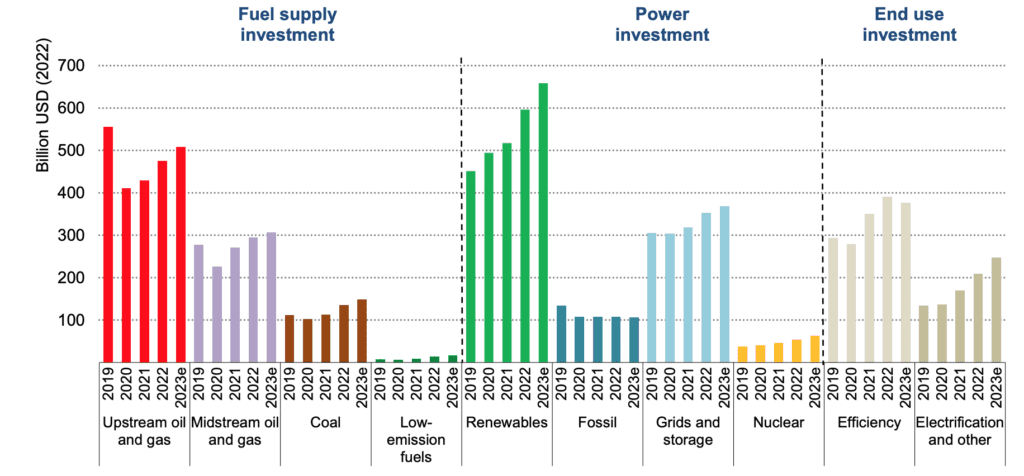

The International Energy Agency (IEA) expects investment in clean energy technologies, including “renewable power, nuclear, grids, storage, low-emission fuels, efficiency improvements and end-use renewables and electrification,” to exceed $1.7 trillion in 2023, the most ever. Yet, even as clean energy investments grow, more than $1 trillion is expected to be invested in unabated fossil fuel supply and power, mainly oil and gas, but also coal (Figure 1), which is, notably, more than a 6% increase in unabated fossil fuel supply investments.

The findings, released on May 25 in the IEA’s latest World Energy Investment report, suggest spending in some fossil fuel categories will return to pre-COVID levels. “Investment in coal supply is expected to rise by 10% in 2023, and is already well above pre-pandemic levels,” the report says. And while investment in new coal-fired power plants remains on a declining trend, researchers were somewhat alarmed to see 40 GW of new coal plants being approved in 2022—the highest figure since 2016.

Almost all of the new coal-fired capacity is expected to be built in China. This reflects “the high political priority attached to energy security after severe electricity market strains in 2021 and 2022,” the report says. Meanwhile, there were no new coal final investment decisions (FIDs) made in Indonesia in 2022, which the IEA said was “an encouraging signal.” In other Southeast Asian countries and the rest of the world, only a very limited number of new coal-fired plants were approved for development, reflecting pledges from a range of countries and financial institutions to stop backing their construction. Those coal plants that were approved continue to be of relatively high efficiency, with subcritical facilities dropping to below 5% of new FIDs, according to the report.

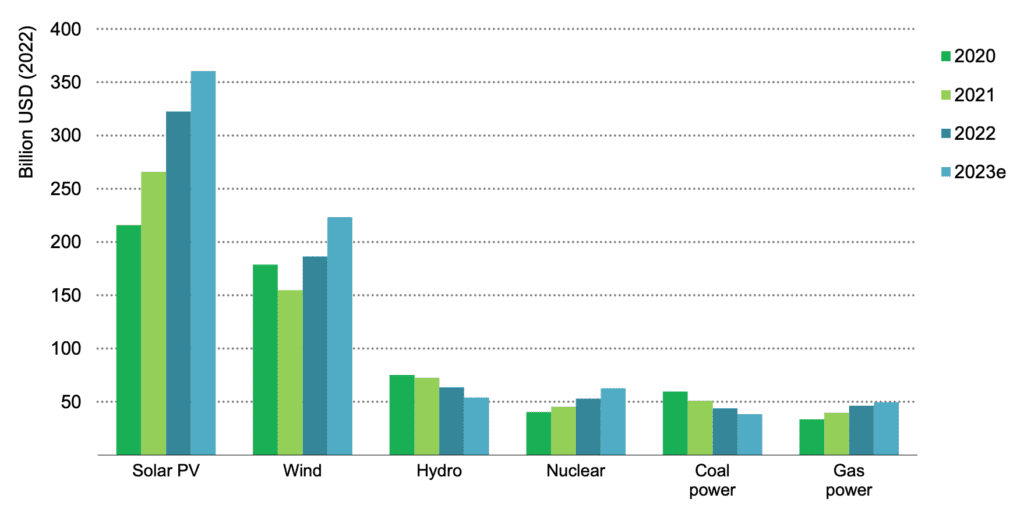

Still, the 15% increase in fossil fuel investment between 2021 and 2023, is far less than the increase expected over the same period for clean energy investments (up more than 24%). “Clean energy is moving fast—faster than many people realise. This is clear in the investment trends, where clean technologies are pulling away from fossil fuels,” IEA Executive Director Fatih Birol said in a statement released in tandem with the report. “For every dollar invested in fossil fuels, about 1.7 dollars are now going into clean energy. Five years ago, this ratio was one-to-one. One shining example is investment in solar, which is set to overtake the amount of investment going into oil production for the first time.”

Among clean energy bright spots mentioned in the report were solar investments in India; deployment in Brazil, which is said to be on a steady upward curve; and investor activity in parts of the Middle East, which is reportedly picking up, notably in Saudi Arabia, the United Arab Emirates, and Oman. Nonetheless, higher interest rates, unclear policy frameworks and market designs, financially strained utilities, and a high cost of capital are holding back investment in many other countries.

“The crucial open question is how quickly clean energy investment scales up in emerging and developing economies, where supportive strategies and policies will need to be accompanied by improved access to finance,” the report says. For the moment, sustainable finance instruments remain concentrated in advanced economies, accounting for nearly 80% of sustainable debt issuance in 2022. “Issuances elsewhere (outside China) are growing from a low base, with India’s successful first green bond a landmark in this sector. Scaling up these instruments and mobilising much greater support from development finance institutions will be critical to the continued broadening and acceleration of clean energy transitions,” it says.

—Aaron Larson is POWER’s executive editor (@AaronL_Power, @POWERmagazine).