The small modular reactor (SMR) concept has long been viewed by many within the nuclear sector and by policymakers as somewhat of an arriviste—an upstart with bold promises but lacking credibility and a track record.

SMRs were touted to save the nuclear industry from its original sins of delays and cost overruns, typical for all large infrastructure projects regardless of the sector, by offering smaller, more economical, and flexible nuclear power solutions. Yet for nearly two decades, it was still “just a concept” based on the assumption that the good old modularization principle, which has worked remarkably well in many comparable sectors, would work for nuclear energy too. Without operational examples, however, all these were often seen as overly optimistic or speculative.

The world’s first SMR-based facility, Russia’s floating nuclear power plant Akademik Lomonosov, launched in 2019 and deployed in the Arctic, remains, so far, the only project that has reached the stage of commercial operation. Out of more than 100 SMR designs that have been reported over the last 20 years as being developed at various stages, about half have been scrapped, shelved, or put on hold. As the nuclear industry as a whole struggled to be accepted as sustainable and competitive, most SMR start-ups were mainly waiting in the wings.

A Change of Fortune

It wouldn’t be an exaggeration to say that 2023 witnessed a sea change. Nuclear energy has finally staged a powerful—though long overdue—comeback. At the COP28 conference in Dubai, 22 countries, including the U.S., UK, Japan, South Korea, and France, signed a declaration that recognizes “the key role of nuclear energy in achieving global net-zero” and pledged to triple their nuclear capacity by 2050. The measure indicates an emerging global consensus on the critical role of nuclear power in energy transition. The declaration includes a specific commitment to “small modular and other advanced reactors” and promises to support their development and construction.

In Brussels, nuclear energy seems no longer perceived as “controversial.” The European Parliament, which was long split over the recognition of nuclear as “green” or “sustainable” in the EU investment taxonomy, on Dec. 12, 2023, in a landmark move approved by a wide margin (409 votes in favor versus only 173 against) to support the deployment of SMRs across Europe. The European Commission has declared its commitment to maintaining “European technological and industrial leadership in nuclear” and offered its support to a newly formed European SMR-focused industrial alliance.

Governments across the world, along with private investors—from Bill Gates and OpenAI’s Sam Altman to retail investors—are queueing for “hot” SMR start-ups’ shares ahead of their public offerings and are now pouring billions into the sector.

Against this backdrop, the New Nuclear Watch Institute, a London-based think tank founded in 2014, has published a report, “Scaling Success: Navigating the Future of Small Modular Reactors in Competitive Global Low Carbon Energy Markets,” which carefully assesses the prospects of the global SMRs buildout through 2050.

Starting Small, Growing Big

According to the NNWI’s base-case scenario, the total installed capacity of the global SMR fleet by the middle of the century would be in the region of 150 to 170 GW(e). About one-third of that growth would be in the U.S. and Canada, almost a quarter in China, and another quarter in the emerging markets of Africa, Asia, and Latin America.

The report highlights that SMR deployment may face challenges within the sector among different SMR designs (competing for specific market segments depending mainly on size and co-generation options). However, it may also face external challenges from alternative low-carbon energy sources, such as utility-scale energy storage, advanced geothermal technologies in some places in the world, and carbon capture utilization and storage, which are also advancing towards full-fledged commercialization. Large reactor segments also pose competition.

Under such circumstances, rapid scaling is crucial for successful projects to leverage the economies of modularization and series deployment. The effort will cater to cost reductions in a limited and fragmented market, which will likely be dominated by first movers.

The report examines several dozen SMR designs that are under development worldwide. It identifies 25 “higher viability” designs, based on a set of comprehensive criteria that includes technology maturity, licensing progress, business model viability, supply chain readiness, economic competitiveness, market potential, spent fuel and waste management, fuel cycle and supply, financial backing and state support mechanisms, and potential market cluster size and competition within respective clusters.

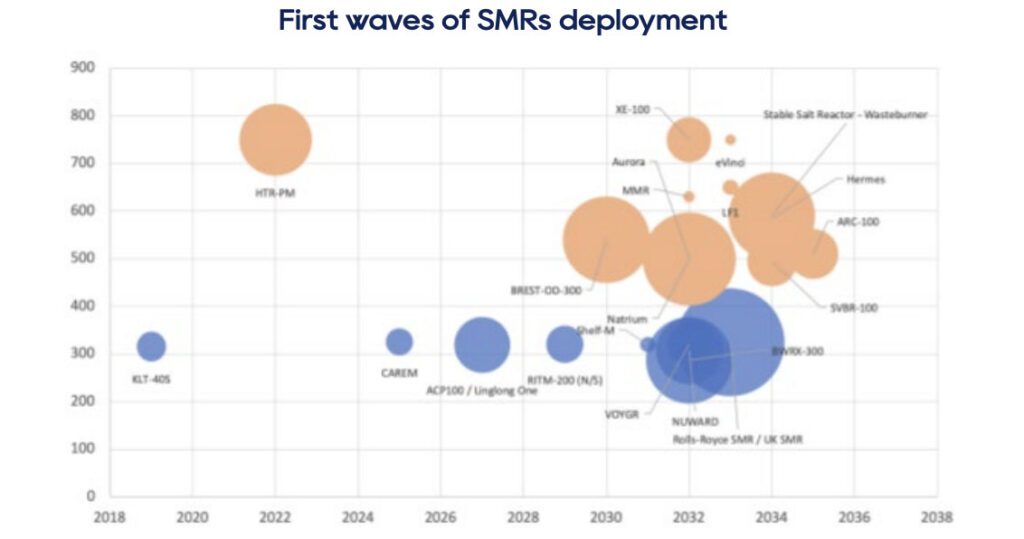

the relatively latest stages of development, in terms of their most likely (base-case scenario) timing of deployment.” Source: NNWI/Rohunsingh et all, 2023

The 25 shortlisted designs are then grouped into categories such as “first movers and front-runners,” “niche projects,” “high-risk potential disruptors,” and so on. The front-runner group includes five designs at the most advanced stages of development and deployment, which are likely to capitalize on available institutional and financial backing to scale up first, reduce costs due to the economies of the learning curve and series deployment, and secure the largest shares of the global market by 2050.

The group includes Rosatom’s RITM-200, China National Nuclear Corp.’s (CNNC’s) ACP-100/Linglong One, NuScale’s VOYGR, GE Hitachi’s BWRX-300, and X-Energy’s XE-100. The following is a brief discussion of the merits and challenges that each of the front-runners faces.

RITM-200 (Rosatom, Russia)

The Russian RITM series currently includes the RITM-200 and RITM-400 for icebreakers; the RITM-200S, RITM-200M, and RITM-400M for floating power plants; and the RITM-200N for onshore nuclear plants. The RITM series leverages an integrated “plant-as-a-service”—essentially a“one-stop-shop” business model that is expected to dominate the global SMR market’s off-grid segment. Owing to comprehensive state support (including funds allocated to the Arctic and the Northern Sea Route development program for a new nuclear icebreakers fleet and SMR-based floating nuclear power plants), Rosatom has now effectively reached the stage of series SMR manufacturing. So far, eight RITM-200 have already been manufactured and installed on icebreakers and six more are currently being manufactured for naval applications. Six others are planned to be deployed as new floating power plants, along with two more for a land-based plant in Yakutia. By 2030, Rosatom is expected to have 16 to 22 operational RITM reactors—a total of about 900-1200 MWe of capacity.

Unlike most SMRs based on pressurized water reactor (PWR) designs, the RITM is designed to use nuclear fuel utilizing high-assay low-enriched uranium (HALEU), which is nuclear material enriched to less than 20%. For now, Rosatom remains the world’s only commercial HALEU vendor, and it fully controls a fuel supply chain.

RITM fuel assemblies use enhanced, accident-tolerant, nickel-chrome alloy rod cladding featuring an energy content per rod of 8 to 11 (for RITM-200M) TWh. The fuel enables the reactor to have much higher maneuverability compared to average PWR performance, with the speed of the change of output at 6% nominal per minute, extending the length of time between refueling to 6-7 years (compared with the average of 2-3 years). It also improves the burnup rate to 109.5 GWd/t U. These features ensure application versatility, both in on-grid (load-following) and off-grid (including remote locations) contexts, and a higher capacity factor (up to 98% availability), which translates into lower levelized cost of electricity (LCOE).

Leveraging its first-mover advantage, the RITM-200 is the first design expected to reach the stage at which the learning curve would bring the target price down to about $50-60 by the mid-2030s. This effectively means price parity with unsubsidized coal power generation and existing large nuclear plants.

Rosatom is also set to benefit from a virtually “closed” (“everything in-house”) supply chain for its SMR, critical for rapid scaling in the face of supply chain imbalances. Although geopolitical fragmentation would bar Russian SMRs from virtually all markets in Organisation for Economic Co-operation and Development (OECD) member countries, Rosatom is likely to extend its dominance in the large reactors sector (with a market share of over 80% in exporting new nuclear builds) to the SMR sector as well, mainly in the emerging markets of the Global South and its domestic market. Rosatom’s RITM series is expected to capture about 17–18% of the global fleet’s capacity by 2025.

ACP-100/Linglong One (CNNC, China)

China’s ACP-100, or Linglong One, is a versatile PWR with a capacity of 310 MWth (125MWe) designed for land and floating platforms and various co-generation applications, including district heating (300th/h hot steam + 62.5 MWe in co-generation mode). Linglong One, including ACP100S designed for floating nuclear power plants, is expected to follow closely, capturing 15-16% of the global fleet in 2050.

The Linglong One is set to be the first onshore SMR in commercial operation from 2026–2027. The first-of-a-kind installation is under construction at the site of the Changjiang nuclear power plant in the Hainan province in China, where CNNC poured first concrete in July 2021. As of the end of 2023, the steel containment dome is reported to have been installed.

Benefiting from lower-cost manufacturing capabilities and cost-saving construction techniques, such as an open-top construction method, Linglong One is estimated to have an average overnight construction cost of $5,000/kW. It holds further reduction potential owing to learning curve and scaling opportunities. With full state support, the design is expected to be deployed widely in China. Use cases include power and heat supply in the North-eastern provinces of Liaoning, Jilin, and Heilongjiang, floating power plants in the Bohai Sea, and power and steam supply along with seawater desalination in the coastal provinces of Zhejiang, Fujian, and Hainan. Among its closest trade partners and allies within the Belt and Road initiative. Additionally, China is likely to promote the deployment of its SMRs by Chinese mining companies operating in Africa.

NuScale VOYGR (NuScale, U.S.)

Despite recent setbacks related to the cancelation of its demonstration project at the Idaho National Laboratory in the U.S., NuScale’s VOYGR is projected to secure around a tenth of the global installed capacity by 2050 (including its floating power plants modification of VOYGR it is developing with in conjunction with Prodigy Clean Energy).

NuScale’ VOYGR is currently the only fully licensed American SMR design (and the second fully licensed design in the world after the Korean SMART). NuScale, however, is still in the process of obtaining the license for its updated, higher capacity 77-MWe design, which is expected to be completed in 2025. It is likely to be the first among the OECD vendors to build a commercially operating plant, expanding rapidly into Eastern and Central Europe, aided by European nuclear regulators’ familiarity with PWR technology and localization options. The company has a mature manufacturing ecosystem and has formed a partnership with ENTRA1 as a developer, offering flexible deployment models, including build-own-operate schemes, similar to the one adopted by Russia’s Rosatom.

To enhance its load-following capabilities the design features a turbine bypass system, for example, which can bypass up to 100% steam at full reactor power directly to the condenser without the need to alter the performance of the reactor itself. NuScale is working toward extending its reactor’s potential applications to the process heat industrial sector, which, due to lower outlet temperatures compared to advanced, next-generation reactors, has been considered out of reach for light water reactors (LWRs). The concept is based on the idea that the steam generated by a standard LWR reactor module can be compressed and heated to produce process steam. Currently the company has achieved a temperature of 500C, with a further potential to extend the temperature to about 650C. This would enable NuScale to supply process heat for oil refining, plastic waste recycling, and so on.

The company is currently on track to build a pilot export plant in Doicesti, in Dambovita County in Romania. At the G7 Leaders in Japan earlier this year, the U.S. administration announced a public-private commitment of up to $275 million to support the deployment of NuScale’s Romanian project. The funding, contributed by the U.S., Japan, South Korea, and the United Arab Emirates (UAE), will aid in material procurement, design work, project management, and site analysis for the project at Doicesti.

The U.S. Export-Import Bank and the U.S. International Development Finance Corporation also issued Letters of Interest for up to $4 billion in project financing. The VOYGR-6 power plant, aiming to produce 462 MWe, is already being licensed by the Romanian regulator. Polish copper and silver producer KGHM Polska Miedź also plans to build a NuScale VOYGR modular nuclear power plant with a capacity of 462 MWe consisting of six modules by the early 2030s.

BWRX-300 (GE-Hitachi, U.S)

GE-Hitachi’s BWRX-300 is also expected to be among the first movers and shakers, by 2050, holding about 5% of the global market share.

Selected by Ontario Power Generation (OPG) in December 2021, the design is advancing toward a construction permit for a pilot plant at the Darlington nuclear station site. If successful, this would represent the first commercial SMR contract in the US. The vendor and operator plan for the first unit to be operational by 2029. In December 2023, Poland’s Ministry of Climate and Environment tentatively approved the construction of six BWRX-300 power plants featuring 24 BWRX-300 reactors across these sites (a combined 7.2 GWe capacity). Orlen Synthos Green Energy (OSGE) announced these locations after shortlisting them for geological surveys.

Strategic advantages of the BWRX-300 include its evolutionary nature and (compared with most advanced designs) limited exposure to fuel security of supply risks, as the design uses standard (boiling water reactor) BWR fuel assemblies. However, licensing BWR technology in countries without previous BWR experience may be time-consuming, as BWRs have a different operational and safety profile compared to more common PWRs. Additionally, due to its size, 300 MWe, the BWRX-300 competes in the highly crowded on-grid market segment, which limits its deployment potential.

GE-Hitachi claims that BWRX-300 enables savings of up to 60% of capital cost per MW “when compared with other typical water-cooled SMR and large nuclear designs in the market” ($2,250/kWe for nth-of-a-kind) and is “deployable globally as early as 2029.” However, historically, almost all ex-ante cost and timeline targets in engineering innovation, both nuclear and non-nuclear, have tended to underestimate—sometimes dramatically—the required resources. Many practical implementation constraints remain unknown until deployment is attempted.

XE-100 (X-energy, U.S.)

X-Energy’s XE-100 reactor is a high-temperature gas reactor (HTGR) designed to operate as a single 80-MWe unit with a possible configuration as a four-unit 320 MWe plant. It is poised to capture a significant market share in the global SMR landscape, potentially reaching 7% by 2050. X-energy and Dow have proposed a four-unit 320-MWe Xe-100 advanced nuclear reactor facility at Union Carbide Corp. Seadrift Operations, a Dow chemical materials manufacturing site in Seadrift, Calhoun County, Texas. X-Energy also has an agreement with Energy Northwest to bring up to 12 XE-100 (960 MWe) units to Washington state, with the first module expected to be online by 2030. Although deployment deadlines may be pushed back, significant support from the U.S. government positions the XE-100 as one of the first advanced reactors to be fully licensed.

X-Energy’s XE-100 is set to capture a significant market share in the advanced co-generation and industrial process heat segment, benefiting from competitive advantages such as a higher outlet temperature (750C compared to the average of 500C), enabling versatile process heat applications so far unreachable by other technologies with lower outlet temperatures. It has its own fuel cycle supply capacities based on the proprietary innovative TRi-structural ISOtropic (TRISO) technology supported by the U.S. government, which reduces fuel security and supply risks. The NNWI report estimates the firm could deploy about 100 reactors by 2050, achieving significant economies of scale and reducing costs.

Five First Movers Could Account for Half the Global SMR Fleet

According to NNWI, taken together, all five first movers are projected to account for over half of the global SMR fleet in 2025 by installed capacity. Evolutionary LWR latecomers, such as NUWARD and Rolls-Royce’s UK-SMR, could potentially secure about 5% of the global market share each, capitalizing on state support. Other designs are currently in the early stages of development but lack substantial backing, such as Holtec’s SMR designs (SMR-160 and SMR-300) and Westinghouse’s AP300, are less likely to reach the full potential learning curve cost reduction stage due to high competition in a relatively overcrowded segment.

Advanced, Generation IV SMRs are likely to encounter substantial delays, with regulators less familiar with the technologies and less mature supply chains. Although some demonstration units might come online by 2035, full-fledged first-of-a-kind deployment and series factory manufacturing is more likely around 2040.

—Tim Yeo is Chairman of the New Nuclear Watch Institute (NNWI) and is a former Minister of State for the Environment with responsibility for climate change policy in the UK Government. As a former Chairman of the UK Parliament Energy and Climate Change Select Committee, he led the work of the Committee on the first report on SMRs. Veronika Racikova is the Executive Director of the New Nuclear Watch Institute (NNWI).