Despite the U.S. and Europe shuttering coal-fired power plants, coal remains a major fuel in global energy systems.

In 2018, global coal demand rebounded and grew by 1.4% due to increased consumption in Asia, where coal consumption increased by 2.5%. This increased consumption was mainly from power generation, which reached an all-time high, increasing 3% in 2018 and accounting for almost 40% of global electricity generation.

China remains the world’s largest coal consumer, using more than 50% of all the coal consumed in the world. According to China’s National Bureau of Statistics, China relies on coal for 57.7% of its primary energy, and for 67% of its electricity.

And China isn’t the only major coal user in Asia. India led all countries in coal consumption growth, increasing its consumption in 2018 by 36 million metric tons oil equivalent—8.7% higher than in 2017. India generated 75% of its electricity from coal in 2018.

Both countries have sizable coal reserves of more than 100 billion metric tons. But, both countries also import coal, together accounting for more than one-third of the world’s coal imports in 2018.

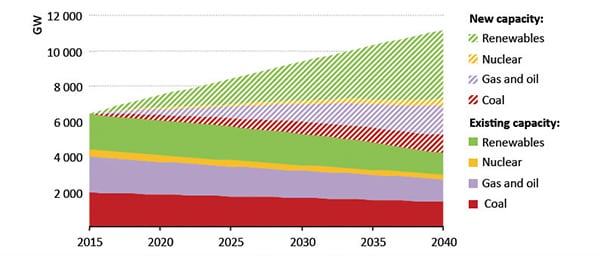

According to the International Energy Agency (IEA), global coal demand is expected to decline in 2019 but remain broadly stable over the following five years, supported by robust growth in major Asian markets. Despite that growth, coal’s share of electricity generation is expected to decline—from 38% in 2018 to 35% in 2024. Regardless, coal is expected to retain its status as the single largest source of power supply worldwide.

China

China is the world’s biggest producer and consumer of coal. IEA expects China’s coal consumption will plateau around 2022 due to a decline in coal use in the residential, small industrial, and heavy industrial sectors, driven by structural changes in the economy and the need to reduce local pollution.

Residential use of coal is a major contributor to localized pollution because it is largely burned in an uncontrolled environment, without the technologies and modern pollution reduction capabilities of larger users. China’s coal power generation, however, is expected to continue to grow, just at a slower rate, dropping its share of the power generation market from 67% in 2018 to 59% in 2024. It is believed that coal is needed to sustain China’s economic growth and guarantee energy security in the future.

China’s reliance on coal helped it become the world’s second-largest economy, pulling nearly a billion people out of poverty. Basedon recently released official economic data, and found 65% of the annual growth in energy consumption in 2019 came from fossil fuels, with coal accounting for 57.7% of China’s energy use. Coal plants, which burn approximately 54% of all coal used in the country, provide 52% of generating capacity and 67% of electricity output.

Despite China’s generation sector being at overcapacity, China added about 40 GW of coal-fired power capacity in 2019—a 4% increase. As a result, the coal fleet’s average utilization rate fell below 50% on average. Even so, China is still building new supercritical coal-fired generators with 100 GW under construction, which would raise current coal capacity by nearly 10%.

Coal Power Overcapacity

China’s coal power overcapacity dates back to the 12th Five-Year Plan, which was formulated in the early 2010s in response to the global financial crisis and was part of the largest economic stimulus program in its history. It targeted a huge expansion in coal mining and coal-fired power generation.

In 2014, China transferred the central government’s authority to approve new coal-fired power plants to the provincial level in order to cut red tape. Because many local governments wanted to increase their economies, and create demand for locally mined coal and jobs through new power projects, about 210 projects with a capacity of 169 GW were rubber-stamped in less than a year. This surge of new projects came as demand for coal-fired electricity declined from 2013 to 2015, moving the central government to curtail approvals and suspend already permitted projects.

Under China’s existing 13th Five-Year Plan, coal power capacity is capped at 1,100 GW. Ahead of China’s release of its 14th Five-Year Plan later this year, stakeholders, such as the network operator, State Grid, and an industry body, the China Electricity Council, are lobbying for targets that would allow hundreds of new coal-fired power stations to be built. State Grid indicated that coal power capacity be at 1,200 GW to ensure the reliability of the power system and to allow key power generating regions to retain some backup and reserve capacity.

The China Electricity Council argued that coal power capacity should reach 1,300 GW by 2030, up from 1,050 GW today, based on its projections for annual electricity demand and the need for capacity to meet peak loads. For comparison, the U.S. had 227 GW of coal generating capacity in February 2020. The 1,300 GW of capacity for China in 2030 would imply the addition of more than 300 GW of new supercritical coal-fired capacity this decade due to the retirement of older, polluting and inefficient plants. With 100 GW of new coal power under construction, another 200 GW of capacity would have to secure permits and financing.

South and Southeast Asia

India’s goal is to become a $5 trillion economy by 2024, in part by investing heavily in infrastructure, which will boost energy demand for industry and electricity production.

Although India has succeeded in bringing some form of electricity access to almost all its citizens, the country’s per-capita power consumption is still low, allowing it to still grow significantly. Despite power generation from renewables expected to increase fourfold between 2018 and 2024, the IEA expects India’s coal power generation will increase by 4.6% per year through 2024, and for India’s coal demand to grow by more than that of any other country in absolute terms over the five-year forecast period. Pakistan has recently commissioned more than 4 GW of new coal power plants and has a similar amount under construction. Bangladesh is about to commission the first unit of 10 GW it has planned.

The IEA expects coal demand in Southeast Asia will grow by more than 5% per year through 2024, led by Indonesia and Vietnam. The region’s strong economic growth is expected to drive electricity and industrial consumption, which will both be fueled in part by coal. Southeast Asia countries are also using coal to provide electricity for their growing populations.

Coal’s future is primarily in the electricity generation markets in Asia, with China, India, and Southeast Asia continuing to build coal-fired generating capacity. The IEA expects generation from coal power plants in Asia will exceed the drop in coal-fired generation in the U.S. and Europe so that coal remains the world’s largest generation fuel over the next five years.

Coal may be struggling in the U.S., but it’s still king worldwide, and likely to remain so with Asia as its primary customer.

—Mary Hutzler is a distinguished Senior Fellow at the Institute for Energy Research. She has more than 25 years’ experience at the Energy Information Administration (EIA), where she served as Acting Administrator and specialized in data collection, analysis, and forecasting.