Inflation-busting retail electricity price rises are doing little to encourage the power plant investment Britain needs to keep the lights on. Offshore wind projects are stumbling as technical and financial risks bite, a carbon tax has failed to achieve its aims, and the European Union is threatening to ban the financial support mechanism that seems to be the only hope of attracting new nuclear capacity.

After years of dithering on energy policy, the UK government has nearly finalized its plans for electricity market reform. Guaranteed prices for low-carbon power, plus a carbon floor price to discourage the use of coal, are the pillars of an Energy Bill published at the end of last year.

The UK faces a capacity shortfall as old coal and nuclear plants are retired. It also needs to stay on track with a binding commitment to cut greenhouse gas emissions by 20% by 2020—to be followed up by a 40% cut by 2030 under European Commission (Commission) plans announced in January. The UK has come round to supporting the Commission’s new target of 27% renewable energy by 2030, though this will not translate into national law.

But despite its subsidies, the Energy Bill is not a magic wand. By offering double the current wholesale price, with contracts to last 35 years, the Department of Energy and Climate Change (DECC) has persuaded three consortia to agree to build much-needed new nuclear capacity. Even without further project slippage, however, none of this will be online before 2023. Meanwhile, several gigawatts of planned offshore wind capacity have been canceled as developers face up to narrow margins and technical challenges.

The Commission is also looking hard at energy subsidy mechanisms across Europe, and seems set to come down hard on the UK’s first new nuclear plant. The UK funding scheme was drawn up with European Union (EU) competition policy in mind, so all will probably come right in the end, but there may be long delays.

Power Prices, Fuel Poverty, and GDP

For more than a year, energy prices have rarely been out of the news.

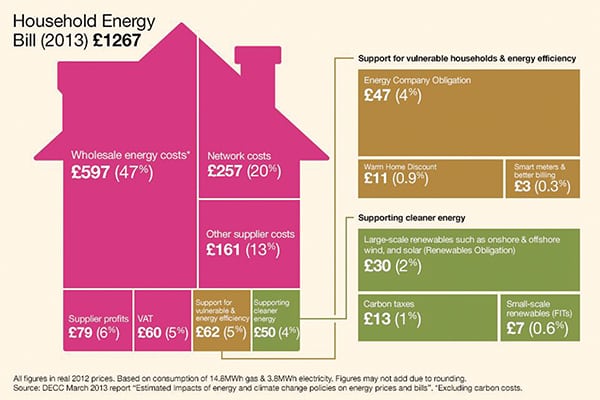

According to the Office for National Statistics (ONS), inflation-adjusted household spending on energy has risen by 55% in a decade, even as energy use fell by 17%. Electricity, gas, and other household fuels cost a typical household £106 (US$176) per month in 2012, up from £69 per month in 2002, the ONS said (Figure 1).

|

| 1. Where the money goes. All figures in this breakout of components of the typical 2013 UK household energy bill use real 2012 prices. The chart is based on consumption of 14.8 MWh [equivalent] gas (50.5 million Btu) and 3.8 MWh electricity. Figures may not add up due to rounding. The wholesale energy costs exclude carbon costs. Source: Department of Energy and Climate Change |

Tom Lyon of price comparison website uSwitch.com said that consumers are having to ration their energy use, with more than a third saying that the need to cut back on heating has affected their quality of life or health.

Unprecedented flooding over the winter has popularized the idea, even in the right-wing press, that climate change is a real threat. With flood cleanup costs reported at up to £1 billion, more people are coming to believe that it is worth spending money on renewables. Yet when they receive their energy bills, many squeezed householders and business owners complain about the impact of green levies, believing that these are largely responsible for the price rises.

In fact, the ONS figures show that most of the cost increases in the last decade occurred between 2004 and 2009. According to the DECC, green levies in 2013 accounted for 4% of a typical household energy bill, with support for vulnerable households and energy efficiency schemes adding a further 5%.

Energy Secretary Ed Davey has accused utility companies of making excessive profits, and called on independent energy regulator Ofgem to consider breaking up the large utilities. The “big six” firms claim that the UK has a thriving and competitive power market.

Wind Is Key to a Low-Carbon Future

The UK’s northerly location, exposed coastline, and large tidal range make wind and marine sources the obvious choices for large-scale renewable energy.

With wave and tidal power going nowhere at the moment, wind is the key. The potential is huge: The UK’s total practical offshore wind resource has been estimated at 120 GW, more than twice the nation’s peak demand of 50 GW to 60 GW.

Current UK installed wind capacity is 7.1 GW onshore and 3.7 GW offshore, and in December 2013 wind supplied a record 10% of UK power demand.

Onshore, the year to June 2013 saw 1.3 GW of new wind capacity added. This growth must top out soon, however. Many prime sites in Scotland, Wales, and northern England are now taken, and developers are finding it harder to gain planning approval in the midlands and south of England, where wind speeds are lower and political opposition is stronger.

With a high density of civilian and military aircraft in UK skies, potential interference to air traffic control radar seriously restricts the siting of wind turbines. A technical modification to Raytheon radar systems announced in February could eventually unlock a further 2.2 GW of onshore wind capacity, said trade body RenewableUK.

In 2012, the Electricity Networks Strategy Group (ENSG), which sets out the views of the DECC and the grid operators, estimated 11.2 GW of onshore wind capacity by 2020.

Offshore Wind Ambitions Falter

Offshore wind, on the other hand, until very recently seemed to be getting into its stride again after the global financial crisis, which triggered a slump lasting into 2012. The 12 months to June 2013 saw 1.5 GW added—a growth rate that overtook onshore wind for the first time. In 2012, ENSG estimated 16.6 GW of offshore wind capacity by 2020, and last November, Energy Secretary Davey confirmed a plan for up to 39 GW by 2030.

Since then, things have again looked less rosy. As they gain offshore experience, developers have come to appreciate the challenges and risks of placing turbines far from shore and in water more than 25 meters deep. The need to protect marine wildlife, including rare sharks and birds, has also affected several projects. As a result, developers have withdrawn from more than 5 GW of planned capacity since November 2013.

The abandoned and down-scaled projects (Figure 2) include the Argyll Array (Iberdrola subsidiary ScottishPower Renewables), Atlantic Array (RWE npower), London Array 2 (DONG Energy, E.ON UK Renewables, and Masdar), and Dogger Bank Zone (Forewind, composed of RWE, SSE, Statkraft, and Statoil).

|

| 2. London Array. The 630-MW London Array offshore wind farm Phase 1, the world’s largest, went online in April 2013. Plans for Phase 2 were cancelled in February 2014 in the face of environmental uncertainties. Courtesy: Siemens |

The UK’s largest generator of renewable electricity, SSE, said in January that it would carry out a wide-ranging review of its offshore wind plans. Prospects for investment in generation assets in Great Britain are not encouraging, the firm said, and its investment after 2015 would be lower than in previous years.

With such a pessimistic outlook from the energy companies, the DECC now admits that the 2020 offshore wind total could be as low as 8 GW, with “up to” 41 GW by 2030. The department says it is still committed to keeping the UK a leader in this sector, but cost could be the killer as concern over energy prices mounts.

Industry heads agree that offshore wind costs must fall, but the question is how far and how fast. At the moment, offshore wind producers are guaranteed a price of £155/MWh, falling to £140/MWh by 2018–19. The latter figure is one that the industry can probably live with, and is actually higher than the £135/MWh expected last year in the run-up to the government’s new Energy Bill. Beyond that, however, the savings must accelerate: The DECC says it wants to reach £100/MWh by 2020.

Benj Sykes, director of wind power in the UK for Danish generator DONG, was widely reported when he said in March 2013 that he expected projects approved in 2020 to be down to €100/MWh (£84 or $139/MWh). DONG’s average offshore wind cost in 2012 was €160/MWh (£134 or $222/MWh), Sykes said.

Other offshore industry bosses and analysts have commented that the £100/MWh figure will be hard to meet by 2020. It is not yet clear what will happen to UK offshore wind if costs remain above this level, but given the critical importance of wind in meeting carbon targets, and the current slowdown even at £155/MWh, the signs do not look good.

Solar Mini-Boom

Despite often-cloudy skies, the UK is seeing a mini-boom in solar photovoltaics (PV). Until the last couple of years PV was the rooftop preserve of middle-class householders attracted by a residential feed-in tariff of 14.9 pence/kWh ($0.25/kWh). More recently, around 250 sites on farms and disused World War II airfields have sprouted PV plants of up to 33 MW, with 50-MW projects in the pipeline.

Current installed PV capacity is now approaching 4 GW, and in October 2013 the DECC forecast 10 GW by 2020. Energy Minister Greg Barker said he believed this figure to be too low: “I think that up to 20 GW of deployed solar is achievable within a decade.”

Barker may be overoptimistic. Much of this new solar capacity would be built in the Conservative heartland of southern England, which has more sunshine and higher property prices than the north of England, Wales, or Scotland. Many rural voters are now showing that they object to commercial-scale solar power almost as much as to wind turbines.

Even 20 GW of solar plants would provide just 2 GW of actual generation at the 10% capacity factor typical of UK latitudes.

Nuclear Renaissance at Last

The UK currently has 9 GW of nuclear generating capacity from 16 reactors at nine sites. Together they provide about one-sixth of the nation’s power.

All but one of these reactors (Sizewell B) are slated to close in the next decade as they reach the end of their lives. (See “UK Uses ‘Lead and Learn’ Strategy for Magnox Reactor Fleet Decommissioning” in the April 2014 issue.) To meet its carbon reduction emissions target, the UK will need to replace all this lost capacity; the 2012 ENSG report assumed 12.3 GW of nuclear power in 2020.

Finding commercial partners for such a large program has been challenging, but the future now looks promising. Up to 15 GW of new capacity looks reasonably secure in the hands of three different consortia.

Furthest along is a reactor to be built by EDF, with Chinese backing, at the existing Hinkley Point nuclear site on England’s west coast. If all goes well, the 1,650-MW EPR reactor will be followed by three more: a second Hinkley Point reactor plus two at Sizewell, another existing nuclear site. British utility company Centrica dropped out of the Hinkley Point project last year.

In May 2012, German utilities RWE and E.ON announced that their Horizon Nuclear Power group would abandon its plan to build new reactors at two existing sites: Wylfa and Oldbury. By November 2012, however, Horizon had been acquired by Hitachi, which now plans to build two 1,300-MW Advanced Boiling Water Reactors at each of the two sites.

The third consortium, NuGen, wants to build two or three reactors near Sellafield—Britain’s oldest nuclear site, though it has not had a power reactor for many years.

NuGen began as a joint venture between GDF Suez, Iberdrola, and SSE. SSE left the consortium in 2011. In December 2013, Toshiba said it would buy out Iberdrola, leaving it with 60% of the consortium and GDF Suez with the remaining 40%.

NuGen, which originally described itself as technology-neutral, had by 2013 narrowed its reactor choices to either AREVA’s EPR (2 x 1,650 MW) or the Westinghouse AP1000 (3 x 1,100 MW). Toshiba’s ownership of Westinghouse has settled the matter, and the first of the three AP1000 reactors is scheduled to come on stream in 2024.

Nuclear’s High Cost

Getting this far was a struggle. The government’s current Energy Bill, introduced to Parliament last November and currently before the House of Lords, has essentially the sole purpose of getting new nuclear and renewable capacity built by guaranteeing minimum prices for producers.

The price-setting mechanism, known as “Contracts for Difference” (CfD), sets out a “strike price” for each generating technology. Producers will receive the strike price for as long as this remains above the wholesale price.

In the case of nuclear it took a strike price of £92.50/MWh—around twice the wholesale power price—to get EDF to agree to go ahead with the £16 billion Hinkley Point C project. The other nuclear consortia were not involved in the detailed negotiations, so the need for a timely agreement gave EDF an effective monopoly. (If Sizewell C goes ahead, the strike price will fall to £89.50/MWh.)

Nuclear has broad support across the UK political spectrum, and the Labour Party has said that if it wins power next year, it will honor the agreement with EDF. Many of those on the left still distrust nuclear on grounds of safety and cost but believe it is essential to meet carbon emissions targets for the next few decades. Most Conservatives believe nuclear is cheaper and more acceptable than wind.

Brussels Strikes Back

In the run-up to the Energy Bill, Energy Secretary Davey said he would not sign any nuclear deal unless it was affordable, gave value for money, and met the coalition government’s promise that there should be no public subsidy. Yet critics believe the high strike price (which will soon be above that paid for onshore wind), plus loan guarantees and liability insurance provided by the government, looks very much like a subsidy. What’s more, the strike price is guaranteed for 35 years.

Last October, EDF said it expected to take the final investment decision by July, subject to final negotiations with the British government and agreement from the Commission on rules about state aid.

Yet the Commission seems to agree that there is something fishy about the Hinkley Point contract, and an initial report published in January suggests that the approval process will not be an easy ride. “It is not clear to the Commission that nuclear technology is immature enough to warrant state aid,” the report says, pointing out that the total subsidy of £5 billion to £18 billion could be more than the cost of the plant.

Dogged by delays to its EPR project at Flamanville in France, EDF is still maintaining publicly that Hinkley Point C can start up in 2023. It seems unlikely, however, that the Commission will deliver its ruling before the autumn, and the process could take as much as two years—given European Parliament elections in May, a five-yearly reshuffle of the Commission in October, and a UK general election in 2015.

Carbon Price Floor Widely Reviled

Charging companies to emit carbon dioxide—either as a direct tax or by allocating a limited number of tradable certificates—is widely seen as key to shifting generation from high-carbon to low-carbon sources.

The EU’s pioneering emissions trading scheme (ETS) has failed in this respect. Though the EU ETS carbon price has peaked at £25/metric ton (t) CO2, which should be enough to promote low-carbon investment, it is generally much lower—down to around £4/t CO2 currently. A reform of the scheme is overdue, but to date has proved difficult.

So as part of its electricity market reform, in April 2013 the UK government introduced a “carbon price floor.” This is currently set at £16/t CO2, rising to £25/t CO2 in 2017 and £30/t CO2 by 2020. UK companies must pay to the Treasury the difference between this price floor and the EU ETS price.

In its first year the “carbon tax” raised almost £1 billion, and by 2015/16 it will be adding £30 to £60 to the average annual household electricity bill.

The carbon tax is widely unpopular. Power generators and fuel suppliers say it needlessly increases costs to consumers, encourages coal-fired generation to migrate from the UK to the rest of Europe, and destabilizes the investment climate because the tax could be changed or scrapped at any time. Green campaigners believe it is ineffective, with the money disappearing into government coffers rather than being used to support renewable energy directly. Consumer champions and fuel poverty campaigners hate the carbon tax because it hits poor people hardest.

In response to criticism over rising household fuel bills, the government recently carried out a detailed review of its various “green levies.” Although the carbon tax has so far survived this scrutiny, in his budget of March 19, Chancellor George Osborne announced that he will freeze it for one year. By 2015 the carbon price will have risen to £18/t CO2 and this level will remain through 2016.

From Coal to Biomass

In 2012, the UK saw a marked rise in coal use for power generation, as low international coal prices and collapsing EU ETS carbon permit prices prompted generators to switch from gas. DECC figures show that in 2011 the UK got 30% of its power from coal and 40% from gas. In 2012 these figures were effectively reversed. Including other industrial and household use, UK coal consumption climbed by a quarter over 2011, and CO2 emissions rose by about 4%, after years of steady falls.

Final figures for 2013 are unlikely to be much different when they are published later this year, though the DECC’s preliminary data for the third quarter of 2013 shows coal down to 33% and gas down to 27%. A generation mix containing 40% coal is not sustainable in the long term, given that it implies about 18 GW of production from coal; now that the shutdown of the UK’s oldest and dirtiest coal-fired plants under the EU Large Combustion Plant Directive is almost complete, the UK has only about 20 GW of coal capacity.

Under new emissions performance standards introduced in the Energy Bill, any new coal plant would have to use carbon capture and storage (CCS), as in the U.S. under new Environmental Protection Agency regulations. Since that is unlikely any time soon, demand growth in the next few years will require a shift back to gas, if it cannot be met by an expansion of wind.

Converting coal-fired plants to burn biomass gives power companies a guaranteed price of £105/MWh as well as avoiding the carbon tax. This is a good deal, given that dedicated biomass power plants get £120/MWh.

Not all conversion projects gain government approval, however. In December, the DECC said it would not approve funding for Eggborough power station, which planned to convert one of its four 500-MW units to biomass.

The UK’s largest power plant, Drax, has fared better (Figure 3). In 2012, Drax Power canceled plans for a dedicated 290-MW biomass plant, but it still wants to become a predominantly biomass-fueled generator. The plant has six 660-MW generating units for a nominal capacity of 4 GW and supplies around 7% of the UK’s electricity.

|

| 3. Fuel shifting. The six-unit Drax Power Station converted one unit to biomass in 2013 and plans to convert two more in 2015. Starting in May 2014, one of those units will cofire 85% biomass with 15% coal. Courtesy: Drax Power |

Drax converted one unit to biomass last year. Two further conversions are planned for 2015; in advance of the conversion, one of these units will cofire biomass from May 2014. (For more on cofiring, see “Utility Coal-Biomass Cofiring: Turning Over a New Leaf?” in this issue.) The plans won government support in 2012 under the old Renewables Obligation mechanism and now have the option to switch to the new CfDs.

Drax Chief Executive Dorothy Thompson is not happy with a freeze on the carbon tax, claiming that the economics of the project were calculated on the basis that power prices would continue to rise in line with the carbon floor price. However, she admitted that the losses at Drax could be more than offset by savings on the carbon tax paid by those units that continue to burn coal.

The European Commission is also looking into whether a government guarantee on a £75 million loan for the conversion project breached EU rules on state aid. The case was raised by Friends of the Earth, which believes it makes no sense to run the Drax boilers on biomass imported from North America.

CCS: Still Years Ahead

Drax is also home to the White Rose project, one of only two carbon capture and storage projects now being funded by the DECC. White Rose partners Alstom, Drax, and BOC are now carrying out a front-end engineering study for coal CCS, while Shell and SSE are doing the same for gas at Peterhead in Scotland. The two projects will then compete for up to £1 billion in construction funding, while two other previously rejected projects seek funding through other means. The DECC program is running late, and the White Rose and Peterhead projects are unlikely to come on stream before the early 2020s—if they get off the ground at all. ■

— Charles Butcher is a UK-based contributing editor.