The flood of cheap Marcellus Shale gas driving massive construction of new natural gas power generation capacity could wreak havoc in the PJM power market, Moody’s Investors Service suggests in a new report.

Two of the nation’s largest power markets, Texas and California, already pose a “distressed environment” for unregulated power companies owing to declining market prices, the credit ratings agency said. Now, a glut of new gas generation in PJM—where new plants are expected to add up to 100 TWh, boosting gas power capacity 25%, by 2021—is poised to increase supply “amid little prospect of growth in demand,” it said.

The agency noted that PJM’s latest forecast report indicates load growth has declined over the last decade, with system load falling to 790 TWh in 2015 from 822 TWh in 2005. Peak demand has also fallen to 143 GW in 2015 from 154 GW in 2005. “Over the past few years PJM has also repeatedly cut its forecasts, and the grid operator currently projects weather-adjusted peak demand growth of only 0.2% per year over the next 10 years,” the report says.

Starting in 2021, on-peak prices could plummet by $7/MWh or $3.5/MWh on an around-the-clock basis, which represent declines of between 10% and 15%, the report forecasts.

The gas buildout will prompt more widespread coal plant closures or conversion to gas, it projects. “However, gas conversion is not a panacea for uneconomic coal plants, because the converted units will have poor fuel efficiency and operate as peaking units,” it adds.

The report projects that coal plants running at a 40% capacity factor will be forced to close. About 7 GW of coal capacity are at high risk, and may be forced to run at a 38% capacity factor, it suggests. Another 12 GW, running at a capacity factor of about 58%, would face a “medium” risk.

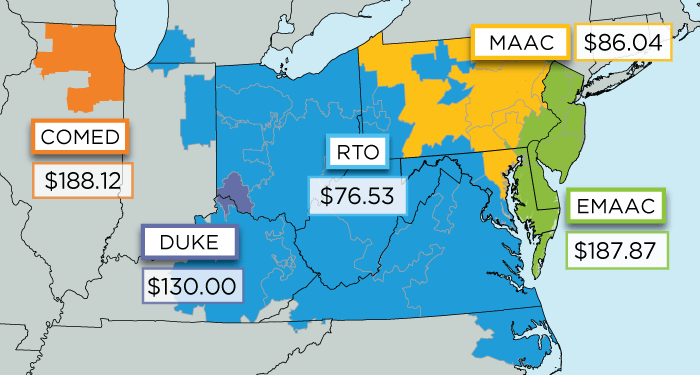

“Unlike inefficient gas plants, coal plants would have difficulties surviving on capacity payments alone because they have a much higher fixed cash cost to cover, commonly in the $70/kW-yr (or $218/MW-day at 88% availability) range or higher. Therefore, they have to run enough to make enough gross margin in the energy market to support their fixed expenditures,” it says.

Among corporate issuers with the most coal capacity in PJM are: Talen Energy Supply, FirstEnergy, GenOn, and Dynegy. The decline in power prices will also financially shake nuclear generators like Exelon and PSEG—as well as companies with gas plants.

Dynegy, Calpine Corp., and NRG Energy, are among a handful of merchant generators that are legally challenging recent measures by New York and Illinois to foster subsidies for nuclear plants economically stricken by low market prices amid the torrent of cheap gas. “If the challenges succeed, closure of uneconomic nuclear plant can support power prices and prospects for coal survival,” Moody’s said.

A number of power companies are already reducing debt to counter these “deteriorating market conditions,” Moody’s said. Exelon Generation has announced a $3 billion debt reduction plan. Calpine and Dynegy, companies with the most exposure to efficient gas plants, are also working to reduce debt.

Calpine wants to reduce its debt by $2.7 billion by the end of 2019, and Dynegy has committed to a debt reduction of between $1.5 billion and $2 billion (which may need to be accomplished through asset sales, the agency said, because the Houston-based company has a “limited amount of free cash flow available to pay down debt”).

—Sonal Patel is a POWER associate editor (@sonalcpatel, @POWERmagazine)