Electric generation and natural gas, both important to each other, have differing cultures, vocabularies, and histories, so making them work together has been a challenge.

Glut. That word describes the state of natural gas, now the dominant electric generating fuel in the U.S. It has profound implications for the generating business and for the gas pipeline and storage industry.

Merriam-Webster’s Collegiate Dictionary, 11th Edition, defines glut as “to flood (the market) with goods so that supply exceeds demand.” That is where the U.S. finds itself today with regard to natural gas. In less than a decade gas has toppled coal, and most experts predict the situation will continue.

As anyone who has taken Economics 101 understands, when supply exceeds demand, prices fall. A decade ago, energy guru Daniel Yergin was predicting that the U.S. would soon become a major importer of liquefied natural gas (LNG), based on an assumption that natural gas supplies were limited and diminishing. Domestic gas prices were rising, making LNG imports look attractive, Yergin argued.

That prediction came at about the same time that Range Resources Corp. used horizontal drilling and hydraulic fracturing in Pennsylvania’s Marcellus Shale formation, striking it rich. Today, the U.S. is on the verge of becoming a large exporter of natural gas, having been a gas importer for many years, primarily from Mexico and Canada. The U.S. Energy Information Administration (EIA) reported recently that the U.S. was a net exporter of natural gas for three of the first five months of 2017. It looks as if that will continue as LNG export facilities are replacing plans for LNG import terminals.

Transforming Electric Generation

More importantly, plentiful natural gas supply has transformed electric generation. Today, more gas is coming to market despite declining gas prices. Gas companies continue to drill new wells, despite the price decline. Much of that gas flows to existing and new electric generation. For example, DTE Energy, formerly Detroit Edison, is seeking to build a new 1,100-MW gas-fired combined cycle plant at a Michigan site where the company operates two older coal-fired plants, which would be shuttered.

When the fracking revolution hit the U.S. nearly a decade ago, natural gas was a swing fuel, often used by utilities as a load-following resource. Coal still dominated electric generation by a wide margin.

In the late 1980s and early 1990s, a “gas bubble” as a result of federal decontrol of natural gas prices created a new, competitive gas industry. It was non-utility generation built on cheap gas, challenging conventional utility-dominated generation, long believed to be a natural monopoly. The bubble never burst, but slowly deflated, and the merchant generators began diversifying their technology to coal and renewables.

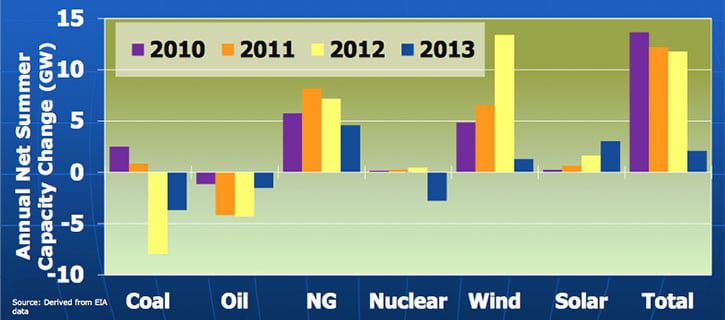

In 2004, using technology the late oil industry pioneer George Mitchell long promoted, the world for electricity generation turned upside down. Gas locked up in Devonian shale formations (and oil as well, in North Dakota) was available in tremendous abundance. According to the American Petroleum Institute, shale gas accounted for 5% of national gas production in 2006. By 2013, the figure had risen to 40%.

This July, the Colorado School of Mines’ “Potential Gas Committee (PGC),” long the gold standard for estimates of gas resources in the U.S., released its latest biennial assessment of the nation’s gas resources. The PGC’s estimate was astounding. The committee of geological and economic experts said the U.S. has a “total technically recoverable resource base of 2,817 trillion cubic feet (Tcf) as of year-end 2016. This is the highest resource evaluation in the Committee’s 52-year history, exceeding the previous high assessment (from 2014) by 302 Tcf (increase of 12%).”

Natural Gas in Abundance

For many years, the coal industry boasted that U.S. reserves were sufficient for 300 years into the future. Today the gas industry boasts its reserves are sufficient to power the country for four centuries or more. That’s for a resource that in the 1970s was thought to be limited and declining so dramatically that it should not be used to generate electricity. That view was enshrined in a 1978 law, the Powerplant and Industrial Fuel Use Act. It banned gas as a fuel for new electric generation, and encouraged coal instead. Congress repealed the act in 1987.

When the shale revolution hit, some gas industry analysts predicted it would be a short-term phenomenon, and shale gas wells would not continue to be productive. At the time, a large fracked gas well could produce 5 million cubic feet/day (MMcf/d). Since then, wells have come in at much greater flow, and old wells have not declined. In August, Chesapeake Energy Corp. reported a well drilled in northeastern Pennsylvania came in at a sustained production rate of 62 MMcf/d.

“The good news is the incredible abundance” of natural gas, Philip Moeller, Edison Electric Institute executive vice president and regulatory guru (Figure 1), told POWER. Moeller was a commissioner at the Federal Energy Regulatory Commission (FERC) and the commission leader on issues related to electric-gas coordination.

|

| 1. Lots of gas, not enough transportation capacity. Philip Moeller is executive vice president of Edison Electric Institute (EEI) and a former commissioner at the Federal Energy Regulatory Commission, where he led the commission on issues of coordination between natural gas and electricity. Courtesy: EEI |

The key issue for electric generators today, he said, is “do we have the transportation capacity” to move the gas to its newly burgeoning market? Inside both industries, the term of art is “deliverability.”

Electric transmission and natural gas transmission are fundamentally different, Moeller noted, which produces some cultural and physical differences. Power moves at the speed of light, while gas moves at about 30 miles per hour. The language between the two industries is different, where the same words mean different things in each industry. This complicates communication.

Chris Ellsworth, a senior market advisor with FERC, told POWER that the cultural differences are often based on historical circumstances, which Moeller also noted. The natural gas pipeline network, which FERC regulates, was largely built to serve local distribution companies (LDCs), primarily residential and commercial customers with heating needs (gas utilities), and industrial customers with a variety of tasks including chemical applications. The gas industry relies on competitive pipeline companies making firm contracts with these large customers.

| The New England Conundrum

In January 2014, a polar vortex event hit the eastern U.S., bringing record low temperatures. New England was hit hardest. Natural gas prices, constrained by the need to serve firm residential and industrial customers first, soared to historic levels—and prices bid into ISO-New England’s (ISO-NE’s) electric energy market followed, resulting in spiking retail electricity prices and public outrage. There was little ISO-NE could do about it. The obvious solution for the long term is to build more pipelines from shale gas fields to New England, and build more gas storage. That has not happened. Major pipeline proposals have crashed against the inability to find anyone to pay for new pipes to the region. Last year, Kinder Morgan canceled a $5 billion New England project when it couldn’t line up customers willing to sign long-term contracts. Then Enbridge shelved a $3.2 billion pipeline project to bring enough gas to power 5,000 MW of generation. Enbridge cited an inability to line up financing in the face of hostility from Massachusetts toward the idea that electric customers should pay for the pipeline. A Massachusetts state court last year ruled against putting the cost of the project into electric distribution rates. The ISO has had to rely on old, inefficient and polluting oil-fired steam plants, burning heavy fuel oil, when temperatures plunge and demand for heat rises. These plants, which make up 23% of total regional generating capacity, run only when gas is supplying its firm customers—local distribution companies and direct industry customers—and doesn’t have spare gas to serve the intermittent electric market. In 2016, with a warm winter, oil made up just 0.5% of the year’s generation. “Fuel has to come from somewhere when the existing pipelines are constrained,” ISO-NE chief Gordon van Welie told POWER. Edison Electric Institute Executive Vice President Philip Moeller recounted that during the polar vortex event, the region saw the highest gas prices in the world for February gas futures. At the same time, 100 miles away in the middle of the Marcellus play, gas futures prices were the lowest in history. “Historically,” said Donald Santa, head of the Interstate Natural Gas Association of America, “the region has been at the end of energy supply lines.” It is densely populated and constrained by environmental politics. “Politically, the region has closed the doors” to new gas pipelines, he said. “The conundrum: who is going to pay for pipeline capacity? Pipes don’t build on speculation.” |

Fundamental Differences

Donald Santa (Figure 2), head of the Interstate Natural Gas Association of America (INGAA), the gas pipeline industry’s Capitol Hill lobbying group, explained the fundamental differences between the two intertwined industries in an interview with POWER in August. “The industries have a different history, culture, and vocabularies,” he said, adding that “the two are operationally different, with different regulatory and commercial models.”

|

| 2. Different history, different culture. Donald Santa is head of the Interstate Natural Gas Association of America (INGAA). He says that while electricity and natural gas markets are linked, “the two are operationally different, with different regulatory and commercial models.” Courtesy: INGAA |

Santa said, “Electricity is an important and growing market for gas pipelines, but not the only one.” Santa, a former FERC commissioner, noted that local gas distribution companies, industrial customers, electric generators, and the growing LNG export market make up the customer base for gas.

The LDCs and industrials remain the largest traditional markets for gas, around which the industry was built. Those traditional customers have predictable demands. The residential demand ramps up in the winter heating season. The industrials know when they need gas well in advance. So the gas industry has concentrated on firm delivery contracts (with some offside interruptible markets).

It’s a remarkably reliable industry. An INGAA survey covering 2006 to 2016 found that pipeline firm-contract customers had their deliveries made 99.79% of the time. “For customers who chose to buy that level of service, delivery was virtually certain,” Santa said.

But electric generators have more variable fuel needs (see sidebar “The New England Conundrum”). They follow electric loads, which are less predictable. “Generators are more variable on their gas take,” said FERC’s Ellsworth. “That can create some issues during periods of congestion. Gas-fired generators tend to be variable, as their load is variable.”

Predictability and Coordination

As gas supplants coal and nuclear as a baseload resource, as well as following load to firm up growing intermittent wind and solar generation, the electric market may become more predictable for gas pipelines.

FERC has encouraged the gas and electric industries, both of which it regulates, to better coordinate with each other. The economic incentives to do so are strong, as both Moeller and Ellsworth observed. The two industries are working through the North American Energy Standards Board to understand and coordinate their cultural and business anomalies. That’s a slow process, as it requires consensus among the parties, but it seems to be working, according to many energy analysts.

“If you compare where we were when this discussion began, five or six years ago,” said Santa, “it was as if we were from different planets.” That has changed, he said, and the two industries are working together to understand each other and coordinate their businesses.

In 2015, FERC tried to align the natural gas and electric operating days so that electric generators would have a better view of their upcoming load when making bids for gas. A FERC proposal would have moved the start of the gas day from 9 a.m. Central time to 4 a.m., but the natural gas industry rose up against that plan. Moeller, who was on the commission at the time and the commission’s lead on gas and electric coordination, said the commission’s proposal accomplished one thing—it completely unified the gas industry in opposition to the proposal.

FERC backed off. A commission press release said the rule it ultimately adopted “recognizes that several regional efforts continue to address the misalignment between the gas day and the regional electric days.”

Santa said that the two industries are cooperating successfully, outside of FERC, on practical matters. “There has been a lot more dialog between the respective sectors,” he said, “on a more practical basis.” He added that his pipeline members meet regularly with their electric customers. INGAA itself holds an annual gathering of pipeline companies and electric regional transmission organizations to discuss cross-industry issues. Santa was wary of further FERC regulatory efforts to foster coordination unless they resulted from the ground up, and from the two industries working together.

|

| 3. Pipeline projects moving forward. This Consumers Energy pipeline project is one of many under construction in the U.S., designed to move natural gas to markets that need it, and to take advantage of the abundance of natural gas production in areas such as the Marcellus Shale. Michigan-based Consumers Energy said it plans to invest about $440 million to upgrade its pipeline system in 2017. Courtesy: Consumers Energy |

Despite the discrepancies that create inefficiencies for generators, the enormity of gas supply has led to a boom in construction of interstate gas pipelines (Figure 3) to move gas from Pennsylvania, West Virginia, and Ohio to markets in the Midwest and South (see sidebar “The Appalachian Pipeline Boom”). That will likely accelerate now that FERC has a quorum of commissioners.

| The Appalachian Pipeline Boom

A recent National Public Radio story identified five large new Appalachian pipeline projects that have Federal Energy Regulatory Commission (FERC) approval. Here’s a quick breakdown of the projects. Rover, approved in February, is a 700-mile pipeline, the largest now under construction in the U.S. It will move 3,250 million cubic feet /day (MMcf/d) from Marcellus and Utica gas wells to delivery points in Ohio, West Virginia, Michigan, and Canada. Operation is scheduled to begin by the end of the year. Northern Access, approved in February, is currently on hold pending litigation after New York denied a water permit in April. The 100-mile pipeline would send 497 MMcf/d from northeastern Pennsylvania to upstate New York. Leach Xpress, approved in January, is under construction. The 161-mile pipeline will move 1,530 MMcf/d from western Pennsylvania, West Virginia, and Ohio to an existing pipeline in Ohio that runs to the Gulf Coast. Atlantic Sunrise, approved in January, has construction underway. It will move 1,700 MMcf/d of Marcellus gas from northeastern Pennsylvania 183 miles south to connect with existing pipelines serving Maryland, Virginia, the Carolinas, Georgia, Alabama, and Florida. Access South/Adair Southwest/Lebanon extension, approved last December, is under construction. It is a 16-mile extension of an existing pipeline to connect Pennsylvania gas to markets in the Midwest and Southeast. Still under review at FERC are six Appalachian pipeline applications, which—along with those that won approval earlier this year—are part of a large group of pipeline proposals from 2015, all aimed at moving Marcellus and Utica shale gas to markets. The following projects are being reviewed. WB Xpress, a 29-mile line from West Virginia, aimed at transporting 1,300 MMcf/d of gas to an existing Virginia pipeline and on to the Cove Point liquefied natural gas export terminal in Maryland. Nexus, a pipeline expected to run 256 miles from Ohio’s Utica fields to Michigan and Canada, with capacity of 1,500 MMcf/d. Mountaineer Xpress, a line with 165 miles entirely in West Virginia running from shale gas resources in the state’s northern panhandle to the southwest, bringing 2,700 MMcf/d to an existing pipeline network. Penn East, a project covering 120 miles from northeastern Pennsylvania to New Jersey, with 1,100 MMcf/d of capacity. Mountain Valley, a 303-mile pipeline from northern West Virginia to southern Virginia, with capacity of 2,000 MMcf/d. Atlantic Coast, a pipeline stretching 600 miles, designed to move 1,500 MMcf/d from northern West Virginia through central Virginia and central North Carolina. |

Opposition to Pipelines Slows Approvals

It has been difficult to get new pipelines approved, particularly in regions where the pipes are not familiar to local citizens. Activists have raised several claims to oppose the projects. Opponents of fracking, which they view as environmentally damaging, have besieged FERC with protests outside and inside the agency, including targeting FERC commissioners’ homes. They have been joined by opponents of natural gas, which is a greenhouse gas and emits carbon dioxide when burned, although significantly less than coal. Their assaults on FERC last year have proven futile but are raising local opposition.

Opponents of gas pipelines have taken their protests to local governments. In Virginia, for example, a major target has been Dominion’s Atlantic Coast project, the largest now pendinERC’s environmental analysis of the project has been incomplete and biased. The pipeline has become an issue in the 2018 Virginia gubernatorial campaign, although there is nothing the state’s governor can do to stop the project once it wins FERC approval.

FERC’s certification of a pipeline application is definitive unless overturned by the courts. Under the 1938 Natural Gas Act, once the commission gives a green light to a pipeline project, the developers can use federal eminent domain to overcome local opposition to the project. Under the 1969 National Environmental Policy Act, FERC must conduct a fairly rigorous environmental analysis of the proposed project before it can approve the pipeline.

Opponents of the new pipeline projects claim that FERC is in thrall to pipeline interests, noting that the commission has turned down applications for pipeline approvals only twice in 30 years. A National Public Radio (NPR) story on the gas pipeline construction boom quoted a retired utility employee: “They don’t seem to pay attention to opponents.”

INGAA’s Santa observed that new pipeline projects have long generated controversy. The 1980s Iroquois Pipeline to bring gas from Canada to the Northeast created a storm of local opposition to FERC, which ultimately approved the project.

Increased production of shale gas means pipeline companies are proposing to build new pipes in areas that haven’t previously had a lot of energy infrastructure, arousing local landowner opposition. The new pipes also tend to be located in areas with greater population density than earlier projects, which generally moved gas from the Southwest.

There is an added element to the pipeline opposition, said Santa. “Opposition based on ideology is something new,” he said, noting the rise of groups opposing anything that looks like a fossil fuel on the grounds of combating global warming. Social media has also made it easier to organize opposition to infrastructure of any kind.“

Opponents are prone to litigate,” said Santa. That puts a “real premium” on making sure the pipeline proposals at FERC are airtight, and the FERC orders granting certificates have no holes. Former FERC chairman Jon Wellinghoff told NPR that FERC “has to stay within the tracks” on pipeline applications. Santa told NPR that projects are so expensive that sponsors have to take major steps to assure that FERC won’t reject them.

FERC was out of business, without a quorum, for six months starting in February 2017, but is now able to make major orders, including pipeline certificates. In late August, three commissioners were in place, with two more in the Senate confirmation process, expected to receive approval.

That doesn’t mean the agency will quickly sign off on the pending major pipes from shale country. Santa said he was sure the commissioners understand the “imperative to deal with the backlog.” But they also need time to hire staff, do an enormous amount of reading, and get up to speed with the agency’s procedures and agenda. Based on his experience, Santa said, “Being a new commissioner is like drinking from a fire hose.” ■

—Kennedy Maize is a long-time energy journalist and frequent contributor to POWER.