Lawrence J. Makovich, PhD, IHS CERA’s vice president and senior advisor for Global Power, predicts a rebound in electricity consumption from recession levels. Specifically, the rebound will be stronger than government projections, led by growth in electricity use by industry.

The U.S. Energy Information Administration’s (EIA) Annual Energy Outlook 2013 (released Dec. 5, 2012) predicted industrial electricity sales increases by 1.4% and 1.2% in 2013 and 2014, respectively. Contributing Editor Mark Axford met with Lawrence Makovich, PhD, an authority on electricity markets, regulation, economics, and strategy during the March CERA conference. Makovich candidly presents his view of the EIA demand growth predictions, the competitive electricity market, and renewable power generation.

I was interested in your comments about the coming industrial renaissance in the U.S. How did you come to the conclusion that U.S. demand will grow more rapidly than the latest forecast from the EIA?

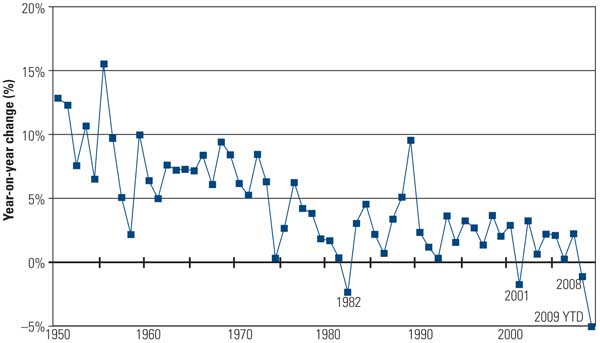

Makovich: If you look back at the trend rate of growth of power, EIA is telling the nation to expect something under 1.0%—I think they’re at 0.9% per year as a trend growth rate. That’s a significant slowdown from what we’ve seen historically. A lot of people have asked me, “What’s behind that?” If you pull the numbers apart, there’s a very interesting story to be seen.

If we look back across the past decade, for example, we saw residential use of electricity grew 1.7% per year. Commercial electricity growth was 1.0% per year, yet industrial consumption was down 0.2% per year. If you dig into the data further, you’ll see that in the last economic expansion, prior to the recession of 2002–2007, residential demand was running up 1.9%, commercial was up a little over 2%, and industrial was going at 0.7% positive. If you looked at industrial production, of which manufacturing is about 80%, industrial production was moving up at about the same pace as the U.S. economy, about 2.4% per year.

What this data tells us is that over the last economic expansion, we had about a 2% or so gain every year in electric efficiency on the industrial side, and that’s something we expect to continue. Now, when we look at the recession, industrial production dropped 20%. The broader economy (GDP) dropped 5% during a year and half, 2008 through mid-2009. So industrial activity and manufacturing activity took a big hit.

Today, we see the U.S. moving into a favorable competitive position particularly because of the low cost of energy now available to manufacturers. Our expectation is that manufacturing and industry in the U.S. will be growing a few points more than GDP. So even if we get 1.5% to 2.0% efficiency gain every year, we’re looking at a much stronger story for industrial power demand over the next five years.

So, if the industrial power usage firms up and grows 1% to 2% per year, and there are similar trends as in commercial and residential energy use increase, I think we’re going to end up much closer to what we’ve seen in the past: an overall growth rate in electricity consumption of 1.5% to 1.7% per year. The current estimates today from EIA and the general pessimism about the economy suggests this is a no-growth business. I think people have confused some cyclical events as permanent structural changes.

Do you think the U.S. will start to feel any of that electricity consumption increase during 2013, or is it going to take a little while longer?

Makovich: The Wall Street Journal began 2013 with an article titled “Power Demand on Wane” (Rebecca Smith, Jan. 2, 2013). The article didn’t correct for weather or the business cycle. It gave people the impression that the drop in consumption has been caused by a broad efficiency effect.

I had the feeling that when the CERAWeek conference began on March 4, the year-to-date power consumption was probably going to surprise people. As of Feb. 28, 2013, electric consumption in the U.S. was up a little over 2%. Now, that was easy to predict because we know that 2012 was the warmest year in 100 years. So the probability that this winter would be as warm as last winter was very low. We also knew that we’d have a positive push from a colder Jan.-Feb. Layer on top of that an economy that is at least 2% larger than it was in 2012, and that gives us two reinforcing factors: more economic activity and a weather correction that is a positive push.

I knew we’d get off to a stronger start in 2013. So we’re above trend, probably even ahead of the GDP growth rate for the first quarter. We expect that summer 2013 won’t be as warm as 2012, so the growth rate will probably taper off during the summer, but we’re still looking at growth in electricity consumption that could be as great as 1.6% for 2013 over 2012.

When I think of industrial manufacturing in America, the places that come to my mind are Ohio, Indiana, and, in a different way, Texas and the Gulf Coast. Will regional demand growth be different in those regions than in the Northeast and California?

Makovich: Electricity is one of a number of important inputs to industrial processes. When you look at the energy input to industry, electricity has been gaining share globally. Industrial electricity use accounts for, on average, 25% to 33% of industrial overall energy consumption. When you think of the trends in automation, robotics, and computer control of industrial process, you can see why electricity is gaining share as an energy input. Places that have relatively low power prices, all else equal, become more attractive to the expansion of manufacturing.

What’s interesting is within the U.S., across the last decade, the spread in industrial power prices from one state to another has expanded quite a bit. Ten years ago, the average distance to the mean for industrial power prices was 2.4¢/kWh. Today it is 3.8¢/kWh. California is an example of a state where power has become relatively expensive. A couple days ago, the Wall Street Journal noted that high labor costs and high energy costs are causing a decline in California manufacturing jobs, even though the U.S. has added 500,000 manufacturing jobs over the past two years.

Power prices are also an important factor for global competitiveness. When you look at our five major trading partners, the U.S. has a competitive advantage in power price. Take Germany for example. In the past decade, the industrial price of electricity has gone up 10 times faster than in the U.S. German industrial electricity prices are more than double the U.S. prices. In addition, the price of natural gas in Germany is about triple the average U.S. cost. Energy prices definitely affect global competitiveness for industry. Energy prices are influencing where manufacturing activity is going these days.

How about the market structure debate? PJM is saying that capacity payments are fundamental to success. ERCOT is saying no, energy only is the best approach. What is your opinion?

Makovich: When California first put together its deregulation of the power sector, CERA had written that there didn’t seem to be an adequate mechanism to recover the full cost of generating capacity. We predicted that there would be boom and bust cycles, and as it played out, that’s exactly what happened. California didn’t have a market structure that supported investment, and they ended up short of power.

I’ve written that the root cause of the problem was a flawed market structure. I testified in Congress that capacity mechanisms are needed for a well-functioning power market. We’ve known for a long time that well-structured power markets need some type of a capacity payment. I think the general trend has been a slow evolution to capacity payment mechanisms. PJM is on its third or fourth major revision. ERCOT started with a capacity requirement. When ERCOT built a lot of new capacity, the capacity payment was suspended. Now ERCOT is running short of power again, and the necessity of a capacity mechanism is becoming apparent. There are a number of interesting proposals about how to structure this mechanism, but without getting into the particulars, CERA thinks a well-structured power market needs a capacity mechanism.

California was once a leader in developing competitive markets 12 years ago, before the deregulation train wreck. Now, after a decade of re-regulation, will the community aggregation movement create traction for more competition?

Makovich: These efforts are very preliminary. At the root of the problem is the high cost of power. California has some of the highest power prices in the country, significantly above the U.S. average. What’s interesting is that residential use per household over the last decade has gone up, not down. Most people don’t realize that in 41 out of 50 states, residential use of electricity per household has gone up. This occurred despite the fact that the real price of electricity went up 10% on average in the U.S. and average personal incomes went down 6.7% during that same decade. What people pay for electricity, their bill, as a percentage of their disposable income has been going up. That creates more and more pressure to find some relief. And I think that’s exactly what you are seeing in California. People have this hope by moving toward a muni or community aggregator they can achieve some price relief.

With the experts predicting low and stable natural gas prices for years ahead, is the U.S. now seeing a flattening or the beginning of a decline in the appeal of green energy?

Makovich: It’s a very interesting phenomenon. The original production tax credit legislation was put in place for just seven or eight years. I’ve always asked, “Why seven or eight years and then expire?” That’s about the amount of time it took us to put a man on the moon after President Kennedy made the commitment. I think the logic was, if we can put a man on the moon, we ought to able to encourage enough activity in wind and solar so that within eight years or so, we would have moved up the learning curve, driven costs down, and achieved sufficient innovation so that the reduced cost would have created a widespread disruptive technology. It didn’t happen.

The reason it didn’t happen was that the biggest innovation that we’ve had in energy, maybe in our lifetime, was the shale gas revolution. It wasn’t an innovation that people really wanted. A long time ago, the government took away its support for this kind of fossil development. Nonetheless, it happened. People were slow to recognize what was occurring, but the notion that innovation would deliver more abundant, lower-cost fossil fuels was not what people expected. Instead, people were told for years that fossil fuels were the fuels of the past. So the innovation that people didn’t want, or expect, has substantially undermined the economics of renewables.

The cost gap between renewables and conventional fuels is as big today as it was 10 years ago. You can see it very dramatically in the stock prices for clean energy companies. They soared when people thought this was the disruptive technology of the future, they dropped with the rest of the market in the recession, and did not recover when the stock market reached an all-time high. I think this has occurred because today’s investment hypothesis is renewable energy is no longer a disruptive technology ready to take off. Instead, the investment hypothesis says that without long-term government support, you’re not going to see growth in renewables.

I think that’s what we’ve got ahead for us right now—a renewables business that’s going to depend for many years to come on continued government support.

The Regional Greenhouse Gas Initiative in the Northeast was the first U.S. carbon market, recently followed by California. Do you think this will spread to other regions of the U.S.?

Makovich: I think the success of these markets to date is rather mixed. In Europe, there were lots of problems with the way the market was set up. Prices initially were much higher than people expected, then much lower, and there were some concerns about fraud in the marketplace. I think the biggest lesson here is that these markets, if set up properly, are a very effective way to put a price on CO2 emissions.

The problem is when some regions do it and others don’t. California and Europe put a price on carbon with a very well-intentioned effort to internalize these costs, while the rest of the world, in particular China, is expanding its power sector largely based on coal-fired generation. Despite all the efforts in the developed countries, CO2 emissions globally are over 50% higher than they were in 1990.

I think the lesson here is that unless you get all the major emitters to participate, taking action unilaterally puts you at a competitive disadvantage. Some people say that every little bit helps, but unilateral efforts have not materially affected the trends of CO2 emissions and the absolute level of concentrations in the atmosphere.

CERA focuses on the question, “What would it cost to transition to emit lower amounts of carbon for the energy that’s used?” There are some huge gaps in the application of good engineering, economics, and science. I think people are doing a lot of things today that don’t make sense from an economic and science perspective, a lot of inefficient activities to address CO2.

For example, Germany is a leading proponent of solar photovoltaic for people’s rooftops. The problem is, Germany isn’t a sunny place. It’s a relatively inefficient application of resources to a technology that does not give you much bang for the buck. The implicit cost is probably over $100/ton of CO2 removed with PV panels in Germany. You could get a 10-fold reduction in CO2 simply by purchasing the allowances on the marketplace because other people have cheaper options to reduce CO2.

The ironic thing is that as the Germans learn the limits of intermittent renewables, they’re being forced back toward conventional power plants. Today, Germany is building more coal-fired power plants than the U.S., a power grid with six times the capacity.

—Mark Axford, POWER contributing editor, conducted and edited this interview.