For all the words published over the past several years about electric utility customer defection—thanks to the combination of lower-cost residential solar photovoltaic systems, tax incentives, and net metering—the customer class utilities are more worried about is the commercial and industrial (C&I) one. That’s because losing one C&I customer can be the equivalent of losing hundreds to many thousands of residential customers. Two trends indicate how large energy users are gaining increasing advantages when it comes to power sources and prices.

Rate Gap Between Classes Is Widening

Most readers already know that C&I customers enjoy lower rates than residential customers and that electric tariff dealmaking is one way states and their utilities court new business. That’s not necessarily a bad thing, as the net benefit to states in terms of jobs and revenue can be offsetting.

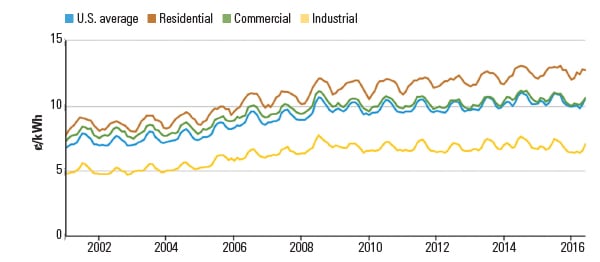

The gap between customer classes varies by state but is highest in New York. There, industrial customers pay on average 6¢/kWh while residential customers pay on average 17.17¢/kWh—nearly three times as much, as of June 2016, according to the U.S. Energy Information Administration’s (EIA’s) Electric Power Monthly data for June 2016 (Table 5.6.B). What’s more telling is that the gap between residential and C&I customers—on average nationwide—is increasing (Figure 1).

Size Provides Leverage

In 2015, sales of electricity to C&I end customers were 2,316,982 GWh, or 62.2% of the total 3,724,525 GWh. Residential sales accounted for 1,399,884 GWh, and the transportation sector made up the balance with 7,659 GWh, according to the EIA. Aside from the clout they have with utilities by virtue of their load (at 1,358,419 GWh, the commercial sector alone was just below the residential sales total in 2015), the size of C&I customers gives them other advantages residential customers lack. These include access to capital, a larger pool of technology options (including power or combined heat and power generation from fossil and renewable fuels as well as multiple storage technologies of varying scales), and a growing number of potential independent power producer (IPP) partners.

Those factors make it increasingly feasible for large customers to cut their ties with the local utility in order to source power that is both cheaper and cleaner. Although procuring “cheaper, greener” power is often the reason both residential and C&I customers decide to self-generate or purchase power from a non-utility provider, utilities work harder to keep and acquire the larger customer. We saw that most recently in New Mexico, where PNM moved rapidly to pave the way for new renewable supply in order to woo a proposed Facebook data center to the state (see “New Mexico Clears Hurdle to Provide Power to Facebook Facility”).

The indicators of this swelling trend seem to increase monthly. Several recent reports and corporate announcements have underscored the added clout C&I customers have thanks to improving economics of energy storage, for example. There is at least one event dedicated to the procurement of renewables by corporate buyers. And, in addition to entities that have long been involved in selling renewable energy credits to C&I buyers, there are also organizations devoted to helping large corporate customers source renewable power supplies, including Rocky Mountain Institute’s Business Renewables Center, which had 143 members representing 4,530 MW of deals as I was writing this column in early September.

Who Is Generating and Selling Power?

Over the past decade, utility and industrial generators have lost ground in terms of gigawatt-hours produced, while IPPs, as well as commercial and residential customer classes, have increased production (Table 1). Although year-over-year gains and losses varied between 2006 and 2015, since the global financial downturn of 2008–2009, only the commercial and residential sectors have shown generation gains each year. (The EIA didn’t include residential generation in its Electric Power Monthly report until 2015.) The changes are relatively small as a percentage of total generation, with utilities and IPPs together still accounting for 95% of generation in 2015, but the shift away from the utility as the primary power provider is likely to continue.

What’s more, in addition to the familiar categories of IPPs and self-generating customers, we now have new sorts of customers who can also sell power on the wholesale market. This summer, Apple gained approval from the Federal Energy Regulatory Commission to sell the power generated from three of its solar projects in excess of its own demand into regional markets. Google Energy gained similar rights in 2010. Some energy industry writers have characterized these moves as turning the tech companies into “utilities.” Although—at this stage—that’s a stretch, these big energy customers are clearly in competition with utilities.

Cost-Shifting Between Customer Classes?

While utilities in many states move against net metering by rolling back rates for customer-generated electricity or proposing higher fixed fees, one has to wonder if what they are really cushioning themselves for is the loss of C&I customers that can leave more easily than residential ones. Though proving intent for every utility would be challenging, the trend in retail prices noted above shows an interesting pattern that could lead one to think that the real cost-shifting is from C&I customers to residential customers—even though, historically, large energy users have argued that if they were to pay the same rate as residential users, they would be subsidizing residential customers.

Regardless of utility intent, it’s clear that large energy users are doing what they’ve always done: seeking ways to reduce their bills. How residential customers, their technology enablers, and regulators respond over time will be interesting to watch. ■

—Gail Reitenbach, PhD is POWER’s editor.