China’s five largest power generators own half of that country’s power generating assets. Faulty policies and the rapidly changing global economy have made it difficult for these companies to fulfill the high expectations arising from enactment of the Power System Reform Scheme of 2002

China’s State Council (the country’s chief administrative authority) issued the “Power System Reform Scheme” (Scheme) on April 12, 2002. The Scheme represented the first steps taken by the government to reform China’s power sector based on power market principles. The Scheme called for restructuring (“generation unbundling”) state-owned power assets owned by the State Power Corp. into five major power generation corporations and two power grid corporations. The top five power generation corporations (Top 5)—China Hua-neng Group, China Da-tang Corp., China Hua-dian Corp., China Guo-dian Corp., and China Power Investment Corp.—were formally established on Dec. 29, 2002.

By the end of 2010, these five corporations represented 49% of China’s power generation capacity. The Top 5 own about half of China’s power generation assets, and the performance of these five companies, to a great degree, determines the economic health of the entire power generation industry. Today, the Top 5 face seemingly insurmountable problems that threaten their continued existence.

| Table 1. Thermal power capacities of the Top 5, as of 2010. Sources: China Electricity Council, State Electricity Regulatory Commission | ||||||

| Hua-neng | Da-tang | Hua-dian | Guo-dian | China Power Investment | Corporate average | |

| Installed capacity (GW) | 113.43 | 105.90 | 95.31 | 90.19 | 70.72 | 95.11 |

| Thermal power (%) | 87.11 | 80.75 | 85.91 | 75.25 | 69.93 | 79.79 |

Many Industry Challenges Remain

The predicament faced by the Top 5 is caused by three principal factors: soaring coal prices, stagnant electricity market reforms, and unfavorable economic conditions—especially for companies that heavily rely on debt financing.

|

| 1. Coal prices are rising. The Qinhuangdao coal exchange market is the largest coal exchange market in China and is considered to be a leading indicator of China’s cost of coal. Increased imports of thermal coal have also driven up the Top 5’s average coal cost. Courtesy: Baidu Inc. |

Soaring Coal Prices. Coal-fired thermal power generation dominates China’s electric power industry. According to the China Electricity Council (CEC), a joint organization of China’s power enterprises and institutions, thermal power accounts for about 73.41% of the country’s installed capacity and generated 80.76% of its power at the end of 2010. Similarly, the Top 5 relied on thermal power generated by coal for about 80% of their installed capacity in 2010 (Table 1).

Fuel costs for those plants accounted for more than 70% of the total cost of generating electricity. In other words, 56% of the cost of power generation is linked to the price of coal. When coal prices fluctuate wildly, the Top 5’s cost to produce electricity also quickly changes.

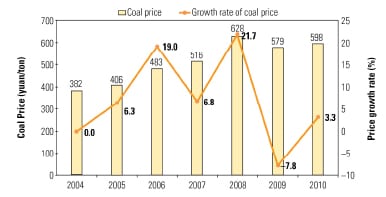

The Chinese government gradually deregulated coal prices beginning in 2002 and completely relaxed the regulation of coal prices in 2005. In recent years, the continuing rise of domestic coal demand and international crude oil prices has sharply pushed up China’s coal prices (Figure 1). In 2008, for example, average raw coal prices rose by 112 yuan/ton ($17.63/ton), reaching a peak price of 628 yuan/ton. About 1.32 billion tons of coal were consumed for power generation that year, which means that the fuel portion of the cost of generating power by all of China’s thermal power corporations increased by 147 billion yuan, leading to an industry-wide loss of 70 billion yuan. This was the power industry’s worst economic loss in history.

Since 2009, coal prices decreased somewhat, although the price has been very volatile (Figure 2). The price of coal began another upward trend at the end of 2010, reaching a peak of 860 yuan/ton on Oct. 23, 2011. The price of coal was in the range of 620 to 635 yuan/ton in mid-August 2012.

Stagnant Electricity Market Reforms. The promise of the Power System Reform Scheme that began the electric power industry’s market-oriented reforms in 2002 was “breaking monopoly, introducing competition.” A decade later, the electricity generation sector has been unbundled successfully, but the electricity price reform portion of the Scheme, part of the core market reforms, has stagnated. The mechanism used to develop the price of electricity is still unreasonable, particularly in light of the other reforms that have been successfully completed.

|

| 2. Average raw coal price for Top 5 power generation corporations, 2004–2010. Since the Chinese government deregulated coal prices in 2002, the market price of raw coal has increased considerably; it peaked at 628 yuan/ton in 2008. The last full year that annual historical prices are available is 2010. Source: China Coal Industry |

At present, the government, not the electricity market, formulates all market electricity prices in China, wholesale and retail. On the generation side, all electricity generators sell electricity to the power grid corporations at a fixed “benchmark price” determined by the government. Customer prices (residential and industrial) are likewise fixed by government tariffs. However, the mechanism to allow competitive bidding for electricity sales by generation companies is still not in place.

The fixed generation price means that the generation companies cannot pass on cost increases, such as the rapidly rising price of coal, to the power grid corporations or consumers in a timely manner. The result has been increasing costs for electricity production but fixed retail rates. Consequently, all of China’s power generating corporations have suffered serious economic losses.

| Table 2. Profit structure of China’s Top 5 power generation corporations, 2008–2010, in 100 million yuan (CNY). As of Aug. 22, 1 CNY = $0.1574. Sources: China Electricity Council, State Electricity Regulatory Commission | ||||||

| Corporation profit category | Hua-neng | Da-tang | Hua-dian | Guo-dian | China Power Investment | Corporate average |

| Thermal power | –85.45 | –128.15 | –140.08 | –110.47 | –138.42 | –120.51 |

| Hydropower | 51.61 | 64.79 | 41.65 | 35.87 | 51.03 | 48.99 |

| Wind power | 9.39 | 14.44 | 5.45 | 47.71 | 3.96 | 16.19 |

| Other | 104.72 | 23.84 | 67.07 | 76.48 | 101.29 | 74.68 |

| Total profit | 80.27 | –25.09 | –25.91 | 45.59 | 17.86 | 18.54 |

Unfavorable Economic Conditions. In the fourth quarter of 2009, China began to implement a tighter monetary policy to deal with rising inflation. The Chinese central bank (the People’s Bank of China, PBC) has raised the loan interest rate and deposit reserve rate of commercial banks five times and nine times respectively since early October 2009. The undesirable side effects of the PBC’s actions were reduced funds supply, limited credit, and soaring capital project financing costs. As capital-intensive enterprises, power generation companies are facing a soaring interest expenditure on existing liabilities (commercial bank loans) and unprecedented difficulties in finding a means to finance construction of new power generation facilities.

|

| 3. Serious business predicament. Ningde thermal power plant of Da-tang Corp. is located in Fujian Province of China. The liabilities/assets rate of Ningde thermal power plant was 98.69% at the end of 2010, which was much higher than the warning limit of 85% set by SASAC, and the total net profit was –22.275 million yuan. Courtesy: Baidu Inc. |

One possible solution is to accept private equity investment to offset the high cost of commercial bank loans. But that approach doesn’t answer the question of what entity would be interested in investing in these troubled corporations without significant market pricing reforms. Also, the power generation corporations have traditionally used debt financing to build new facilities and have little to no experience with private equity investment because the corporations have never been an attractive investment.

The Result: Poor Financial Performance

Unlike the thermal power business, other power-related businesses—such as wind power generation and coal production—have guaranteed profits. The thermal power business, operating as independent corporations, has experienced little retail rate relief while the cost of fuel has significantly increased. The results are predictable: very poor financial performance. From 2008 to 2010, the Top 5 lost the business equivalent of about 12 billion yuan, about $1.88 billion (Table 2). Given the current unstable economy and the Top 5’s heavy reliance on thermal power for income and profits, these companies’ poor economic performance is expected to continue until electricity market reforms are completed.

A close look at Table 2 will reveal that the thermal power portion of the portfolio is the cause of the overall poor financial performance for the Top 5. In fact, the thermal power portion of the portfolio has pushed the many financial ratios used to evaluate corporate performance out of the acceptable range. Two of those ratios are the liability/asset rate and the rate of return on equity capital.

| Table 3. Percentage of liabilities to assets for China’s Top 5 power generation corporations. The five corporations were established in late 2002, so the 2003 data reflects the first full year of operations. Sources: China Electricity Council, State Electricity Regulatory Commission |

||||||

| Hua-neng | Da-tang | Hua-dian | Guo-dian | China Power Investment | Corporate average | |

| 2003 | 62.30% | 67.10% | 70.70% | 71.40% | 64.80% | 67.26% |

| 2007 | 76.40% | 79.30% | 82.60% | 80.70% | 74.70% | 78.74% |

| 2008 | 81.80% | 86.70% | 88.00% | 85.30% | 82.10% | 84.78% |

| 2009 | 84.50% | 88.60% | 87.70% | 81.80% | 84.40% | 85.40% |

| 2010 | 83.95% | 87.48% | 88.65% | 82.29% | 83.78% | 85.23% |

| Table 4. Financial performance of Top 5 power generation corporations, 2002–2010. Profits and equity capital are shown in 100 million yuan (CNY). As of Aug. 22, 1 CNY = $0.1574. The Top 5 was formed in late December 2002, so 2003 data reflect the financial results of the first full year of operation. Sources: China Electricity Council, State Electricity Regulatory Commission |

||||||||||

| Corporation | Economic indicator | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

| Hua-neng | Total profit | 43.5 | 63.8 | 73.6 | 80.9 | 96.2 | 101.7 | –58.4 | 60.8 | 69.8 |

| Investment | 475 | 527 | 590 | 735 | 798 | 936 | 814 | 949 | 1016 | |

| ROEC (%) | 9.2 | 12.1 | 12.5 | 11 | 12 | 10.8 | –7.2 | 6.4 | 6.9 | |

| Da-tang | Total profit | 19.1 | 26.5 | 31.1 | 36.3 | 55.5 | 75.6 | –63.2 | 22.9 | 15.1 |

| Investment | 341 | 363 | 380 | 497 | 502 | 617 | 554 | 583 | 654.9 | |

| ROEC (%) | 5.6 | 7.3 | 8.2 | 7.3 | 11 | 12.3 | –11.4 | 3.9 | 2.3 | |

| Hua-dian | Total profit | 16 | 10.1 | 12 | 18.5 | 30.5 | 42 | –68.8 | 20.9 | 25.3 |

| Investment | 255 | 263 | 281 | 315 | 396 | 422 | 373 | 436 | 559.4 | |

| ROEC (%) | 6.3 | 3.8 | 4.3 | 5.9 | 7.7 | 10 | –18.5 | 4.8 | 4.5 | |

| Guo-dian | Total profit | 8.9 | 14.3 | 22.4 | 30.5 | 41.3 | 48 | –71 | 59.6 | 61 |

| Investment | 199 | 215 | 234 | 333 | 394 | 474 | 440 | 766 | 968.7 | |

| ROEC (%) | 4.5 | 6.6 | 9.6 | 9.2 | 10.5 | 10.1 | –16.1 | 7.8 | 6.3 | |

| China Power Investment | Total profit | 14 | 13.9 | 14.7 | 20.4 | 39 | 45.3 | -69.5 | 37.2 | 50.2 |

| Investment | 305 | 242 | 245 | 255 | 278 | 559 | 491 | 581 | 664.6 | |

| ROEC (%) | 4.6 | 5.7 | 6 | 8 | 14 | 8.1 | –14.1 | 6.4 | 7.6 | |

High Liability/Asset Rates Persist. An easy and effective method of gauging a company’s finances is to examine its assets and liabilities. A too-high liability-to-asset rate is a common problem faced by each of the Top 5 power generation corporations. At the end of 2003, one year after the founding of the Top 5, the average liability/asset rate was only 67.26%, which is much lower than the warning limit (85%) set by the state-owned Assets Supervision and Administration Commission (SASAC). However, at the end of 2010, the average liability/asset rate of the Top 5 increased substantially, and got to 85.23% (Table 3), exceeding the SASAC-set warning line. A liability/asset rate exceeding 85% means the corporation is taking a considerable risk of insolvency—a sure sign of significant economic distress. A financially healthy power generation company will have a liability/asset rate well below 85% in China, according to SASAC’s rule.

According to SASAC reports, of the 436 thermal power firms operated by the Top 5, 85 firms (about 19%) had liability/asset rates approaching 100% and were on the verge of bankruptcy at the end of 2010 (Figure 3). Large amounts of debt taken on by the Top 5 over the past few years, caused by their poor profitability, is part of the explanation for the high liability/asset rate. One of the direct results of a high liability/asset rate is soaring interest expenditure. In 2010 alone, the interest expenditure of the Top 5 reached 70 billion yuan, which was 5.4 times the net profit of the Top 5 over the same period. The overall economic condition of the Top 5 further deteriorated.

The Rate of Return on Equity Capital Is Low. For the years 2003–2010, with the exception of 2008, the Top 5 were overall profitable corporations (Table 4). The 2002 data reflects performance during the year prior to forming the Top 5 in December 2002.

One way to evaluate the quality of corporate profitability is the relationship between equity and profits, or the return on equity capital (ROEC) rate. As you can see in Table 4, the ROEC is relatively low, which means that the profit generated by the Top 5 is low compared to the large amount of equity capital (normally borrowed debt) invested. From 2003 to 2010, the average ROEC rate of the Top 5 was 5.42%, which is much lower than the interest rates of bank loans. In effect, depositing equity capital into a bank savings account has been more profitable than investing in the power generation business.

In sum, the Top 5 are caught between two seemingly immovable barriers. The first barrier is the burdensome debt that has weighed down corporate profitability since the power corporations were formed in 2002. Poor balance sheets have also limited the equity financing option because there are better investment opportunities in profitable industries. The second barrier is the stagnation of the market pricing reforms promised by Power System Reform Scheme a decade ago.

Until the Top 5 are able to market price electricity to reflect the true cost of production, particularly the price of purchased coal on the global market, there is little hope of a quick return to profitability and fulfilling the original promise of “breaking monopoly, introducing competition.”

— By Zeng Ming, Li Chen (lichenbj@126.com), Ma Mingjuan, and Zhou Lisha, North China Electric Power University, Beijing, China. The Energy Foundation supported the work described in this paper (G-1006-12630).