The onset of the COVID-19 pandemic is not the type of thing enterprise technologists could see in our magic crystal ball. Before the onset of the virus and its effects, I set out three predictions for the energy, utilities, and resources sector for the coming year—but of course, a global shutdown of business, transport, and daily life was not one of the things I anticipated. But as I revisit my predictions, some of them will hold up better than others, although some may come to pass sooner and others will simply be delayed.

Renewables Surge as the Energy Industry Looks for New Growth Areas

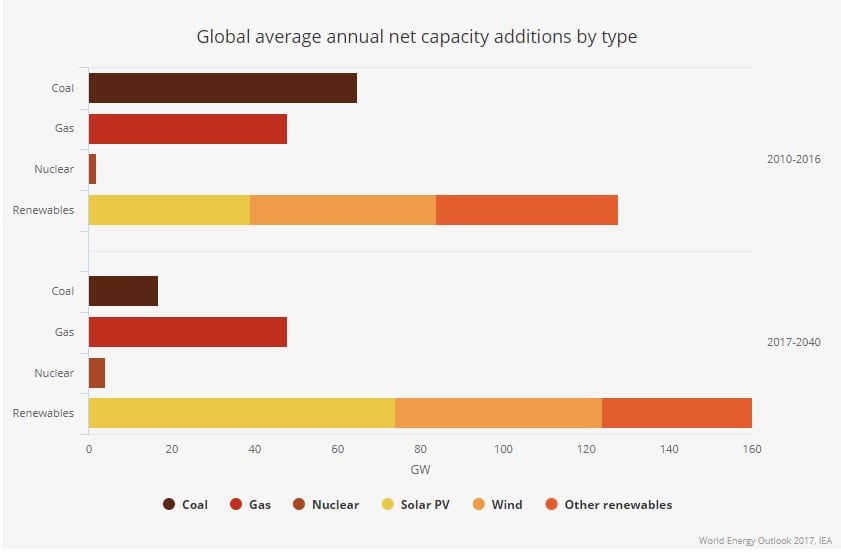

Due in part to increasing demand for energy, I predicted for the second year in a row that the growth of renewables in the energy mix would increase by double digits till 2024. Of course, demand for oil and gas has cratered as the world stays at home, but I think we can stand by the prediction on renewable energy, even though it is higher than some other predictions that put growth more in line of past performance of 5.5% annual growth or 7.9% between 2018 and 2019. I also mentioned the importance of companies diversifying their energy mix to remain relevant and sustainable in the long term. This trend is continuing at a pace, and we see some emerging leaders riding in on renewable power and major energy companies already pivoting some of their capacity to renewables—although exceptions hold out, according to Platt’s. If nothing else, renewables will grow even faster than before as a percentage of energy consumed given the hit being taken by the oil and gas sector.

The International Energy Agency has revised its prediction for monthly oil demand for 2020 compared to 2019, although it suggests demand will return to normal toward the end of this year. Commercial airlines, some manufacturing, and personal automobiles are all idled right now, cratering demand, even as a global price war drove down price. Now, outputs like gasoline are at prices unheard of for decades, but demand is inelastic due to stay-at-home orders across much of the world. Some demand patterns will come back slowly, but as stated, the IEA is optimistic in the intermediate term.

The immediate impact on the oil industry is hard to deny. Diamond Drilling filed for Chapter 11 bankruptcy, citing the price war and coronavirus. Oil and gas producers are scaling back investment plans globally and drawing back their capital investment programs. According to Natural Gas Intelligence, an index of U.S. exploration and production companies plan to scale back their capital spending by 8%, or about $8.3 billion. Some parts of the industry will continue to invest more than others, with offshore expected to do better than shale, in part because capital investments here will not pay off for another two to five years. As contracts are terminated, the flexibility to stack and preserve assets, and manage operational expenditures and margins, while ensuring safety and that critical maintenance is performed, becomes even more important for upstream asset owners.

With oil having traded below zero, the only substantial growth area for the sector in the immediate term may be storage, as globally there is a shortage of capacity to hold onto oil pumped from the ground because it is not being consumed. So, while fabrication of new floating production, storage, and offloading (FPSO) vessels is on hold, I am aware of at least one FPSO vessel under contract that is now to be converted specifically for storage. We may see several more of these projects convert to storage-only, or existing FPSO vessels used strictly for storage until there is somewhere to go with oil until demand returns.

Adding Value Through Remote Assistance and Customer Services Pays Off

While we will always need energy, current times are proof that traditional commodities-based generation methods are impacted by fluctuations in price. This is one reason many energy and utilities organizations have expanded into value-added services that drive new revenue and give customers a reason to prefer them. This is particularly a strong trend in Europe and especially in the UK, where a more open retail market enables customers to choose from whom they should buy their energy. And customers are demanding suppliers focus on environmental aspects including sustainability, emissions, and the drive to a carbon-neutral economy.

Given the COVID-19 pandemic, utilities organizations that also want to deliver appliance or equipment repair services to customers will benefit from adopting technologies such as remote assistance, which can either guide customers through repair and maintenance projects or give a technician on-site access to experts who can offer consultation from a remote location.

In countries such as the UK, there is heightened competition for retail customers, and larger utilities organizations must make investments in customer services and enabling technology in order to avoid incursions by more nimble competitors. A large utility organization will have to compete for customer equipment service business with dedicated contracting and service organizations running advanced omnichannel customer relationship management (CRM) systems driven by artificial intelligence.

Careful Asset Management Leads to Better Foresight

While assets in the energy sector—from offshore platforms to oil refineries to power generation turbines—are long-lived and carefully managed, I predict that given market volatility we will see an increased focus on systems to support sound, long-term asset lifecycle management decisions. This means demand in the sector for complete enterprise asset management (EAM) software will increase as executive teams realize they cannot manage what they cannot see. And they will need to see more than they have before—operational cost, output and asset readiness, and capacity metrics in the context of the goals of the organization. They will need to decide which assets to idle and then manage extensive decommissioning processes. They will need to decide where to build additional capacity or make net new investments, which will require advanced what-if scenario planning.

In the coming years, we will see the energy sector looking at project and asset lifecycle management as a strategic solution rather than as a pure work management tool to ensure preventive maintenance actions are performed to help reduce operational cost. A move toward a more diverse portfolio of generation assets will not only reduce operational cost but will also help set the most profitable and competitive rate (trading and retailing) based on the generating costs of these different assets. They will look for software and a vendor ecosystem that can help them manage returns on their capital assets by harnessing asset data and either using it for decision support or increased automation.

—Colin Beaney is global industry director for Energy, Utilities & Resources with IFS.