An essential ingredient in the success of any business endeavor is thorough planning. We’ve all heard the axiom "proper prior planning prevents poor performance" or a variation on that theme. Why the need for peak performance? Competition within the industry has never been as intense, with utilities combining in search of economies of scale. The need for competitiveness aside, there’s a fundamental truth in our business that should figure prominently in the planning of every power generator—regardless of size or region: Your plants and people are getting older by the day.

Rocking in the dark?

The energy utility sector is seriously threatened by a serious manpower shortage expected as soon as the end of this decade. The Philadelphia-based consulting firm Hay Group recently projected in a report that 40% of senior electrical engineers and 43% of shift supervisors working for natural gas and electric utility companies will be eligible for retirement by 2009. Yet more than two-thirds of firms surveyed have no succession plan for supervisors, and 44% have no plan for vice-presidents.

"The electric and gas industries could easily collapse if they don’t put a plan in place for staffing, retention, recruitment, and training," said Mike Brown, senior consultant and utilities sector leader for Hay Group. "We need to seriously question if we will be able to keep the lights on in the next 10 years."

The Hay Group report also predicts that 40% to 50% of all utility employees will be retiring in the next three to four years. If that proves true, the timing couldn’t be worse, given America’s urgent need to expand and upgrade its utility infrastructure of pipelines, power plants, transmission lines, and other facilities. Completing the double whammy is the report’s finding that fewer young people are choosing energy as a career, because deregulation, downsizing, and consolidation have tarnished the industry’s traditional reputation for job security. Engineers and techs have options, and they’re voting with their feet.

Baby Boomers are now handing the reins to Generation X, along with the opportunity to move into the executive ranks. But manpower shortages exist at both the entry and executive levels. Apropos of that, Brown noted that "Utilities have invested historically next to nothing in their officers." For that reason, he explained, "People are reluctant to take managerial positions. They don’t need the grief, and they don’t need to make any more money."

White and blue collar

Universities, realizing that fewer students are interested in pursuing a career in the generation industry, in many cases downsized or eliminated their engineering tracks in favor of computer science, "especially during the dot-com era," Brown said. "We used to graduate 2,000 power engineers a year," he added. "Now we’re at 500 a year. But we could probably use about 100 per state now."

In Brown’s opinion, many young people are unwilling to put in the effort that an engineering program requires. "I call them the Millennium Generation, born after 1980," he said. "Where the Baby Boomers believed that if you worked hard, your rewards would come in time, the next generation seems to value quality of life more than money."

Utility regulators are also facing the same mass employee exodus. The Nuclear Regulatory Commission (NRC), in particular, is preparing for a giant wave of retirements soon; nearly half of its staffers are at least 50, and 36% will be eligible to retire in the next five years. Bad timing again, just as the agency prepares to implement a new licensing regime and decide whether to go forward with the Yucca Mountain repository. The potential loss of a critical mass of technical staffers and their historical knowledge has generated concern at the agency’s highest level.

Plant managers and NRC commissioners may not have to deal with what has been dubbed the "tsunami effect" alone. Two years ago, the Utility Business Education Coalition (UBEC)—an alliance of gas and electric utilities keen on workforce development—established the Utility Workforce Planning Network to solve a single problem: the dearth of entry-level hires in energy. Among the UBEC’s tactics is fostering communication among local utilities and high schools, community colleges, and economic groups in their territory. UBEC was formed about 10 years ago to address two specific issues: a potential employee shortage and the need to attract skilled workers to the industry.

"We’ve found that the aging of the workforce is a reality that had been masked by deregulation-based downsizing and the introduction of technology and new work practices," said Steve Kussman, executive director of UBEC. With an employee pool that has shrunk by about 25% and has virtually no turnover, "We learned that [the energy utility industry has] just about the oldest workforce out there. The two critical job areas that continue to need the most attention are skilled and craft labor at the first level and the first-line supervisory level," Kussman explained.

Early bird

For an example of how to deal with the tsunami effect, consider that Akron-based First Energy is preparing for what may be its largest mass hiring in several decades. Its workforce’s average age is 48 years, so FirstEnergy needs to replace a host of highly skilled and experienced employees who are expected to retire over the next few years. During this year and next, about 745 positions are expected to become available in energy delivery, 575 in power plants and support services, and 280 in corporate and service areas. The "now hiring" sign has been posted for engineers, business analysts, finance types, dispatchers, IT specialists, administrators, and line and technical workers.

The company is prudently acting now to ensure that new employees will benefit from working side-by-side—at least for a while—with existing, experienced staff. A corporate spokesman said management expects to reap huge dividends from its early planning for a systematic transfer of knowledge and from expanding mentoring and on-the-job training programs already in place. To grasp the enormity of FirstEnergy’s task, realize that by the end of next year nearly 25% of FirstEnergy’s 13,000 employees in Ohio, Pennsylvania, and New Jersey may be new hires.

Supply shortage

The aging utility workforce challenge also faces universities, the incubators of new utility engineers. U.S. academia has become increasingly dependent on foreign student enrollment in engineering and science programs. About half of all students pursuing advanced degrees in engineering, math, and computer science aren’t U.S. citizens, and nearly 70% of postdoctoral researchers in engineering and physical sciences are foreign-born. Complicating the problem, faculty members are getting up in years themselves; about 30% of science and engineering professors qualify for AARP membership. What’s wrong with the first part of this picture? Most foreign students return home after getting their degrees.

One set of statistics may be open to question, but it’s hard to dismiss several, including these two, that point to the same trend:

- In 1975 there were 77 nuclear engineering programs in U.S. universities. Today, the web site of the engineering program accrediting organization ABET lists only 18 accredited programs leading to a BS degree in nuclear engineering. A sign of the fallout from this implosion: Since the mid-1980s, the number of university research reactors has fallen by about half.

- According to the American Society for Engineering Education, U.S. universities award about 70,000 engineering degrees annually—while 191 American Bar Association-approved law schools graduate 43,000 attorneys. Could the U.S. economy’s continuing shift from manufacturing (what utilities really do) to service be any clearer?

Plants age, too

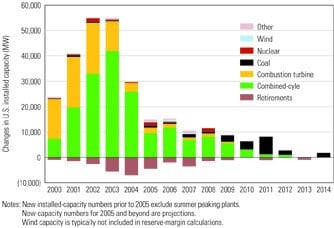

The U.S. fleet of baseload steam power plants may be aging, but they’re hardly ready to be put out to pasture. On the contrary, the country’s dependence on older units has never been greater. About 30% of the power generated by American utilities comes from plants built more than 30 years ago, with a few still going strong after 50. That these oldies but goodies remain vigorous is a testament to the experience and strong O&M practices of the current workforce. Keeping the plants vital for as long as possible is an imperative for the next generation of utility engineers and technicians (Figure 1).

1. Coming and going. U.S. capacity additions and subtractions by in-service year and plant type. Source: North American Electric Reliability Council

The need to extend plant life is a consequence of the disjointed U.S. regulatory and business environment. In some regions, independent system operator (ISO) reliability-must-run (RMR) requirements force plant owners to operate units well past their prime. In others, RMR contracts—which provide cost-of-service rates to power plants in deregulated states—have encouraged investment in new capacity by pumping up expectations of high spot-market prices. However, the fact that inefficient plants, as higher-cost producers, may not be dispatched often enough to recover even their fuel costs does tend to put prospective investors off. Mandated spending on new environmental control equipment is another deterrent.

Problems from the East Coast . . .

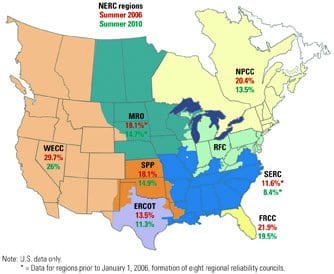

Because market forces and regulatory climates differ by state and region, there is no one-size-fits-all way to guarantee that supply and demand will be matched over the short or long term. In New England, for example, about 7,000 MW of capacity now is either operating as must-run or seeking Federal Energy Regulatory Commission (FERC) approval to do so. FERC has been approving the must-run payments to keep plants in service that are needed to maintain regional reserve margins (Figure 2).

2. Enough to go around. Reserve margins by North American Electric Reliability Council (NERC) region. Source: North American Electric Reliability Council

Utilities and consumer advocates say that the must-run agreements—by distorting free markets—are further driving up New England’s retail electricity prices, traditionally among the highest in the country. Plant owners, they argue, must suffer the slaps of the market’s "invisible hand" during hard times to deserve its blessing when sales are strong. In response, plant owners warn that, without RMR contracts, they may not remain in business long enough to help avert a potential regional capacity shortfall in 2008.

The proliferation of must-run contracts in New England underscores the complexity and connectedness of problems plaguing the power industry. Owners of aging plants say the stream of expensive retrofit mandates coming from FERC and local regulators makes them question whether extending a plant’s life is worth it. But with little new capacity on the horizon, transmission bottlenecks leaving grids vulnerable to reliability problems, and environmental concerns at a fever pitch, public overseers of electricity markets have no choice but to be heavy-handed.

For investor-owned utilities (IOUs), resource adequacy requirements and RMR contracts allow them to extend the useful lives of assets that would otherwise be ripe for retirement. However, for both IOUs and regulators, the challenge is to decide whether relying on so many older, less-reliable plants makes better economic sense than investing in new, gas-fired capacity. As Calpine’s recent bankruptcy proves, putting too many eggs in the natural gas basket may not be a prudent strategy either, given continuing and rising gas price volatility.

Massachusetts’ municipal utilities are urging FERC to take a fresh look at proliferating RMR contracts. Massachusetts Municipal Wholesale Electric Co. (MMWEC), which provides services to this group of munis, has asked the agency to deny an application for must-run status filed by Boston Generating LLC’s 1,658-MW Mystic Units 8 and 9. Munis serving the cities of Concord, Reading, and Wellesley also oppose the proposed RMR contracts. According to MMWEC, the contracts amount to "customer-funded life support."

A system analysis conducted by the New England ISO in December 2004 found that the Mystic units were essential to grid reliability in the Greater Boston area for two reasons: No substantial upgrades have been made to the local grid in recent years, and electricity use has continued to grow. Contributing more heat than light to the debate, MMWEC has told FERC that a must-run agreement for the Mystic plants would amount to a "$238 million a year consumer bailout. [The plants’] troubled history raises the possibility that the RMR payments sought by Mystic [would cover] imprudent costs that have never been subject to regulatory scrutiny," MMWEC said. Only one outcome of this impasse is certain: Ratepayers will foot the bill.

. . . to the West Coast

California’s electricity system has "critical needs requiring swift and decisive action," states the 2005 Integrated Energy Policy Report of the California Energy Commission (CEC). The report constructs a bleak mosaic of rapidly growing population, annual demand growth of 1,000 MW, skyrocketing wholesale electricity prices ($20/MWh in 2001 and $50/MWh today), potential supply shortages, and an inadequate and aging delivery infrastructure.

Of the 13,000 MW of new capacity that has came on-line in the Golden State since 1998, most took the form of gas-fired combined-cycle plants designed to run at high load factors. The trend continued until recently, with 11 permits for gas-burning plants issued over the past two years. However, new applications have since slowed to a trickle, and caution is the order of the day. Owners of 7,300 MW of new capacity that has been permitted say they won’t break ground without a signed power-purchase agreement (PPA) in hand to facilitate financing.

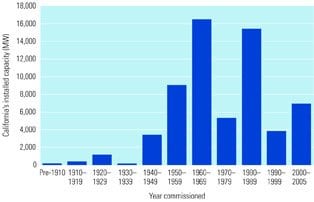

In California a recent shift in electricity usage patterns has confounded resource planners: Peak demand has increased, creating a load-management problem. As you surely know, combined-cycle plants are less able to ramp up or down quickly to meet peak demand than steam plants, which still dominate the state’s fleet. But sooner or later, the age of those steam plants (Figure 3) will have to be dealt with. Of California’s 971 power plants (with a cumulative nameplate capacity of 53,000 MW), 181 (representing 49% of that capacity) are over 30 and therefore cannot be trusted. Moving into middle age are another 128 plants representing 32% of the state’s supply.

3. Too pooped to pop? The age of California’s power plants. Source: California Energy Commission

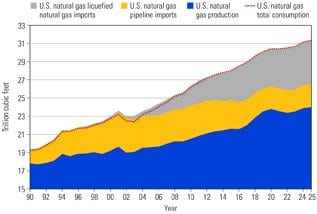

The retirement of old, uneconomic plants is as much of a nationwide problem for resource planners as aging workforces are for utilities. But reserve margins in California may soon grow thinner than those of other states. Planners warn that the state could face severe power shortages within a few years unless Sacramento steps up efforts to secure adequate supplies from within or beyond California’ borders. With the benefit of 20/20 hindsight, the increased share of natural gas used for power generation in California (from 30% in 1999 to 41% in 2004) must be considered a mistake, because it has left the state more vulnerable to shortages of gas supplies (Figure 4). Even if imports of liquefied natural gas (LNG) fill future gaps, there’s no assurance that LNG prices won’t be manipulated OPEC-style by foreign cartels.

4. Got gas? U.S. natural gas supply and demand history and projections. Source: U.S. Energy Information Administration

Perversely, with $9/mmBtu natural gas representing a much larger share of combined-cycle plants’ operating costs, and given the inability of gas futures markets to hedge prices beyond two years, gas price volatility makes developing a new plant a crap shoot—unless a power purchase agreement (PPA) is in hand. Exacerbating the problem, RMR contracts that keep legacy plants alive only serve to push construction of new, more-efficient capacity further into the future (Figure 5).

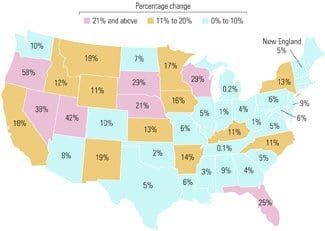

5. All power plants are local. Projected U.S. new capacity additions from 2005 to 2014, as a percentage of 2004 installed capacity. Source: NERC

Being sanguine about this situation isn’t easy, but it’s not impossible, either. Case in point: In California, about 11,000 MW of Department of Water Resources PPAs will expire between 2009 and 2011 and another 6,000 MW by 2016. An optimist might consider these deadlines for finding replacement capacity a chance to make the state less reliant on older, inefficient plants and more reliant on new generating units featuring advanced technologies. At times like these, it’s worth remembering that in Mandarin, the word for "crisis" combines two characters: one meaning "danger" and the other representing "opportunity."