POWER Associate Editor Sonal Patel reported on Sept. 12 that “nearly 100 renewable energy and environmental groups and businesses have asked the Energy Information Administration (EIA) to reevaluate renewable energy forecasts, alleging the agency’s projections don’t reflect ‘the current status and recent, real-world growth rates of renewables.’” The EIA forecasts are presented in its Annual Energy Outlook. The groups seek to have the EIA increase its projections because they are “unreasonably low and have not been borne out by actual experience.” Concrete suggestions about how the EIA might do so were not forthcoming.

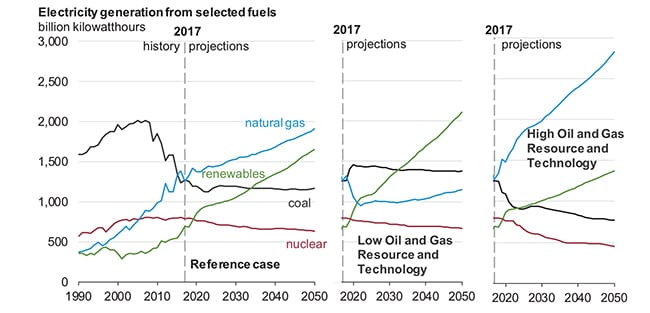

The groups’ ire is misplaced and shows a woeful ignorance about the purpose and work of the EIA. The EIA develops a “Reference Case” for its National Energy Modeling System for its AEO that is based on current laws and regulations by assuming that existing laws and regulations remain unchanged throughout the projection period, unless the legislation establishing them sets a sunset date or specifies how they will change.” In other words, the EIA folds into its projections the impact of existing national and state laws as they are now, not how a group or groups would like the laws to be in the future. Perhaps the best example is the American Taxpayer Relief Act of 2012 (ATRA) passed by Congress on January 1, 2013 that renewed the Production Tax Credit for wind for another three years and included projects cryptically categorized as “under construction.” Therefore, the EIA computer models only analyze the impact of the PTC for the statutory three years and not further into the future. The EIA then runs a series of other cases to determine the sensitivity of changes in law, fuel prices, and so on. This has been the Administration’s approach to energy modeling since the first Annual Energy Outlook was released in 1979.

Now it’s my turn to suggest two reasons why the EIA analyses and projections regarding the growth of renewables are too ambition and should be corrected downward. First, the EIA analyses assume the enforceable Renewable Portfolio Standards now set by 30 states are fully met in capacity, generation, and timing. In a conversation with EIA Deputy Administrator Howard Gruenspecht (then-Acting-Administrator) at the Electric Power Conference in May 2012, Gruenspecht confirmed those were the ground rules for the AEO, because to do otherwise was politically unwise. Many states have failed to meet their RPS goals and at least “16 states with renewable portfolio standards are considering legislation that would reduce the need for wind and solar power,” according to a report by RenewableEnergyWorld.com. My proposal is when any state RPS renewable growth goals are missed, the AEO models should be updated to reflect true progress, rather than merely expectations.

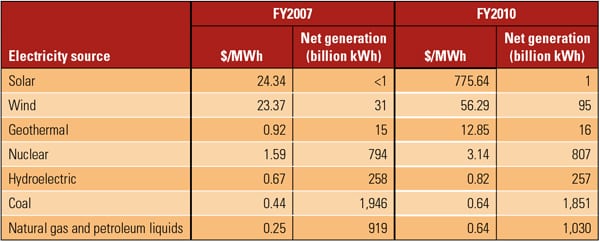

My second recommendation pertains to the plant cost estimates used by the EIA in its predictive models. The “overnight costs” of a variety of power generation alternatives are listed in the report’s Table 2.5-Technology Performance Specifications along with capacity, nominal heat rate as well as capital and annualized O&M costs. All this data feeds directly into the EIA models. However, hidden in notes in previous AEO reports, but not included in the current report, is a critical assumption: capital costs and O&M costs are based on an assumed 30-year plant equipment life.

On what basis does the EIA assume that all currently installed and future wind turbine will operate (or are capable of operating) continuously for 30 years? The industry experience appears to be perhaps 10 years, maybe 15 years maximum before it is “repowered” with a later technology. The EIA should update its economic analysis to include the cost of a turbine replacement at the end of 15 years to accurately portray the technologies true life cycle cost. I don’t know what this rational assumption means but I suspect it would play havoc with the results of EIA projections for wind energy in the future.

I pointed out this exception in the EIA analysis to Gruenspecht during that same discussion and he agreed that it was a weakness in the AEO analysis. But it wasn’t changed in the 2013 release a year later as far as I can tell–in fact, the capital cost of wind equipment was reduced 19% from 2012. I don’t know what the impact of this change would have on the AEO projections but I suspect it would be significant, and probably politically untenable. But it would be the right thing to do because national and state policies are made based on the results of this report.

As noted on page 21-3 of the report, “Based on recent experience, most WN [wind] operators do not treat O&M on a variable basis, and consequently, all of the O&M expenses are shown below on a fixed basis.” Let me translate that statement: Wind power developers, almost without exception, are required to purchase a long-term service agreement (LTSA) from the turbine supplier in order to obtain bank financing. Banks are adverse to O&M cost risk when loaning money. Many of those LTSAs are for 7-15 years, which means reported O&M costs (which are usually considered propriety information and seldom revealed, many owners don’t know the real numbers either) are not the true O&M costs incurred by the supplier or owner. The anecdotal O&M cost data that is publicly available shows O&M costs often exceed pro forma estimates but actual field data is tough to get our hands on for a thorough analysis.

As a side note, the IGCC cost estimate in the plant cost estimate report is $4,400/kW (Oct. 1, 2012 $) for a 600 MW plant, the size of Duke Energy’s Edwardsport IGCC plant. Edwardsport happens to be a 600 MW plant that went commercial mid-2013 and is projected to cost ~$3.5 billion or ~$5,800/kW. In other words, the cost of Edwardsport is a third higher than the estimate used in the AEO models. This observation raises more questions than it answers.

–Dr. Robert Peltier, PE, consulting editor