Competitive generation giant Constellation Energy has agreed to sell approximately 4.4 GW of natural gas–fired generation capacity in PJM Interconnection to LS Power Equity Advisors for $5 billion, marking the largest single tranche of divestitures required to resolve antitrust and market-power concerns arising from Constellation’s $26.6 billion acquisition of Calpine Corporation.

The deal, announced on March 18, will transfer five facilities in Delaware and Pennsylvania to LS Power at an acquisition price of approximately $1,142/kW. Closing, expected later this year, remains contingent on secondary review by both the Department of Justice (DOJ) and the Federal Energy Regulatory Commission (FERC).

The five facilities poised to transfer to LS Power are a mix of modern combined-cycle high-efficiency generation and older simple-cycle peaking capacity, all of which operate within the PJM Mid-Atlantic zone:

- Bethlehem Energy Center. A 1,134-MW gas-fired combined-cycle plant in Bethlehem, Pennsylvania, which was commissioned in 2003.

- Hay Road Energy Center. A 1,136-MW dual-fuel combined-cycle plant near Wilmington, Delaware, whose units were commissioned between 1989 and 2002, and is capable of running on natural gas or low-sulfur diesel.

- York Energy Center Unit 1. A 569-MW dual-fuel combined-cycle plant in Peach Bottom Township, Pennsylvania, which was completed in 2011.

- York Energy Center Unit 2. An 828-MW combined-cycle plant at the same Peach Bottom Township site as Unit 1. The combined York complex has a combined capacity of about 1,397 MW.

- Edge Moor Energy Center. A 707-MW simple-cycle plant near Wilmington, Delaware, originally commissioned in 1954 and subsequently converted from coal to natural gas and oil. The plant is the oldest and most dispatch-limited asset in the portfolio.

“This transaction is an important step in satisfying the DOJ’s requirements and advancing our path forward,” said Joe Dominguez, president and CEO of Constellation on Wednesday. “These are well-run facilities that will continue powering consumers and businesses for decades to come. We’re pleased to be moving ahead and expect to complete the remaining DOJ requirements later this year.”

Why Did Regulators Require Divestitures?

Constellation announced its agreement to acquire Calpine on Jan. 10, 2025, in a cash-and-stock transaction valued at an equity purchase price of approximately $16.4 billion—or $26.6 billion inclusive of Calpine’s approximately $12.7 billion in net debt assumed at closing. As POWER first reported, the deal sought to combine Constellation’s 22-GW nuclear fleet—the largest in the nation—with Calpine’s roughly 26-GW gas-fired and geothermal portfolio to create a combined generation footprint approaching 60 GW across nuclear, natural gas, geothermal, hydro, wind, and solar. The transaction required clearance from FERC, the DOJ, the New York Public Service Commission, the Public Utility Commission of Texas, the Canadian Competition Bureau, and other regulatory agencies.

While FERC approved the transaction on July 23, 2025, the regulatory body conditioned on the divestiture of four specific PJM assets—Hay Road, Edge Moor, Bethlehem, and York 1 —on the basis that Constellation’s post-merger market share in the Mid-Atlantic zone raised horizontal market-power concerns. Specifically, FERC determined that the merger would trigger market-power screen failures in PJM submarkets such as PJM East and 5004/5005, indicating that the combined entity’s overlapping generation could increase concentration and harm competition without structural mitigation. PJM submarkets such as PJM East and 5004/5005 are constrained transmission zones within the broader PJM market that can function as localized markets when transmission limits restrict power flows.

However, the DOJ’s Antitrust Division, acting alongside the attorney general of Texas, subsequently filed a civil antitrust complaint and proposed consent decree on Dec. 5, 2025. The measure was notably the first structural relief the division had sought in a generation-sector merger in nearly 15 years. Citing concerns that the merger would reduce competition between Constellation and Calpine’s gas-fired fleets and enable price increases, the DOJ’s divestiture list extended beyond FERC’s four-plant requirement to add Calpine-owned assets, including the 828-MW York 2 facility in Pennsylvania, the 605-MW combined-cycle Jack Fusco Energy Center near Houston, and a minority ownership stake in the 385-MW combined-cycle Gregory Power Plant near Corpus Christi, Texas.

Constellation closed the Calpine acquisition on Jan. 7, 2026—ahead of the originally anticipated mid-2025 to early-2026 window—creating what the company describes as the world’s largest private-sector power producer. The combined entity holds 55 GW of capacity, about 5 GW below the roughly 60 GW projected at announcement, reflecting required divestitures that reduced the net combined fleet. Constellation sold its minority stake in the 385-MW gas-fired Gregory Power Plant in Texas earlier this year, which leaves the 606-MW gas-fired Jack Fusco Energy Center in Texas as the only remaining asset to be divested under the DOJ consent decree.

The March 18 agreement to sell the five PJM facilities to LS Power for $5 billion “represents the largest and most substantive element of the DOJ and FERC resolutions,” Constellation said on Wednesday. However, before the transaction can close, two regulatory actions remain: The DOJ must clear the asset transfer under the terms of the existing consent decree, and FERC must separately approve the change in ownership of the jurisdictional facilities. Constellation has suggested it expects to complete the remaining DOJ requirements—potentially including the Fusco divestiture—before year-end 2026.

What This Means for Market Structure

Constellation’s combined entity, integrating Calpine’s assets, now holds approximately 55 GW of capacity across nuclear, natural gas, geothermal, hydro, wind, and solar. In PJM, Constellation held approximately 20 GW before the deal closed. Calpine contributed more than 5 GW across 14 PJM plants, according to the DOJ’s Competitive Impact Statement filed Dec. 12, 2025, in the U.S. District Court for the District of Columbia. In the Electric Reliability Council of Texas (ERCOT), Calpine added approximately 9 GW to Constellation’s existing 5 GW footprint—making the combined company the dominant private generator in Texas and the third-largest supplier in that market by capacity before divestitures.

The divestiture requirement, notably, stemmed directly from the competitive concentration that the combination created in two specific wholesale markets. The DOJ identified two relevant geographic markets as the locus of anticompetitive harm: ERCOT and the PJM Coastal Mid-Atlantic area, a transmission-constrained subregion encompassing southeastern Pennsylvania, New Jersey, Delaware, and the eastern shores of Maryland and Virginia, bounded to the west by the Nottingham transmission constraint near the Maryland-Pennsylvania border.

The DOJ argued that Constellation’s combination of low-cost nuclear baseload—which generates consistent revenues at prices below the market-clearing price—would create a direct financial incentive to withhold higher-cost mid-merit and peaking units from PJM’s day-ahead and real-time energy auctions, forcing the market to accept higher-priced substitute offers and raising the clearing price across all dispatched units. In ERCOT, post-merger Constellation would control more than 12% of total generating capacity and over 20% of the natural gas generation that most frequently sets the market-clearing price in Texas, the DOJ alleged.

LS Power’s Strategic Rationale

For LS Power, a family- and employee-owned development, investment, and operating company founded in 1990, the Constellation deal marks a substantial boost to its portfolio. The New York–based energy infrastructure company says it has developed or acquired more than 50,000 MW across more than 200 projects and raised more than $77 billion in debt and equity capital for North American infrastructure in a platform that spans natural gas, solar, wind, hydroelectric, battery storage, and transmission assets.

The firm operates through three primary business lines: LS Power Development, which advances new generation and transmission projects; LS Power Generation, which operates a portfolio of 22.4 GW; and LS Power Equity Advisors, the investment vehicle named as the acquirer in the Constellation transaction.

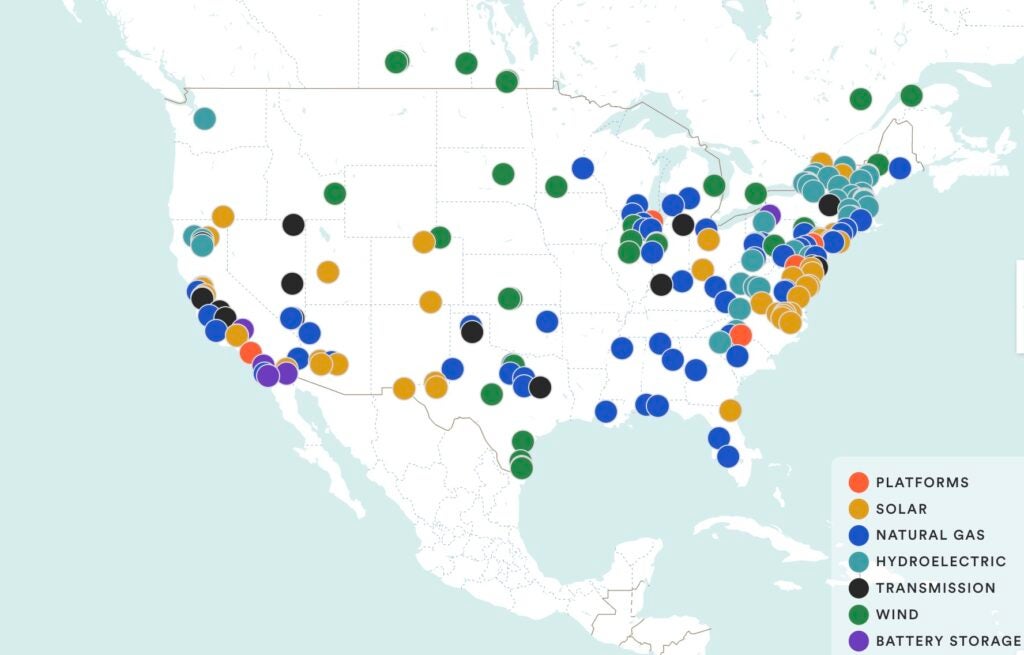

LS Power’s North American portfolio as of March 2026 spans natural gas, solar, wind, hydroelectric, battery storage, and transmission assets across more than 200 projects. The firm’s concentration of natural gas capacity in the PJM Mid-Atlantic corridor is visible in the dense clustering of blue dots along the Eastern Seaboard. Courtesy: LS Power

Less than two months before the March 18 announcement, LS Power completed the $13 billion sale of 13 GW of its gas-fired generation fleet and its CPower demand response platform to NRG Energy on Jan. 30, 2026. The transaction announced in May 2025 received DOJ antitrust clearance on Jan. 23, 2026, and FERC approval in November 2025.

The company, notably, has a long track record of repositioning ahead of anticipated market cycles. Between 1990 and 2001, LS Power built and sold nine gas-fired plants, exiting before what it describes on its website as an anticipated overbuild of gas generation. In 2003, it pivoted to distressed asset management, launched its private equity platform in 2005, expanded into high-voltage transmission in 2006, pioneered utility-scale battery storage in 2016—its 250-MW Gateway Energy Storage project in San Diego was the world’s largest battery at energization in August 2020—and in 2024 consolidated its gas assets into Lightning Power, an approximately 11-GW independent power producer, before selling the bulk of that fleet to NRG in January 2026.

In a January 2026 interview published on lspower.com, LS Power COO Darpan Kapadia suggested that market economics may be a key driver of that strategy, highlighting the widening gap between the cost of new-build generation and that of existing assets. “The last gas power plant we developed, which reached commercial operations in 2014, cost $900/kW,” he said, noting that “today’s estimates range from $2,200–3,000/kW.” Even under favorable conditions, “the earliest we could be energized and delivering electrons…is late 2030 or early 2031.” The five Constellation assets—poised to be acquired at approximately $1,142/kW—may offer a significant discount to replacement cost. “Operating gas generation assets that can be purchased at a discount to these levels will have a significant moat,” Kapadia said.

Kapadia also pointed to the sharp surge in demand. “Over the last 12 months, electricity demand in the MidAtlantic/PJM market has grown by over 3% and in ERCOT/Texas it’s grown by over 4.5%,” he said, adding that “after more than 20 years of near-zero load growth, that’s a pretty big deal.”

On Wednesday, LS Power CEO Paul Segal reiterated the portfolio’s strategic value amid rising demand. “PJM is at the epicenter of the surge in electricity demand, and these are exactly the kind of assets the grid needs—efficient, dispatchable gas generation that can deliver reliable power around the clock,” he said. “LS Power has been developing, building, and operating gas-fired generation for over 35 years. We expect our extensive operational experience will enable seamless integration of the assets and their employees and look forward to engaging with plant staff and the local communities around the facilities.”

—Sonal C. Patel is a POWER senior editor (@sonalcpatel, @POWERmagazine).