Pending Environmental Protection Agency regulations to slash U.S. power plant emissions likely will lead to the closure of nearly 18% of the nation’s coal-fired generation capacity, trim demand for steam coal by 15% to 31% and boost demand for natural gas by 8% to 16%, a new Credit Suisse analysis concludes.

While the Credit Suisse analysis agrees with similar assessments by Wall Street research firms that the EPA rules could hit the coal industry hard and boost market share for natural gas, it departs somewhat from those analyses by suggesting the rules over time likely will be beneficial for the utility industry because they will help shrink the current generation glut and thereby lead to higher power prices—and increased revenues—for power plant operators.

"We see EPA policy accelerating the tightening of market conditions and rebound in generation earnings in 4-5 years, making the recovery more ‘investible,’" Credit Suisse said.

The September 23 analysis addresses the utility sector impacts of separate regulations being finalized by EPA to reduce sulfur dioxide (SO2) and nitrogen dioxides (NOx) emissions across the eastern United States and to slash emissions of mercury and other hazardous air pollutants (HAP) nationwide.

Credit Suisse and other Wall Street research firms, industry experts and EPA officials broadly agree that the rules in combination will require all of the nation’s coal fleet to have SO2 scrubbers and other controls that can work in concert to reduce SO2, NOx, particulate matter, mercury and other HAPs.

While EPA contemplates requiring these controls to be in place by 2014 and 2015, Credit Suisse said it expects the agency will allow up to two additional years for compliance due to the sheer volume of new controls that will need to be installed.

The analysis concludes that the EPA rules will hit hardest a set of smaller, older plants for which the economics of installing expensive pollution controls cannot easily be justified. Credit Suisse looked primarily at plants with a capacity of 300 MW or less in its analysis.

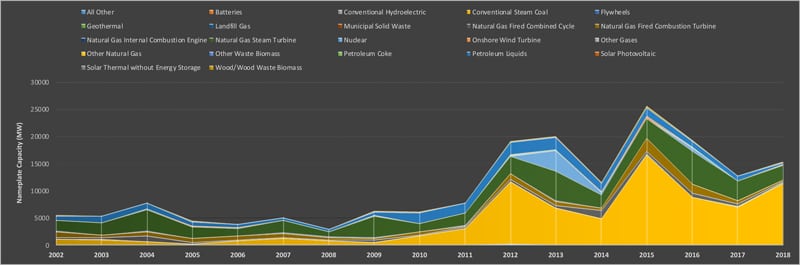

Within this fleet of small plants, some 50 GW of capacity are more than 40 years old and have no environmental controls, the analysis noted. If that subset is expanded to include plants that lack SO2 scrubbers, the fleet "at risk" grows to 69 GW, or 20% of the total 340 GW U.S. coal fleet, it said.

"When we think about the fleet at risk of retirement, we find comfort in a 60 GW closure baseline in large part from the small plants at risk with the realization some will survive but many plants over 300 MW will instead face closure for equally challenged economics," the analysis said.

At the same time they face the EPA rules, coal fleets also are contending with the steady decline of natural gas prices, caused in large part by astounding growth in shale gas production in many regions of the country. The resulting "crummy economics" for coal are so bad that plant owners would be well advised to consider closing their smaller, uncontrolled units even before turning to the equally vexing problem of raising capital for pollution controls, Credit Suisse said.

"If the EPA rules were not bad enough for coal generators, we think a large chunk of the U.S. coal fleet is vulnerable to closure simply due to crummy economics where we see coal pricing at a premium to natural gas out the forward curve when adjusting on an electricity-equivalent basis," the analysis said. "Awful energy margins suggest to us that owners should be re-evaluating their coal fleets due to pure energy economics before even taking on the burden of a [capital expense (capex)] for environmental control equipment."

Accordingly, Credit Suisse said it thinks "[plant] owners will be more motivated to close plants as they realize that the environmental capex obligations are unavoidable and the realized/projected energy margins are inadequate to justify running the plants (before they try to afford the capex). Clearly some game theory will exist for plants that are ‘on the bubble’ as owners wait for others to close, which should improve market pricing; but we see a realistically healthy chunk of the fleet ‘under the bubble.’"

In analyzing the rules’ impact on the coal and gas markets, Credit Suisse modeled two scenarios, one in which 60 GW of coal are retired and the other in which all 103 GW of plants lacking both scrubbers and selective catalytic reduction (NOx controls) are retired.

Coal demand would fall by 157 million tons annually, or 15%, under the first scenario, and by 324 million tons (31%) under the second scenario.

Natural gas demand would increase by 157 trillion cubic feet (TCF) or 7.8% in the first scenario, and grow by 3.7 TCF (16%) just from the coal retirements alone—before taking into account market share gains from future demand growth.

"Even more interesting to us, when we take into account natural gas needed to meet future power demand growth we could [see] another 1.2–2.5 TCF in seven years, bringing total natural gas demand from the power sector to 3.0 to 4.3 TCF under the 60 GW retirement scenario," Credit Suisse said.

Interestingly, Credit Suisse said the EPA rules will lead to tighter power markets and a faster return to "replacement cost" economics, changes it said would increase earnings by merchant generators—with some "outsized" winners.

"We could see broad-based opportunity for the power generators with enforcement of the EPA rules mostly through tightening power markets that will support higher energy and capacity prices (where available)," the analysis said. "The upside will come through both a shift to higher-cost plants setting the marginal price of electricity as well as a willingness to wait for the ‘right’ pricing signals before building new assets (most visibility with higher capacity prices), a situation that does not exist in the market today."

In summing up the investment implications of its analysis, Credit Suisse said "[t]he most significant mantra to take from this EPA analysis is to own cleaner generation in dirtier markets, where coal is more commonly on the margin and in turn vulnerable to closure.

"From our earnings estimate runs, we see the biggest [earnings per share] benefits coming in at [FirstEnergy and Allegheny Energy Inc.], Exelon Corp. and RRI Inc., while the most indifferent stocks to EPA policy include [NextEra Energy, Entergy Corp. and Public Service Enterprise Group.]

Equally interesting is that Credit Suisse concludes that the EPA rules also will bring growth opportunities to some—but not all—regulated utilities. Generally speaking, these benefits will flow from the likely need to build new generation to ensure system reliability in the wake of the anticipated closures of the older, smaller coal plants. The analysis projected that the EPA rules could boost regulated utility earnings per share by 1 to 4%.

Likely winners among regulated utilities—based on relatively low likely capex requirements due to the EPA rules and/or the potential to build new generation—are Allete Inc., Great Plains Energy Inc., Alliant Energy Corp., OGE Energy Corp., and Ameren Corp, the analysis said.

—Chris Holly is a reporter for The Energy Daily, where this first appeared.