By Kennedy Maize

Washington, D.C., June 12, 2012 – It’s hard to cry the blues for a union worker at a nuclear power plant making $122,000 a year with a good health plan and a solid 401(k). That’s the situation of the average striking (or locked out, if you will) member of Local 369 of the Utility Workers of America at Entergy’s Pilgrim nuclear plant outside Boston.

These workers have it pretty good. And I’m in no position to judge the validity of the competing claims their union and the plant’s New Orleans-based owner make over the righteousness of the lockout (or strike, if you will). I haven’t read the collective bargaining agreement, so I know very little about the details of the Pilgrim work rules. But in some ways, I’m reminded of the commonplace reaction when professional athletes strike: it’s millionaires versus billionaires. Boo hoo hoo!

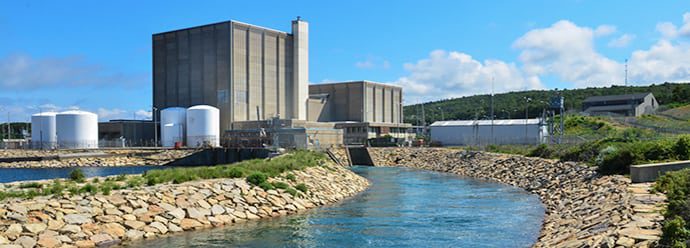

On the other hand, I shed no tears for the owners of a major generating asset who have just been handed a money-printing machine by the U.S. Nuclear Regulatory Commission in the form of a 20-year extension of the original 40-year license to operate an old, outmoded and (some would argue) less-than-safe reactor design. Pilgrim is, after all, built around a General Electric boiling water reactor with a Mark 1 pressure-suppression containment, a variant of the Fukushima Daiichi units that melted down in early 2011.

Nuclear plants have quite low O&M costs, given the inherently low costs of fuel. This plant was surely fully depreciated long ago, and is carrying either no capital costs or costs of money that are insignificant. Correctly, such economic calculations carry no weight in the NRC’s decision about whether the plant is safe enough to continue to operate for another 20 (or 20 more beyond that?) years. But there can be no doubt that Entergy financial types had visions of waterfalls of dollars flowing their way when they ran the relicensing numbers for the plant five or more years ago.

Let’s be clear: Entergy is not reaping the fruits of a risky and expensive investment made over 40 years ago to build the 670-MW generating unit (subsequently uprated to 685-MW). That was Boston Edison, a utility that has long-since become an operating unit of the NSTAR distribution utility). Entergy bought Pilgrim from Boston Edison in 1998, during the sell-off by utilities divesting radioactive only child generation during the era of restructuring.

And “bought” isn’t quite the right word to describe Entergy’s acquisition of Pilgrim. As the New York Times reported in 1998, Entergy’s successful bid for the plant was $80 million, of which $67 million represented the value of the plant’s inventory of nuclear fuel. So Entergy paid $13 million, $20/KW, for the plant’s capacity at a time when a gas-fired or coal-fired plant was running at $500-$1000/KW. Not a bad deal.

But wait, there’s more. What the paper did not report – but what I recall from writing about the sale for Electricity Daily at the time – was that the sale included Pilgrim’s decommissioning fund. That meant that Entergy got access to several hundred millions of dollars that it could invest to its own benefit as part of the sale. So, one can argue that Boston Edison paid Entergy to take the nuclear plant off its hands. It was a gift, not a sale.

Sweet. And no wonder the plant workers want a bigger piece of the pie. It’s a mighty big, mighty tasty pie, now that the plant has another 20 years to print money at very little (or no) risk to Entergy.