To remain competitive in power markets increasingly characterized by disruptions, NRG Energy plans to accelerate its transition from a pure independent power producer (IPP) model to a more simplified customer-driven integrated power model that favors its retail businesses.

In a number of presentations showcased on March 27 as part of NRG’s 2018 Analyst Day, company executives described the move as imperative for NRG’s financial health. The “value” in the industry, which is facing low commodity price futures, including for natural gas and renewables, is generally moving from power plants to customers, they said.

A Turbulent History

Incorporated on May 29, 1992, NRG Energy held its stance as a pure IPP until 2009, despite being forced into bankruptcy after Enron Corp. collapsed in 2001 and thwarting multiple takeover bids, including from Mirant Corp. in 2006 and Exelon Corp. in 2008. In 2009, the company, which then had a generating fleet of about 23 GW, took its first step toward an integrated portfolio with the purchase of Reliant Energy, a company spun off from Houston Lighting and Power. Reliant served 1.6 million customers in Texas at the time.

“Back then, gas was high—double digits—and retail was thought of as a hedge for the generation fleet—not the reverse,” noted Chris Moser, executive vice president of NRG’s operations, on March 27.

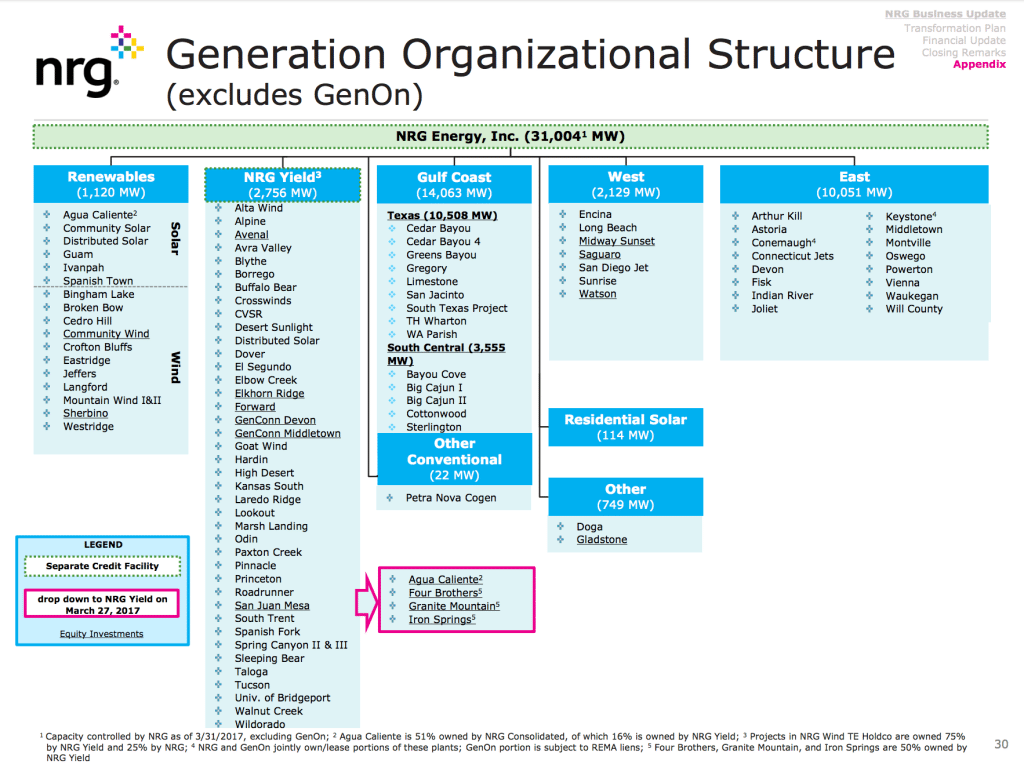

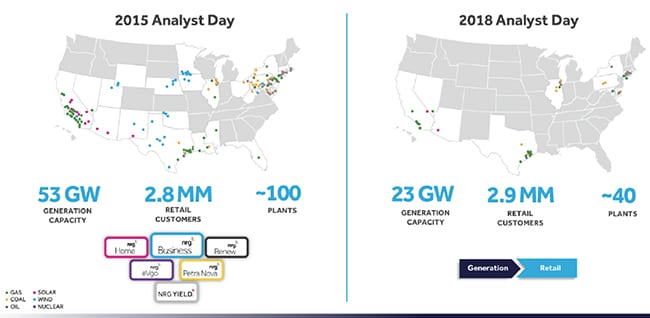

Between 2012 and 2015, caught up in a wave of consolidation within the IPP sector, NRG doubled its fleet to 53 GW, buying GenOn Energy in December 2012 for $1.7 billion and acquiring the assets of bankrupt merchant generator Edison Mission for $2.64 billion in 2014. “The main thesis here was eliminating costs by realizing synergies as we combined different companies,” Moser said. “The expansion vastly increased our presence across the Northeast, California, and Chicago. But value migrated away from the assets and towards customers and relationships with customers. We began streamlining our fleet to better match retail and stay in markets that we liked—in effect reversing who was the hedge from whom.”

In May 2017, however, NRG moved to relinquish GenOn to bondholders, saying the company had racked up a high debt burden relative to cash flow, and that it had been financially crippled by falling wholesale power prices and capacity prices, which were spurred primarily by the glut of cheap gas depressing power prices. This February, as part of a transformation plan announced in July 2017 to cast off $13 billion in debt and generate more free cash flow, NRG also moved to divest the bulk of its renewable assets under NRG Yield and sell about 3.6 GW tied to its South Central Generating business.

And now, as part of its transformation plan, the company is working to slash its exposure to “negative” market trends, and it has deemed a combination of generation and retail as the best path forward to reduce risk and improve stability of earnings, Moser said.

Once GenOn’s exit is complete, NRG’s fleet will shrink by more than half to 23 GW from 40 power plants, but the company will retain 2.9 million retail customers. The new fleet—characterized by 46% natural gas generation, 31% coal generation, and 15% oil generation—will comprise 11.5 GW of generation in Texas, “a very tight market and the only one with any load growth,” Moser noted. It will also include 9.7 GW in the East, most that “has enjoyed strong capacity prices due to being in premium zones.” Finally, the company will retain about 2.6 GW in the West, “which continue to support reliability, even as California fearlessly forges its own unique energy future.”

Banking on Market Trends

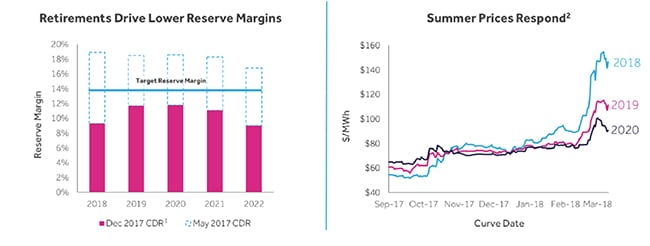

According to Moser, the streamlined fleet is strong, especially considering mixed market trends that are currently impacting generation. At a macro level, mixed asset retirements are reshaping supply stacks, most notably in the Electric Reliability Council of Texas (ERCOT), where load growth averages about 2% on a normalized weather basis, he said.

Earlier this month, ERCOT suggested that retirement of older generating units and high peak usage owing to economic growth could tighten operating reserves this summer. Moser noted that NRG stands to benefit. “Texas looks tight this summer, and it looks to remain that way for a while,” owing to a “continued delay of new conventional generation,” he said. As reserve margins are driven lower, prices will soar, he predicted. That’s a boon for NRG, which saw about 1 GW of capacity driven out of the ERCOT market “due to persistent low prices and an energy-only structure.”

Some experts predict ERCOT prices could soar this summer from about $35/MWh sustained over the past few summers to $150/MWh in response to the increased threat of scarcity. “That last violent move up” is in part a reaction to ERCOT’s Seasonal Resource Adequacy Report, which shows the grid entity could have only 550 MW available for operating reserves, Moser said. Three other scenarios ERCOT modeled that hinged on more outages and less wind showed ERCOT could suffer shortages of 2 GW, he said.

> While ERCOT’s reserve margins are expected to increase in the summer of 2019 to 11.7%, that projection assumes more than 10 GW will be added to the grid—7 GW of renewables and 3 GW of natural gas. But that capacity may not come online, Moser suggested, because the current market doesn’t support new builds. “That new gas has been pushed back year after year and looks to be slated for 2020 rather than 2019. As for renewables, the actual amount billed has historically come in about half of what [ERCOT’s Capacity, Demand and Reserves Report] has forecast. Adjusting either assumption means that the 2019 reserve margin will end up well below the current forecast, which is low to begin with,” he said.

While ERCOT’s reserve margins are expected to increase in the summer of 2019 to 11.7%, that projection assumes more than 10 GW will be added to the grid—7 GW of renewables and 3 GW of natural gas. But that capacity may not come online, Moser suggested, because the current market doesn’t support new builds. “That new gas has been pushed back year after year and looks to be slated for 2020 rather than 2019. As for renewables, the actual amount billed has historically come in about half of what [ERCOT’s Capacity, Demand and Reserves Report] has forecast. Adjusting either assumption means that the 2019 reserve margin will end up well below the current forecast, which is low to begin with,” he said.

Moser also said the situation wouldn’t improve markedly through 2020. “The market is basically flat to the annual revenue requirement of a [combined cycle gas turbine] in 2020 for a single year. After that single year, the current market doesn’t support new builds at all,” he said. Renewables like wind and solar may remain profitable if subsidies are sustained, but the wind production tax credit is slated to end after 2019. Meanwhile, infrastructure to move more wind is sorely lacking, he suggested. The Competitive Renewable Energy Zones (CREZ) were designed to move 18 GW of power, but there is currently 20 GW of wind on the system. “The practical importance of that is that the CREZ lines are saturated more often than not.”

The East, meanwhile, is seeing several proposed energy and capacity reforms, “all of which are positive” for NRG’s fleet, Moser noted. In PJM’s energy markets, price formation reform could allow inflexible units to set prices—and increase them by $3 to $4/MWh. And in February, PJM filed “constructive comments” in a Federal Energy Regulatory Commission (FERC) fast start docket, which is part of the regulatory body’s investigation into whether tariff revisions are required for pricing of resources committed to real-time response of unforeseen system needs. “And what they did was to actually expand the number of units eligible to set market prices beyond FERC’s original request,” Moser said. “FERC was originally talking about a one-hour minimum run and start time, and PJM is trying to expand that to two. This is in lockstep with PJM overarching price formation efforts, which were recently highlighted in testimony before Congress.” PJM is expected to release more information about allowing inflexible units to set prices and potential improvements to scarcity pricing, he added.

PJM may also soon file two different options before FERC “aimed at eliminating the pernicious price impact of state subsidies,” Moser said. On a national level, while FERC rejected the Department of Energy’s controversial proposed rule on grid reliability and resilience pricing, Moser said “the seeds that the DOE planted [concerning its promotion of onsite fuel at power plants] may be beneficial” to NRG’s solid-fuel fleet.

But NRG is bracing for market trends that could adversely impact the business, too, Moser said. These include: “Natural gas prices that have settled into the low stable range and show no signs of budging, and renewables, which have arrived in several supply stacks, aided mostly by subsidies. Finally, disruptive technologies like batteries can have a negative impact, but they show no likelihood of economic adoption anytime soon,” he said.

For NRG, the drive to pursue an integrated portfolio should be focused on matching generation with retail, Moser suggested. “Even with a low capacity factor, eastern generation covers retail’s take and because the size of the fleet is also greater than retail peak load, we have plenty of generation to flex up as retail grows,” he said.

For NRG, the drive to pursue an integrated portfolio should be focused on matching generation with retail, Moser suggested. “Even with a low capacity factor, eastern generation covers retail’s take and because the size of the fleet is also greater than retail peak load, we have plenty of generation to flex up as retail grows,” he said.

—Sonal Patel is a POWER associate editor (@sonalcpatel, @POWERmagazine)