premiums. Higher EML means higher premiums, so it is in the asset owners’ interest to keep this as low as possible. Another important aspect when using EML and/or MFL is what sort of insurance limit is required when a project is financed, for example, and lenders sit behind some insurance requirement. It’s important to engage in these discussions at an early stage to be able to optimize premium costs.

Offshore Wind. Construction and installation costs for offshore wind have driven the industry toward the use of a single offshore substation (OSS) for the whole wind farm, which, from an insurance perspective, adds a significant increase of risk and subsequent increased insurance premiums. The role of the OSS is to collect all the power produced from the wind farm, transform the power to the required voltage, and export it back to the substation located onshore. In essence, if the OSS fails, the transmission of electricity stops.

In the event of a full loss of a OSS (such as from a large substation fire or a structural failure of the jacket structure), the whole wind farm would be non-operational for the entire repair/replacement period (lead time), which with the rising shortage of supply vessels globally can be up to 24 months or more. As an example, the total cost of replacing an OSS for a 1-GW or larger offshore wind farm is in the range of $200 million to $300 million. If you add in business interruption (BI) of at least $200 million per year for a period of two years, the total EML would reach at least $600 million. This does not include penalties that might be in place from the power off-taker. The time element coverage (delay in startup [DSU] and BI) has been under the scope of markets in the last few years as conditions such as the volatility clause has taken a front seat when declaring this sum insureds to the markets. Therefore, this critical equipment issue on offshore wind assets would be under heavy scrutiny in years to come.

Solar. The recent large losses due to hail in PV solar plants in the U.S. has driven markets to impose limits on possible coverage in a desperate attempt to respond to million-dollar claims over the last few years. Will this also be the case in Latin America? The combination of the current boom in renewable construction and somewhat unpredictable changes in weather will most likely lead to more large-scale natural catastrophe (NatCat) induced losses. Parametric insurance solutions do exist for specific catastrophic events, and these should be considered given recent extra limitations in policy limits on traditional insurance coverage.

BESS. Thermal runaway is the largest threat to BESS integrity. Spacing of units and effective response from the local fire department are precautional parameters that are not yet fully implemented on all BESS sites nor fully agreed upon by various insurers, OEMs, and project owners. Take the unit spacing requirement as an example. With constantly evolving industry/insurance requirements, a plant, which, for example, might have been up to standards in 2015 might now find itself with new requirements that are not “easy fixes.” This is a known problem and something that should be considered during the project design phase. Insurers needs to be involved early to make sure there are no surprises a couple of years after commissioning.

Hydroelectric Power. Hydro is a mature technology, and the risks determining the coverage are relatively well-understood. That said, construction and operation of hydroelectric plants are not risk free. In 2018, the diversion tunnel collapsed at the 2.4-GW Hidroltuango project in Colombia, causing significant delays and an estimated $2.5 billion in losses. At the 1.5-GW Coca Codo Sinclair project in Ecuador, problems related to quality of the work appeared after commissioning in 2016, and still have not been fully resolved. Besides construction risks and quality issues, NatCat events, such as flooding, need to be re-evaluated every year, especially for assets running on rivers where one dam failure can affect other assets or infrastructure downstream.

What Can Be Done to Reduce the Risk?

The asset owner should determine what the actual risks are already at the feasibility stage of the project, and which ones of these should be transferred to an insurance company. This can be done by analyzing the total cost of risk (TCoR) for various design solutions, as well as by the use of advanced modeling tools, including catastrophic modeling tools. The total cost of risk is exactly that, a measure to determine the overall cost of risk over the entire project lifetime. By managing this parameter, the owner can determine what impact various design solutions will have on the insurance-related costs, losses included. It is possible to obtain a good balance between risk retention (owner takes the risk) and risk transfer (the risk is transferred to the insurer) by effectively using risk management tools at an early stage of the renewable project.

To conclude, solar, wind, hydro, and BESS technologies are driving the global energy transition, shaping the energy landscape in the U.S. and Latin America. Falling costs, favorable policies, and technological advancements are propelling the growth of these renewable energy sources. As insurers carefully evaluate the risks involved, tailored coverage options are being developed to ensure the long-term viability of renewable energy projects in an ever-evolving geopolitical and economic environment. With continued collaboration between industry stakeholders, governments, and insurers, the path to a sustainable future powered by renewable energy becomes clearer.

—Andreas Fabricius is a senior risk control consultant with Aon Global Risk Consulting, Canada, and Daniel Ocampo is Aon Natural Resources Industry leader for LATAM, Mexico.