Utility mergers and acquisitions are on the upswing again. When faced with flat load growth, pervasive regulatory uncertainty, and the rising cost of doing business, larger companies are better able to afford expensive new plants while maintaining shareholder dividends.

No one ever accused Jim Rogers of thinking small. Over his years in the energy business, the Duke Energy CEO has frequently looked around his neighborhood and seen places he wanted to go—and companies he wanted to acquire.

During his 23 years as a CEO in the electricity business, Rogers has used mergers to grow his companies, his clout, and his reputation, both in industry and in the world of public policy and politics. When Rogers became PSI Energy (Public Service of Indiana) CEO in 1988, his gaze soon fixed on Cincinnati Gas and Electric. It was a troubled utility that nearly foundered on an ill-fated venture into nuclear power. The resulting marriage created a company called Cinergy. Rogers led the merged company for 11 years. In 2006 he orchestrated a deal in which powerhouse Duke acquired little Cinergy; after a suitable cooling-off period, Rogers ended up in the catbird seat.

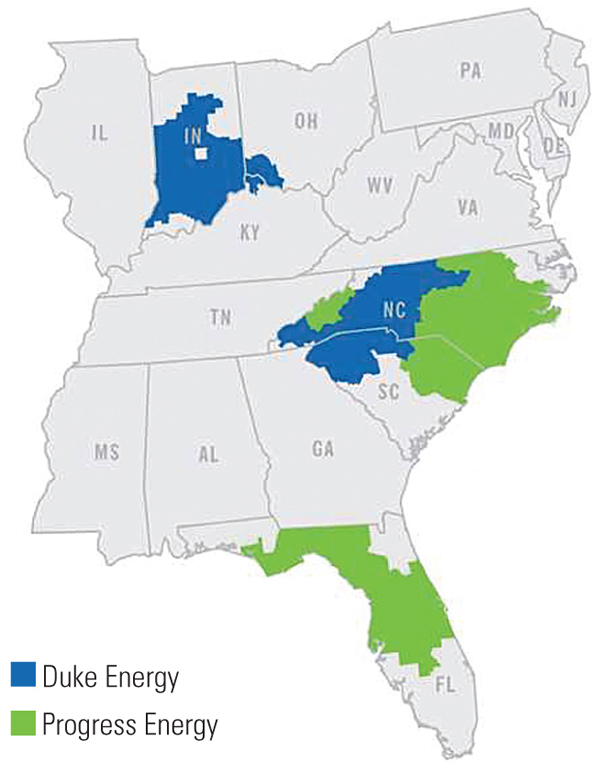

Rogers’ latest move is to use the muscle of his Charlotte, N.C., utility to acquire his Raleigh-based neighbor, Progress Energy, producing what would be the largest investor-owned utility (IOU) in the nation. In the deal announced in January, Duke will buy Progress for $13.7 billion in stock (at a modest 7% premium for Progress shareholders) and assume $12.2 billion in Progress debt, creating a behemoth with a market capitalization (the total value of the combined companies’ outstanding shares) of $37 billion.

The new company, to be headquartered in Charlotte, will own assets worth over $90 billion, serve some 7.1 million customers in six states (North Carolina, South Carolina, Florida, Ohio, Indiana, and Kentucky), and have 57 GW of generating capacity, including what the companies claim will be the largest regulated fleet of nuclear plants in the U.S. (Figure 1). Duke currently has seven nuclear units at three sites with a total nameplate capacity of 6,816 MW. Progress has five nuclear units at four sites, totaling 4,345 MW.

|

| 1. Mega-merger pending. Approval of the Duke Energy–Progress Energy merger will form a utility with over $90 billion in assets and annual revenues exceeding $22 billion. The generating capacity of the new Duke Energy Corp. will exceed 57,200 MW, and its service territory will cover more than 100,000 square miles. Source: Duke Energy, Progress Energy |

An Unlikely Marriage

The Duke-Progress merger caught many by surprise, in part because of the personalities involved. Often, mergers result when a young, aggressive executive takes over from an older, less-assertive leader looking for an easy path to the first tee. In the case of Duke and Progress, two very strong personalities—Rogers and Progress Chairman, President, and CEO Bill Johnson—are involved. Both can suck the oxygen out of a room just by entering. Johnson is well over six feet tall and fit. He is a former big-time college football player (he matriculated at Penn State under legendary football coach Joe Paterno but transferred to Duke University). Both he and Rogers are lawyers. Unlike the peripatetic and flashy Rogers, Johnson has spent his entire career as an electric utility executive at Progress.

According to the merger announcement, Rogers will become a company éminence grise, thinking big thoughts and working on the national and international stage. That’s a role that fits his personality. Rogers led the electricity industry’s failed endeavor to get Congress to enact a cap-and-trade program to control carbon dioxide emissions. He also has been a leading advocate of utility energy efficiency programs and renewable generation. A rare Democrat swimming in the sea of Republicans inhabiting industry executive suites, Rogers was successful in persuading his party to schedule its 2012 national convention, where President Obama will be renominated, in Charlotte.

Johnson will become the day-to-day chess master, moving the pieces around the utility’s broad territory. He has a reputation as a conventional but very effective manager. But the Zen master vs. chess master distinction may not hold, according to one veteran industry observer, who told POWER, “The border is pretty blurry. It’s hard to tell where public policy and company direction begin and end.”

A utility lobbyist told the environmental news service Greenwire, “Bill Johnson is a deep strategic thinker who is much less likely than Rogers to throw around flavor-of-the-month ideas in an effort to appease some regulators and legislators.”

What drives the Duke-Progress merger? Nuclear power plays an important role, according to several analysts. Barclays Capital investment banker James K. Asselstine, a former member of the Nuclear Regulatory Commission (NRC), made that point recently at a Platts nuclear conference in Maryland. He noted that at $10 billion a pop, new nuclear plants can sink a company.

NRG Energy, for example, was, until recently, heavily involved in the South Texas Project (STP) nuclear expansion, to the tune of more than $5 billion for its share. The company has a market capitalization of $5 billion, so failure in Texas could mean goodnight for NRG. On April 19, NRG announced it was writing down its investment in the development of STP Units 3 and 4, at least partially in response to the nuclear disaster in Japan.

A combined market cap of $37 billion for the new Duke-Progress utility would make investments in new nuclear more palatable, Asselstine concluded. Barclays Capital is advising Progress in the merger.

In an interview, Peter Fox-Penner of The Brattle Group agreed there was a nuclear aspect to the deal. “There is no question, a bigger balance sheet is better” for companies that see a future in new nukes, he said. “That’s clearly a major part of it.”

A well-run utility in two states with conventional cost-of-service state regulation, Progress was clearly an attractive target for a takeover. John Rowe, the aggressive CEO of Chicago-based Exelon Corp., acknowledged after the Duke announcement that he had considered a play for Progress. But Rowe said his number crunchers couldn’t make the deal work out.

Rowe’s Exelon lost a major merger move five years ago when its plan to take over New Jersey’s PSEG Corp. faltered because the New Jersey Board of Public Utilities nixed the deal. That merger would have created the largest U.S. IOU. Rowe made it clear he was still looking to grow through acquisitions, and on Apr. 28, Exelon announed a $7.9 billion deal to acquire Constellation Energy. If the deal is approved by regulators, it will make Exelon the country’s largest operator of nuclear plants.

FirstEnergy Deal Closes

As Duke and Progress were unveiling their merger—the start of at least a year-long journey—Cleveland-based FirstEnergy and Allegheny Energy, headquartered outside Pittsburgh, were wrapping up their $8.5 billion combo. Announced in February 2010, the FirstEnergy-Allegheny deal got the final seal of approval from the Pennsylvania Public Utilities Commission almost exactly a year later, on Feb. 25, 2011. The new, beefier FirstEnergy will have some $16 billion in annual revenues and six million customers in Pennsylvania, Ohio, Maryland, New Jersey, New York, Virginia, and West Virginia.

FirstEnergy was the result of merger mania that escalated in the 1980s and peaked in the 1990s. That episode was largely driven by structural changes in the electricity business that resulted in the creation of competitive wholesale and retail markets serving about half of the states, plus the unique need to deal with troubled, high-cost nuclear plants. Akron, Ohio–based FirstEnergy was born of the 1986 merger of Cleveland Electric Illuminating and Toledo Edison, two troubled neighbors who joined to create Centerior Energy Corp. Toledo owned the Davis-Besse nuclear plant, which has had a checkered history (Figure 2). Centerior became FirstEnergy in 1997 by merging with Ohio Edison. FirstEnergy acquired GPU Corp. in 2001, which owned Three Mile Island (TMI) Unit 2, which was shut down in 1979 and never reopened. Exelon Nuclear owns and operates TMI Unit 1.

|

| 2. Buy rather than build. FirstEnergy Nuclear Operating Co., a subsidiary of FirstEnergy Corp., owns the single-unit 879-MW Davis-Besse Nuclear Power Station. The plant was originally owned by Centerior Energy Corp.—created by the merger of Cleveland Electric Illuminating and Toledo Edison—and was acquired by FirstEnergy in 1997. In August 2010, FirstEnergy submitted a license renewal application for Davis-Besse (which is licensed to operate through 2017) to the NRC, a process that is sure to be extremely contentious given the plant’s uneven operating history. Source: NRC |

Merchant Mergers

Mergers on the merchant side of the business are also picking up speed. The most recent example is the newly minted GenOn Energy Inc., a mixture of Mirant Corp. and RRI Energy Inc. When that deal closed in early December 2010, the combined 23,600-MW merchant operator instantly became one of the largest independent power producers in the U.S. Edward R. Muller, chairman and CEO of GenOn, said the merger “will create significant near-term stockholder value driven by $150 million of annual cost savings.”

Is This a Trend?

Are the Duke-Progress, FirstEnergy-Allegheny, and Exelon–Constellation Energy deals evidence of a revitalized trend of electric company mergers? Opinions are mixed. According to Thomson Reuters Deals Intelligence, “Merger activity in the energy and power sector is off to its fastest ever start in a year, with nearly $94 billion in deals so far in 2011,” up 40% over last year. That assessment came in February, after the Duke announcement and just as the FirstEnergy deal was closing. The figures include foreign merger and acquisition (M&A) activity, such as BP’s $7 billion hookup with India’s Reliance Industries. According to Thomson Reuters, “Cross-border energy & power deals have accounted for $58.1 billion of the activity this year, or 63 percent of worldwide mergers in the sector. U.S. targeted deals have accounted for roughly half of the volume.”

Berenson & Co. electric analyst Ed Tirello is bullish about electric company mergers. But then, he would be. Tirello is famous for his 1987 “50 in five” prediction: He predicted that only 50 investor-owned electric utilities would be around in 1992. He missed. According to the Energy Information Administration, in 2000 there were 240 IOUs in the U.S.

Tirello chuckles at his missed prognostication. “It’s taken a bit longer,” he says with good humor, “but the premise doesn’t go away. Look at the industry as a whole. It doesn’t matter what the generating fleet looks like today, it is all going to have to be turned over in this country in the next 20 years. Years ago, we did five, 10, 20-year advanced plans. Deregulation messed that up and we stopped doing it. And we are back to doing that planning again.

“[The Environmental Protection Agency] is putting pressure on generation. Plants are getting old. Rules change and fuels change, and you must get the money somewhere to keep the lights on.” So, in Tirello’s mind, the way to find the resources is to bulk up. “When you look at mergers so far,” says Tirello, “each one had a particular reason. But the overall theme is still there: fewer and larger. You need stronger balance sheets to change the fleet over.”

The Brattle Group’s Fox-Penner isn’t buying all of Tirello’s analysis. “The industry is always considering mergers and acquisitions,” he said. “Nothing jumps out at me as a major driving force today. There are always a lot of factors hitting the industry at any one time, things such as the cost of debt and equity, strategic factors, regulation. Maybe there are times when they all align, as Ed Tirello thought they did in the 1980s, but I don’t see any kind of alignment of factors at this time.”

Fox-Penner points to the deal last year when PPL Corp. agreed to buy E.ON.US for $7.6 billion (cash and debt) as an example of how particulars drive business marriages. In that case, PPL, based in Allentown, Pa., had become essentially an unregulated merchant generator. The U.S. arm of the German multinational E.ON was the owner of conventional, state-regulated, cost-of-service utilities: Louisville Gas & Electric and Kentucky Utilities. The particular structural elements “led to that particular deal” and not some larger force at work in the industry.

Following the same playbook as Tirello, Todd Shipman of Standard & Poor’s said the rating agency expects to see “25 in 5” or 25 utility mergers in the next five years. Given the Duke-Progress, Northeast Utilities–NStar, and FirstEnergy-Allegheny hookups over the past year, that prediction seems a safe bet.

Shipman pointed to several factors that are likely to bring utilities together over the next few years:

- Low electricity sales growth putting pressure on dividend growth.

- Rising costs of environmental retrofits in response to regulatory and legislative requirements.

- The perpetual regulatory uncertainty that hangs over the industry.

- Direct investment by deep-pocketed foreign countries or companies (often there is little difference between the two) in either equities or as a market for technology sales.

A carefully designed complementary merger can reduce corporate risks and, therefore, costs, providing desirable upward pressure on company earnings over the long term.

Veteran Washington energy lawyer Clint Vince is agnostic when it comes to merger trends. “There is a certain logic” to electric generating company mergers, he said in an interview. “The businesses have spread out beyond state borders, it’s an increasingly competitive business, and major capital costs, particularly for nuclear, are increasing, so it makes sense to spread out over a larger customer base for some companies.” On the other hand, Vince said, “It’s hard to know if we are actually seeing a trend. It will take some more time to reach any conclusion on that question.”

Add the market research firm of Wood Mackenzie to those who see a merger trend in progress. In a recent report, Wood Mackenzie says it expects M&A activity in the power business to “intensify in 2011 as North American power markets remain oversupplied with power generating capacity and face sluggish demand growth prospects and environmental policy pressures.” Hind Farag, North American research manager for the firm, notes that during the past two years, some 13% of installed North American power plant capacity has been involved in M&A deals. “Since January 2009,” she said, “completed and announced M&A activity has involved at least 148 gigawatts of existing generators in North America while only about 70 GW of new resources achieved commercial operation during the same time period.”

Generalizations are dangerous when discussing “energy” mergers, because that rubric encompasses so much: Integrated oil companies, wildcatters, new shale gas developers, merchant electric generators, regulated electric companies, and local gas distribution companies all fall under the heading. Tracking trends across such a diverse landscape becomes daunting. One indicator, and it is far from conclusive, is the pace of mergers coming before the Federal Energy Regulatory Commission (FERC). FERC must review all mergers that involve electric utility assets used in interstate commerce. According to FERC data, the late 1990s represented the peak of the agency’s merger activity. FERC dealt with 17 merger applications in 1997, 15 in 1999, and 16 in 2000. In contrast, it saw four merger applications in 2005, 10 in 2006, five in 2007, three in 2008 and 2009, and two last year.

Though it’s difficult to find a clear-cut merger trend, one new element feeds the urge to merge. Since 2005 it has become easier—although still time-consuming and costly—to pull off a major merger. For 70 years, starting with the 1935 Public Utility Holding Company Act (PUHCA), federal policy looked askance at electric utility mergers, although the vigilance waned considerably in the final two decades of that period. The 1935 law was the result of the collapse of Samuel Insull’s pyramid of utility holding companies in the Great Depression, a disaster that dwarfed this century’s Fall of the House of Enron.

Congress in the 2005 Energy Policy Act essentially repealed PUHCA requirements for vigorous FERC merger oversight. Since then, the states have largely supervised mergers of firms under their jurisdiction. New Jersey, not FERC, killed the Exelon-PSEG affair.

Only a few states have taken their merger authority to heart. Scott Hempling, head of the National Regulatory Research Institute, the policy think tank for the National Association of Regulatory Utility Commissioners, said he has been trying to “encourage states to develop a merger policy” but has had limited success.

Hempling argues that states should look hard at mergers based on whether they further the broad interests of consumers in the state, not simply based on whether they are benign or on what state regulators can extort from the parties in merger conditions. “There has not really been an understanding of the key effects a merger can have” on a state, Hempling says, citing potential issues such as the impact on ancillary services, renewable generation, and transmission needs. “Are we producing corporate structures so diverse and complex and financing too difficult for normally staffed regulators to keep track of,” he asks? His implication is that the answer is yes.

— Kennedy Maize is a POWER contributing editor and executive editor of MANAGING POWER.