Authored by Bryan Sillaman and James Alford of Hughes Hubbard

In the midst of the global COVID-19 crisis, another unprecedented event took place that was largely overshadowed by more urgent, and life-threatening, circumstances. On April 20, 2020, the price of U.S. West Texas Intermediate crude oil dropped below zero dollars per barrel (bbl), plunging past negative $40/bbl at one point during the day. This never-before-seen market reaction stemmed from an unforgiving combination of a sudden and drastic drop in global demand for oil; a dispute among certain countries on the level of production cuts; and a lack of storage capacity sufficient to accommodate U.S. supply. Although the price rebounded in the following days, the mid-term effects of the COVID crisis on the energy industry as a whole will continue to play out over months and years to come.

According to the International Energy Agency (IEA), global energy demand in the first quarter of 2020 dropped 3.8%, as compared to the first quarter of 2019. Depending on the length and severity of lockdown measures, as well as the potential for a second wave of infections, global energy demand could decrease by 6% or more for 2020, which if it occurs would be a decrease in energy demand seven times greater than that which occurred after the 2008 financial crisis.

Among the fuel categories assessed by the IEA—coal, oil, natural gas, nuclear, and renewables—only renewables registered a global increase in use during the first quarter of 2020, rising about 1.5%, as compared to the first quarter of 2019. This resilience—attributed in part to low operating costs and the completion of some significant renewable projects from 2019—stands in stark contrast to the global decrease in usage of coal (down by about 8% as compared to 1Q2019) and oil (down by about 6.5% as compared to 1Q2019) in the same period.

While some of that decrease will undoubtedly reverse when economies are functioning more normally, it also has investors, business leaders, and policy makers around the globe assessing the broader implications of the energy make-up in various jurisdictions.

The Outlook for ‘Clean’ and ‘Renewable’ Energy

There were certain signs of a more definitive shift toward clean and renewable energies prior to the COVID crisis. 2019 saw mass protests, many organized by young people around the world, against the future impact of climate change. In his influential 2020 letter to chief executive offices—titled “A Fundamental Reshaping of Finance”—Larry Fink, CEO of BlackRock, equated climate risk with investment risk, and noted that BlackRock not only would increasingly evaluate the ways in which companies in which they invest are managing such risk, but would also vote against management and board directors “when companies are not making sufficient progress on sustainability-related disclosures and the business practices and plans underlying them.”

Global super-major oil and gas companies are increasingly releasing their climate strategies and shifting their focus to the clean and renewable space, whether through acquisitions of clean and renewable companies and technologies, and/or through investment in carbon capture programs. In France, clean and renewable projects are a key part of the country’s Programmation pluriannuelle de l’energie (“multi-year energy plan”), and are estimated to contribute upward of €21 billion to the French economy by 2028, or 10% of the current value of the French industrial sector. The European Union’s European Green Deal is aimed at making the European Union carbon neutral by 2050, and to do so is planning to invest €1 trillion in sustainable investments over the next decade to do so.

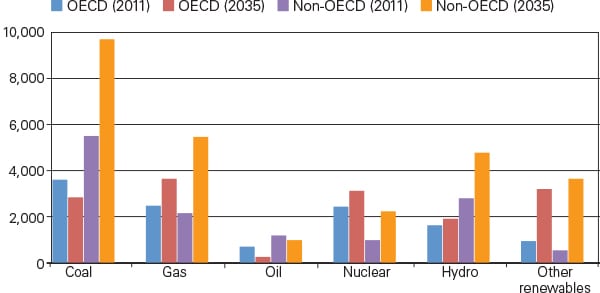

According to Bloomberg New Energy Finance (BloombergNEF), 2019 saw $336.3 billion in clean energy investment (led by onshore and offshore wind, followed by solar), with China comprising $83.4 billion of this amount. The U.S.—which is second only to China in installed renewable capacity—doubled its renewables capacity between 2010 and the end of the decade, and wind and solar power have already passed coal, gas. and hydroelectric power as the two leading sources of electric power, between them accounting for about 10% of electrical generation in the U.S.

Large-scale, utility-grade wind and solar projects, which a decade ago were possible only through tax incentives and state-level mandates, are now competitive on price, thanks in part to decreased manufacturing costs and innovations in solar panel and wind turbine technology and design.

While the investment outlook for 2020 is currently plagued with uncertainty, the confluence of factors driving change in the global clean and renewable energy industry is likely here to stay. As it will in other sectors, this crisis will prompt new innovations and has the potential to spur even further change throughout the energy sector.

Renewable energy capacity is projected to expand by 50% between 2019 and 2024 globally, led by solar photovoltaic (PV) and significant growth in distributed solar power PV systems. Offshore wind is projected to contribute 4% of this increase, with its capacity forecast to triple by 2024. A 2019 assessment by BloombergNEF of 104 emerging markets ranked the top five for clean energy investment as India, Chile, Brazil, China, and Kenya, due to a combination of clean energy targets, policy initiatives, and robust natural and/or human resources.

Compliance Risks Relevant to Clean and Renewables Sector

With all the enthusiasm and promise that these projects and technologies hold, entry into, or expansion of, this space is not without compliance risk, particularly as such projects gain momentum across emerging markets and the developing world. While some of these risks are consistent with what we see in more mature, extractive industries, others are unique to the clean and renewables space, and should be considered by companies that are active or entering into this area, particularly in jurisdictions where they may be less experienced.

Evolving Regulatory Environments: In certain jurisdictions, the technology and potential profits arising from a clean or renewable energy project may be more advanced than the regulatory framework that governs:

- The government’s role (if any) in awarding such projects.

- The licensing and permitting process surrounding such projects.

- The tax, tariff, subsidy, or other fiscal regimes governing such projects.

- Whether, and to what extent, local or national content obligations apply.

The greater the uncertainty surrounding these key aspects of a project’s viability and profitability, the greater the potential, at least, for compliance exposure in how companies address these uncertainties. The engagement of lobbyists or efforts to otherwise influence legislation or government-backed initiatives (at a national, state or local level) can present heightened risk for companies participating or investing in these activities. While it may not be feasible to have gained complete transparency and resolution on all these areas before investing in a clean or renewable energy project, companies should seek to have a clear-eyed view of the areas of greatest uncertainty and risk from a regulatory perspective, and develop an approach for how they will address those uncertainties in a risk-based manner to mitigate their compliance risk.

“Finders” and Other Intermediaries: In any developing industry, there are undoubtedly those who come out of the woodwork in an effort to make a quick fortune by using their connections, oftentimes by playing matchmaker between those who can develop or finance projects and those who own land, resources, or the ability to influence regulatory levers that can make or break a project’s success. The clean and renewable space is no different, as individuals seek to pitch investment ideas to companies looking to diversify their renewables portfolio or enter the space for the first time. Companies should be on the lookout for such third parties when they are considering potential opportunities, and inquire specifically of any counterparties whether proceeds or funds will go to third party individuals or entities that are not transparently identified. Contractual representations and warranties and, where necessary, robust third-party due diligence, can help mitigate these risks.

Opaque Ownership of New Market Players: One of the exciting things about the clean and renewable sector is the number of small, entrepreneurial companies that are contributing in meaningful ways to the technological enhancements and investment opportunities that are helping to grow the industry. Partnering with or acquiring such companies may offer opportunities for more established energy industry players to enter particular markets, projects, or sectors in an efficient way. Such partnerships and acquisitions should be closely assessed, however, from a compliance perspective, to ensure that there is a clear and transparent understanding of:

- The ownership and management of the companies.

- The provenance of any asset interests that have been acquired by them.

- Their role going forward, including any role that may require interactions with public officials (i.e., obtaining governmental approvals, licenses, etc.).

Smaller, entrepreneurial companies that are similarly looking for financing or a potential acquisition down the road should also give thought to how a financing institution, asset manager, or larger industry player may assess them from a compliance perspective, to help gain a competitive advantage over peers who may not have factored such elements into their value propositions.

Partnering with Governmental Entities: A growing trend internationally is for governments to partner with private power generators under national public-private partnership laws designed to facilitate public and private co-ventures to undertake large-scale generation of renewable energy. Partnering with a government, or government-owned entity, may present its own challenges from a compliance perspective, as the representatives of that entity will likely themselves be considered as foreign public officials under laws such as the U.S. Foreign Corrupt Practices Act. As such, the roles and activities of the state-owned company and its representatives should be clearly defined in advance, to ensure that there is a clear understanding of the division of labor and responsibility for key areas that can present compliance risk such as those identified above. Companies should also seek to define in advance how they will address topics such as compensation for board representatives from the state-owned entity; permissible travel and hospitality expenditures; and whether such partnering brings with it obligations for corporate social responsibility or related types of activities.

Sources of Financing: Companies operating in, or seeking to enter, this area should consider the financing structure associated with a proposed project. For utility-scale projects, project financing is the method of financing frequently used to raise debt for project development and construction. This is typically structured as non-recourse financing in which the lender relies on revenues generated by the project to repay the loan. In effect, the lender takes the same risk as the developers of the project and compliance issues can therefore become particularly important in their assessment of the overall risk profile of the project. In addition, the multilateral development banks (MDB) have made the financing of renewable energy projects a lending priority worldwide in eligible countries. Any such financing by an MDB brings with it the obligation that companies involved comply with the ethical and compliance obligations of the particular MDB, which go beyond prohibiting corruption and include other types of unethical conduct, such as fraud, misrepresentations, and collusion. Any compliance policies, programs or training, should therefore be developed with such obligations in mind.

Country / Geographic Risk: As noted above, emerging markets present substantial opportunity for future investment in clean and renewable projects, and have also helped to produce equipment at lower cost, making such projects in developed markets bankable. By way of example, China manufactures about 70% of solar panels used in utility-grade or residential solar projects around the world, with another 10% to 15% coming from Southeast Asia. While these incredible economies of scale have helped drive down the price of solar projects, China remains a country that presents heightened risk from a corruption perspective, despite a significant campaign against corrupt activities by President Xi Jingping. Clean energy and renewable projects are also an area of increased government and investment focus in other geographies, such as India, Central and South America, Africa, and the Middle East, that present their own unique and varied corruption risks. Companies that are looking to invest in projects in these jurisdictions, or who may look to companies operating there as partners or critical parts of their supply chains, should assess the corruption environment in such jurisdictions in order to measure the potential risk associated with operations there.

Conclusion

As with many things, the long-term impact that the COVID-19 crisis will have on the clean energy and renewable sector remains to be seen. Nonetheless, the innovation and potential, as well as the appetite, for more sustainable technologies and energy sources appear promising for years to come. To ensure that the benefits of such projects from an environmental perspective are not offset by governance and compliance failures, companies should ensure that they take a holistic view of the areas of potential risk, and develop a mitigation plan consistent with those risks to better protect themselves and ensure a profitable and environmentally friendly project for the future.

—Bryan Sillaman is a managing partner with Hughes Hubbard’s Paris office and a part of the firm’s renewable energy and anti-corruption and internal investigation practice groups. He regularly advises energy companies on compliance risks associated with projects around the world. He can be contacted at bryan.sillaman@hugheshubbard.com. Jim Alford serves as Counsel in Hughes Hubbard’s Washington, D.C., office. He specializes in project development and financing of clean and renewable energy projects internationally, with a focus on Latin America and Mexico, and is a member of the firm’s renewable energy, corporate, finance and Latin America practice groups. He can be contacted at james.alford@hugheshubbard.com.