The Federal renewable energy production tax credit (PTC) was created when Congress enacted the Energy Policy Act of 1992. The PTC for renewable energy generating projects signaled the birth of the modern renewable energy industry in the United States. In the years since, the industry has grown in fits and starts, including the creation of the investment tax credit (ITC) in 2005. There have been no less than six extensions of the PTC over the years.

With President Obama’s 2008 election and the passage of the American Recovery and Reinvestment Act of 2009 (ARRA) following closely on the heels of the worst economic meltdown since the great depression, the green energy industry emerged from its infancy, demonstrating the hallmarks of a mature industry:

- Project capacities measured by the hundreds of megawatts

- Tens of billions of annual investment dollars from well-heeled banks and institutional investors

- Photovoltaic solar penetration at the household consumer level

- Growth of average monthly energy output from 10,508 GWh in 2008 to 18,777 GWh by the middle of 2012

- Increase of total installed capacity to approximately 70 GW, accounting for 38% of all new installed capacity in the first half of 2012

- New technological concepts like offshore mega-wind and solar thermal energy capture/storage

But undeniable as the growth of renewable energy industry has been, many hallmarks of its infancy remain:

- Technological growing pains

- Volatility resulting from rapid and unpredictable technological and political change

- Persistent company failure and industry consolidation

- Continuing dependence on government incentives

The political, financial and economic maelstrom of the past four years has yielded uncertainty over exactly how grownup green energy is. Emergence from the regime of stimulation and subsidy promises to answer the question in short order. The potential vacuum created by the saturation and expiration of green energy incentives presents new challenges for the financing of renewable energy projects and should transform the landscape in a post-incentive financing world.

Mother’s Milk: Historical Renewable Energy Incentives

Three forms of sustenance have nurtured the renewable energy industry: Federal tax credits, accelerated depreciation, and state incentives. Federal tax credits have historically included the PTC, providing tax credits for each kWh of generation over a ten year period, and the ITC, offering tax a tax credit equal to 10% or 30% percent of installed plant cost following initial asset deployment. Under Section 1603 of ARRA, projects that commenced construction during 2009, 2010, or 2011 were eligible to convert the PTC into an ITC and claim a cash grant in lieu of the tax credit.

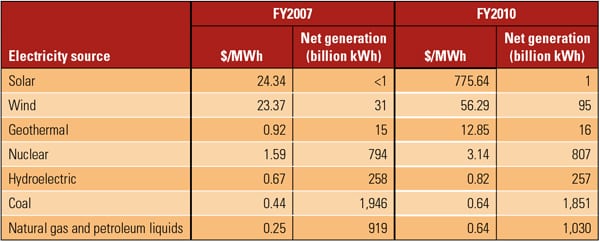

A summary of renewable energy technologies with corresponding tax credit incentives and expiration dates is as follows:

Table. Expiration dates of existing renewable subsidy payment.

In addition to tax credits, the federal government has traditionally permitted renewable energy project developers to depreciate 50% of the cost of their equipment over an accelerated five-year period. ARRA further compressed accelerated depreciation, permitting first-year 100% depreciation of a project placed into service before 2013.

Federal tax policy has been the cornerstone to U.S. renewable energy policy, but in recent years state and local action has also proven a valuable industry driver. Thirty states and the District of Columbia have established renewable portfolio standards (RPS) requiring utilities to procure a portion of their energy from renewable resources. Aggressive portfolio standards have resulted in heavy utility subscription to the renewable energy and renewable energy certificate procurement markets. Consequently, many RPS programs are at or approaching saturation, procurement activity has slowed and pricing for green energy attributes has fallen substantially.

Growing Up In a Post-Subsidy World

Federal tax incentives can represent between 50% and 60% of the installed costs for a renewable energy project. The possible expiration of tax incentives has naturally led to doubts about the readiness of renewables to compete in mature energy markets. The downturn in the wind market in 2012 with tax credit expiration looming shows that additional policy initiatives are needed to propel the U.S. green energy industry from adolescence to adulthood.

Loss of tax incentives and saturation of green energy programs will necessitate either new sources of revenue or increased cost reductions to fill the hole in subsidy-free project economics. Short of a long-term extension of tax credits and expansion of RPS objectives, the recipe for continued industry growth may include some combination of (a) increased competitiveness, (b) feed-in tariff policy, (c) master limited partnership structures, (d) asset securitization, (e) increased strategic investment, and possibly (f) “leveling the playing field” between renewable and conventional energy generation.

Increased Competitiveness

In parts of the world where energy costs are high, renewable energy can be conventionally competitive. In the U.S., where fossil fuels are cheap and abundant, the market for renewables is challenging. If a positive slant can be placed on the U.S. energy environment for renewables, it is the potential to use policy and financial instruments to drive continued technological improvement and efficiency.

A combination of technological improvement, increased scale, and government policy has reduced the cost of renewable energy deployment in the past four years. The cost of solar technology in particular has been reduced from installed costs of approximately $7.50 per watt in 2009 to as low as $2.65 per watt in 2012. Moreover, improvements in the size and efficiency of renewable technology have resulted in higher capacity factors and lower levelized energy costs. Similar improvements must continue across the industry for renewables to be a mature segment of the energy sector.

Feed-In Tariffs

For years some European countries have nurtured their renewable energy markets by implementing feed-in tariff programs that compel utilities to buy green energy at administratively determined power purchase rates. The rigid price signal from European feed-in tariffs has produced mixed results. Positively, installed capacity has grown exponentially, resulting in the creation of a vibrant renewables manufacturing and installation industry. At the same time, artificial administrative pricing has frequently resulted in overpricing and ultimately unforeseen tariff rate reductions that have injured the industry.

Some U.S. state and local governments are taking a cue from European markets and beginning to develop their own feed-in tariff programs, in some cases with an American entrepreneurial slant. Rather than administrative tariff pricing, some U.S. tariffs, like those developed in California, award contracts based on a reverse auction, with the lowest price bidders winning off-take contracts.

With reverse auctions either (1) prevailing bidders will underprice their bids and projects will not be built; or (2) bidders will accurately price their bids and projects will be successful. Under customary program rules, the capacity associated with incomplete projects is returned to the procurement pool to be re-bid. Correctly priced projects may be elbowed out of the way by more aggressive bidders in the short term, but in the long run, as completion costs become more certain and bids become more realistic, viable tariff rates are likely to prevail.

Master Limited Partnership

One competitive advantage that conventional energy has enjoyed over renewables is access to the master limited partnership (MLP) corporate structure. The MLP structure allows for interests in energy projects to be sold to investors in public equity markets. There is some support for applying this structure to renewable energy projects, enabling them to access a broader range of investors and, by increasing capital supply, reduce financing costs.

Implementation of the MLP structure for renewable energy will not, absent changes to passive loss rules in the tax code, enable MLP investors to monetize tax losses and other benefits enjoyed by renewable energy companies (to the extent they are not extinguished). Notwithstanding that inefficiency, access to the public markets would improve project economics and help drive the continued growth of the industry.

Securitization

Since the financial meltdown of 2008 amid the collapse in value of bundled mortgages, “securitization” has become, in many minds, a dirty word. Total asset-backed securitization issuances in the U.S. have declined from $754 billion in 2006 to only $125 billion in 2011. Though much of the bathwater has been disposed of, some, including those in the renewable energy industry, hope to preserve a healthy baby.

Securitization bundles pool tranches or classes of asset-backed investments to diversify asset performance risk in a single portfolio offering. The benefits of securitization are two-fold: (1) diffuse risk theoretically enables the issuer to obtain a lower cost of capital and (2) division and bundling of assets facilitates divestiture for investors and issuers. The Dodd-Frank Act imposes restrictions on securitization that may make it more complex and expensive, but the concept of improving capital cost and liquidity holds some promise for the industry.

Strategic Investment

Renewable energy investment has mostly been limited to a small list of commercial banks, insurance companies, utilities, and institutional investors. A few strategic investors like Google have become active in the market, but most of corporate America has ignored investment in renewable energy projects. This is due in part to the conservative returns associated with it.

But in a volatile world where the perception of risk-free government credit is eroding, companies with significant cash reserves may be looking for safe investments that earn a reasonable rate of return. Contracted project financings may present such an opportunity for cash-rich investors, particularly when combined with the liquidity afforded by MLP and securitization vehicles. Moreover, as the industry matures, the discovery of synergies and strategic advantages in renewable energy developers and equipment manufacturers becomes increasingly likely.

Leveling the Playing Field

One argument for abandoning renewable energy subsidies is that the free market, rather than the government, should pick winners and losers. Proponents of this argument often ignore the subsidies enjoyed by fossil fuels, estimated at between $775 million and $1 trillion worldwide for 2012. Comparatively, 2010 global subsidization of renewable energy has been estimated at about $66 billion. If current U.S. renewable energy incentives are not renewed, the industry could stay competitive by “leveling the playing field” between renewables and fossil fuels, either by eliminating existing conventional subsidies or by extending them to renewables.

This approach has problems. It is not clear that renewable energy, which has enjoyed a very short period of subsidization, can compete on a level field with fossil fuel projects, which have had U.S. subsidies since 1916. Further, a “level” field, where there is no cost to oil, gas or coal fired plants for externalities such as resource protection or pollution, would not accurately reflect the relative cost and benefit of renewable energy compared to fossil fuels. This suggests that a comprehensive carbon pricing mechanism is needed to balance the competition.

The End of Adolescence?

When will the U.S. renewable energy industry emerge from its adolescence? The end of the subsidy-rich environment enjoyed over the last decade will hold the answer, though it seems the industry will not mature further without policy initiatives that reflect the true cost and value of energy. Still, the technology-neutral policy discussion, continued equipment cost reduction and rapidly increasing competitiveness, suggest that an adult renewable energy industry may not be far off.

—Daniel Sinaiko is a partner in the global project finance group at Akin Gump Strauss Hauer & Feld LL. Brett Fieldston, an associate at Akin Gump Strauss Hauer & Feld LLP, contributed to this article.