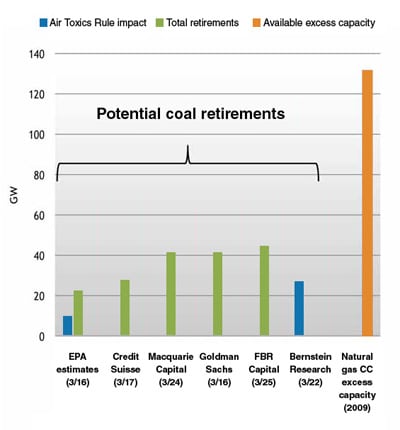

An update to a 2010 analysis on the market and regulatory outlook facing coal-fired power plants in the U.S. from economists at The Brattle Group forsees that 59 GW to 77 GW of coal plant capacity are likely to retire over the next five years—about 25 GW more than previously estimated—due primarily to lower expected natural gas prices.

The report titled “Potential Coal Plant Retirements: 2012 Update” notes that as of July 2012, about 30 GW (or 10% of total coal capacity) had already announced plans to retire by 2016. The report’s new estimates take into account how the decrease in spot and forward gas prices, combined with low demand for power, have reduced projected energy margins and costs of replacement power.

But it also analyzes the latest developments of two Environmental Protection Agency (EPA) rules—the Cross State Air Pollution Rule (CSAPR) and the Mercury Air Toxics Standards (MATS)—which it says have “less restrictive requirements on the compliance deadlines and equipment than previously predicted."

CSAPR was recently vacated by a federal court, but that ruling adds "an increased level of uncertainty regarding the timing and requirements under a potential future proposal by the EPA." The ruling may increase the role of the EPA’s existing Regional Haze Rule for coal-fired plants in the Eastern Interconnect, the report says.

It essentially considers two scenarios for required environmental control technologies that have an assumed compliance deadline of 2016: a "lenient" one that would warrant installation of selective noncatalytic reduction (SNCR) technology, and a "strict" one that would mandate installation of selective catalytic reduction (SCR) technology. "We find that 59 GW to 77 GW (for lenient versus strict scenarios, respectively) of coal plant capacity are likely to retire instead of retrofit with environmental equipment. These retirements occur absent any future regulations restricting carbon emissions," the report concludes.

The outlook bases its assumptions on a projection that natural gas forward prices at Henry Hub will reach $4.30/MMBtu (2012 dollars) by 2016. Retirement projections are "very sensitive to future market conditions," the report notes, concluding that if there were a $1/MMBtu increase in gas prices, the group’s range of projected retirements would drop 21 GW to 35 GW. If natural gas prices instead dropped by $1/MMBtu, the range of retirements would increase to 115 GW to 141 GW.

"Note that this very substantial level of retirements corresponds to 36-45% of the existing coal fleet, enough to likely cause reliability issues if not countered by rapid development of replacement power (or by supplemental capacity revenues of some kind to sustain more of these coal plants)," it cautions.

Scenarios analyzing strict versus lenient environmental rules only change the group’s projection range by about 18 GW (59 GW in the lenient case versus 77 GW in the strict case that requires more SCRs). "Thus, gas prices are a much more significant influence on retirements than the stringency of the remaining regulations," the report says, though it points out that a $30/ton carbon dioxide price starting in 2020 could cause base projected retirements to surge to 127 GW to 149 GW.

Environmental regulations would affect regional supply curves enough to prompt an increase in wholesale spot prices "by a few dollars, for a few years," the analysis reveals, likely a $5/MWh price spike starting in 2015.

It also suggests that most coal-fired retirements (80% or more) would be from regulated units. Capital expenditures to install environmental control equipment and build new generation capacity to replace retiring units owned by non-merchant entities, meanwhile, will run between $126 billion and $144 billion, with little change compared to changes in retirements reflecting prices of gas, power, and carbon dioxide.

"This relatively robust result is due to similarity of capital costs between new gas plants and multiple retrofits. For example, a small coal plant (200 MW) would need to spend about $1,000/kW to install a dry [flue gas desulfurization] and a baghouse if it is retrofitted, while retiring and replacing the plant with a new gas [combined cycle plant] would entail approximately the same capital expenditure," the report explains. "As a consequence, lower coal plant margins result in more gas plant replacements, at roughly the same cost as the avoided retrofits."

Perhaps the biggest impact from changing market and regulatory conditions will be felt by smaller generation companies or utilities with predominantly coal-fired generation, the report finds. “Our analysis indicates that future coal retirements will be a bit more than double the level announced to date,” said Frank Graves, Brattle principal and co-author of the study. “The impacts will be modest over large areas, but more acute locally, especially for owners of smaller fleets that are predominantly coal-based."

For example, an estimated 4% of coal plant owners (which operate about 20 GW of total U.S. capacity) would need to retire more than 50% of their generation under the base case. "However, once industry-wide compliance adjustments are made, the coal fleet should be as profitable as it would have been absent the environmental rules," the groups says.

Sources: POWERnews, The Brattle Group

—Sonal Patel, Senior Writer (@POWERmagazine)