I spent the week before this issue went to press at IHS Energy’s CERAWeek in Houston, listening and talking to many of the attendees representing 55 countries during the annual event that examines strategic issues facing the global energy industry. Though several themes were addressed, I want to focus on one in this column: competitiveness.

Cost competitiveness is probably what comes to mind first, and that did get its due attention, including from U.S. Department of Energy Secretary Ernest Moniz, who said that it’s really important to reduce the costs of low-carbon technologies. As the week progressed, several other dimensions of competitiveness emerged. How competitive are you and your company along each of them?

Supply Competitiveness

Though there was consensus about the continued bright outlook for shale oil and gas in North America, several speakers acknowledged that shale resources aren’t a solution everywhere. Fuel competitiveness involves cost and availability but also surety of supply.

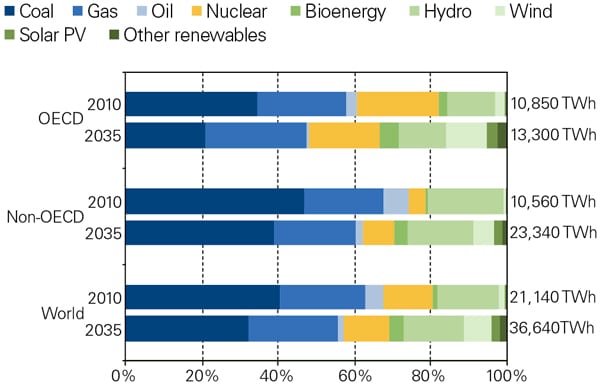

In developing nations, natural gas is not cost-competitive with other options, including renewables. As a representative of China’s state grid noted, if China can get gas from the U.S. and Russia, and if it can develop its own shale gas, then gas may be the best option, especially for coastal areas. Until then, China sees wind power as a good long-term option, nuclear as a good mid- and long-term option, with continued use of coal, though at a lower percentage of the total mix.

Meanwhile, as Black & Veatch (B&V) Chairman, President, and CEO Steven Edwards commented, growth in the U.S. is mostly around renewables, driven “by the competitiveness of renewables in the marketplace.”

By now, readers of POWER and our GAS POWER Direct eletter are familiar with the mismatch between natural gas and electricity markets, but there’s an even bigger challenge. In fact, Spectra Energy President and CEO Gregory Ebel argued that gas/electric trading day coordination is a red herring and that fundamentally, what we have is a capacity problem. That capacity problem translates into supply security challenges. Reliability of supply as an element of national security was a refrain at the event because Russian troops had recently entered Crimea, but U.S. gas delivery was also top of mind.

The competition for natural gas this winter shone a light on the problem. I even heard one CEO explain that his generating company has been in the position of having the independent system operator tell a plant to run, while his gas supplier said it couldn’t deliver the gas. Neither side could believe the problem was real until the CEO got them conferenced together by phone.

Workforce Competitiveness

Several speakers, including Diane McQueen, Alberta’s energy minister, bemoaned the difficulty of staffing energy projects. As IHS Vice President John Larson noted, though U.S. unemployment figures suggest there are workers to fill the labor shortages across the energy sector, there’s a “skills mismatch.” Diversifying the workforce was one solution that Secretary Moniz mentioned. Workforce diversity was also the focus of a reception hosted by the American Petroleum Institute for women in the energy industry.

Ecosystem Competitiveness

The relevant competitive dimensions depend on your business ecosystem, and cultural values are an increasingly important dimension.

As Spectra’s Ebel observed, public opinion is “never right or wrong—it is what it is.” And Harald Schwager, member of the Board of Executive Directors for Germany’s BASF SE, the world’s largest chemical company, noted that Europeans differ from the rest of the world in believing that “energy is only good energy if it’s expensive,” because only then, they believe, will people not waste energy. Everywhere else, the belief is that only cheap energy is good energy.

In a Thursday plenary, B&V’s Edwards noted that the Chinese Premier Li Keqiang had the previous day declared war on pollution. In China, said Carlos Pascual, special envoy for international energy affairs at the U.S. Department of State, addressing pollution—especially along the coast—is an even higher priority than cost containment (gas is twice as expensive as coal) or climate change.

Global Competitiveness

In his opening address to Wednesday’s gas sessions, President and CEO of Siemens AG Joe Kaeser argued that the U.S. has a once-in-a-lifetime chance to develop an industrial manufacturing sector because energy is so cheap and stable, “and people in this country know how to handle it.” That’s why global companies like his continue to invest in the U.S. “Today,” he said, “it’s all about going west. The U.S. is once again the place to be.”

That theme was carried forward by BASF’s Schwager, who noted that Germany’s BASF has started to shift investment to the U.S., including new plants. Investment in Germany is down from 60% of total investment to less than 50% for basic chemicals, although the total amount of investment is up. That doesn’t mean the advantage is solely America’s; Europe isn’t doing too badly, he argued, especially given its strong infrastructure.

Power Plant Competitiveness

As Robbie Diamond, president and CEO of Securing America’s Future Energy, noted, we can control our domestic energy policy but we can’t control the global market. That attitude should also apply to generating companies: You can’t control the market, but you can control your own operations by ensuring that they are as competitive as new technologies, smarter practices, and energy-efficient operations can make them. Nearly every article in this issue relates in some way to the issue of competitiveness. How will you become more competitive? ■

— Gail Reitenbach, PhD is POWER’s editor. Follow her @GailReit and the POWER team @POWERmagazine.