In international trade, a gap between theory and practice has always existed. Theory stresses, as an underlying ideal, the economic benefits of trade based on comparative advantage. In practice, and for a variety of reasons—institutional constraints, political factors, ambiguity of legal doctrine, bilateral or multilateral treaty obligations—the ideal intermittently bows to reality, whether in the form of explicit protectionism or other barriers.

A prominent and highly disputed example concerns the prospective United States’ exports of liquefied natural gas (LNG). A less publicized—but similarly instructive—case involves expanded exports of U.S. coal. Foreign market conditions would appear to represent ideal opportunities for U.S. coal exports. Whereas coal’s role in the U.S. economy has receded markedly and is projected to continue shrinking, its use in Asia—notably China and India—is expected to maintain its robust demand growth for at least the next 25 years. Competitively priced, efficiently mined, and backstopped by large reserves, American coal’s prospective stake in that market is solid, notwithstanding the environmental burden that unconstrained combustion practices may inflict. Yet the fuel is embroiled in controversy—political and environmental—over plans to serve these foreign markets.

An Industry Under Threat

Even to hold its own, much less contemplate a rebound, coal in the United States seems to have a moribund future. After all, it is an industry that, between 1990 and 2010, saw its workforce fall from around 130,000 to 86,000. Although advances in productivity contributed to this change, a flat level of production (at a bit over a billion tons yearly) throughout this two-decade period, an uneven and sluggish trend in exports (which are only now slowly rising), and—especially painful—a dramatic loss to natural gas in new electric power plants all add up to a somber prospect of stagnation. Projections by both the U.S. Department of Energy’s Energy Information Administration (EIA) and the International Energy Agency offer little hope for a rebound: U.S. coal production by 2025 is expected to barely exceed that recorded in 2000. With a sustained preference for natural gas, coal’s use in electric generation—53% in 2000 and 48% in 2010—would fall to around 37%, because its principal customers would be existing coal-fueled plants rather than new ones coming online.

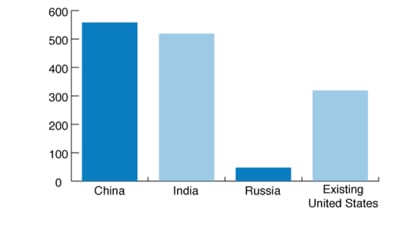

Elsewhere in the world, demand for coal, itself showing appreciably slower growth than during the last decade, would nonetheless continue expanding, with India and China at the forefront of that expansion. (Some two-thirds of China’s electric generation is expected to remain coal-fueled in 2035.) Clearly, the prospect of U.S. exports helping to meet that demand would be one of the few lifelines left for the American industry to survive on, and then only modestly. To be sure, fundamental breakthroughs in carbon capture and containment could alter that picture, but that and other as-yet remote technological changes are not considered here.

Recent U.S. coal exports stood at about 110 million tons a year—about 10% of total production. Some 90% of these exports exit at six major ports, all on the East or Gulf Coast, the most important of which are Baltimore, Norfolk, and New Orleans. To facilitate even moderate export growth—EIA’s baseline projection for 2025 is 115 million tons—it is widely accepted that new transportation capacity, both inland and coastal, is imperative. That’s because, to serve the key Asian Pacific market using Rocky Mountain surface deposits, more dedicated long-haul rail capacity and expanded terminal facilities—logistically favoring Washington and Oregon—would be needed.

The Contending Issues

Notwithstanding expressions of such expansion needs by the coal industry, the last couple of years have seen both protests and legal efforts to forestall that prospect. Though primarily nongovernmental, the opposition also has prompted some expressions of concern by officials at various levels of government. These efforts have little to do with market impacts or statutes explicitly germane to the coal industry. They have everything to do with the programmatic thrust or interpretation of the National Environmental Policy Act (NEPA) or project-specific provisions of such federal statutes as the Clean Air Act. In either case, the filing of environmental impact statements (EIS), where statutorily required, constitutes a core vehicle for the opposition movement.

It’s worth mentioning as well that opposition arguments sometimes have included the point that US coal exports encourage rising worldwide carbon dioxide emissions. The U.S. Environmental Protection Agency (EPA) appears to harbor such concerns, as noted later. However, it is almost certain that U.S. exports merely displace Colombian, Australian, Indonesian, or other coal supplies that would fill the breach created by U.S. export restrictions. In any case, I see no merit in debating in this article how U.S. trade policy should be framed in the light of foreign greenhouse gas policy because such policy questions deserve to be part of a broader analysis and focus on global warming imperatives. Such a wide geographic focus would also need to address the effect of U.S. natural gas exports, which would shift at least some foreign energy use away from coal—never mind that such salutary effects are curiously overlooked in some environmentalist opposition to LNG exports.

If, on purely economic grounds, the case favoring the benefits to both industry and the nation is largely unambiguous, what is one to make of the dissenting—largely, though not exclusively, environmental—position?

On the environmental front, several sources of concern are apparent: the impact of expanded mining; issues like air pollution and increased traffic associated with long-haul rail transport from coal fields to port areas; the disruptive consequences to the communities closest to the to-be-constructed port facilities; and, not least, the extent to which, singly or in combination, these might add more than trivially to U.S. greenhouse gas emissions. In one way or another, each of these aspects is bound to involve regulatory hurdles by federal, state, and perhaps local authorities. It is within the framework of such regulatory oversight that opposition to the coal expansion plans is being waged.

I amplify this development with a couple of specific examples:

- As reported in the Seattle Times, two years ago the firm SSA Marine applied for federal and state permits—triggering a formal environmental review—to construct a $500 million export facility (maximum capacity: 54 million tons) at the Gateway Pacific Terminal near Ferndale, Washington, with plans to launch operations by 2015.

- Subsequently, a proposal by a subsidiary of Arch Coal for a coal port instigated a joint environmental review by Washington State’s Department of Ecology, Cowlitz County, and the U.S. Army Corps of Engineers. The Corps, which has jurisdiction over regional waterways, including the Columbia River, has been advised by EPA to also consider the full range of environmental impacts, from coal mining in Montana and Wyoming to increased coal demand in Asia. In EPA’s words, what it seeks from the Corps is the preparation of “an adequate NEPA review, as governed by the Agency’s responsibilities under provisions of NEPA and the Clean Air Act.”

The impacts explicitly, if illustratively, singled out by EPA for consideration by the Corps are neither general nor few in number. They include such factors as local haze, endangered aquatic species, tribal cultural resources, and incursion into scenic areas. Significantly, EPA also ponders “the cumulative impacts to human health and environment from increases in greenhouse gas emissions . . . from Asia to the United States.” To adequately analyze such far-reaching impacts and still allow permitting decisions to be rendered in a timely fashion could prove to be a formidable challenge. After all, even a near doubling of annual U.S. coal exports (to, say, 200 million tons) has to be judged in the context of foreign consumption of approximately 1.7 billion tons. Whether, with such magnitudes, it is reasonable to expect the Army Corps of Engineers to make a credible determination of CO2 impacts seems open to question.

Opposition to, or questions raised about, these export plans go beyond comments by regulatory agencies and legally framed filings by a number of environmental nongovernmental organizations. Dissenting views have also been expressed by several members of Congress, including Senator Ron Wyden (D-Ore.) and then-Representative Edward Markey (D-Mass), elected to the Senate in July.

In a May 2012 letter to President Obama, the two legislators expressed their concern that “unrestricted” exports of U.S. coal, petroleum products, natural gas, and chemical feedstocks would undermine the benefits of these resources to the domestic economy. Claiming presidential authority under the Energy Policy and Conservation Act of 1975, they urged Obama to “address this problem” and ensure that exports “proceed only to the extent that they are in both the short- and long-term national interest.” However that contention may play out, it seems a bit selective to cite the “long-term national interest” when that objective may be constructively addressed as well—or perhaps more effectively—by measures more likely to reduce worldwide recourse to, and emissions from, coal combustion.

Concluding Thoughts

The economic rationale for coal export plans seems unassailable, given the industry’s domestic stagnation and continued demand growth abroad. Even if foreign coal combustion signifies rising greenhouse gas emissions, the United States has, at best, limited ability to control that outcome because the import needs of China, India, and other countries can be satisfied by suppliers outside of the United States.

I leave it to legal scholars to parse federal statutes invoked to allow a presidential restriction on energy exports. The temptation to exploit the elasticity of the concept of “national interest” is understandable. But it may be risky if that policy route is seen as mainly providing cover in its deference to domestic stakeholders, never mind that it may violate the spirit, if not the letter, of our obligations under World Trade Organization rules. Recall how, a few years ago, Vladimir Putin disrupted westward-bound pipeline gas exports, apparently with the dual purpose of settling political scores with Ukraine and keeping prices low for Russian consumers. A disrupted energy sector in several European countries was an additional consequence. More recently, as recounted in an RFF report by Jhih-Shyang Shih and colleagues, China used its global monopoly position in certain rare-earth commodities to benefit its domestic firms by manipulating exports. Heavy-handed meddling in foreign trade is surely a direction in which the United States would not wish to head.

Environmental issues remain unsettled and deserve attention as part of the broad export debate. Both magnitudes and logistical factors—increased western surface mining, multiple train loads heading to Pacific export terminals, congestion in Oregon and Washington urban areas—constitute developments that, even if not unprecedented, are significant enough to trigger the purview of NEPA, as well as programmatic or project EIS oversight along various links in this lengthy and intricate supply chain.

Ultimately, society’s coal dilemma transcends the U.S. coal dispute. As these observations are written (in early 2013), a new study by the International Monetary Fund spotlights the scope and distorting impact of subsidies in the global energy system. The report distinguishes between two subsidy components: one part calculates the extent to which prices to energy users are set below supply and distribution costs; the other part, much more difficult to estimate, and therefore controversial, primarily addresses the magnitude of “spillover” effects, such as CO2 emissions. While coal accounts for a minimal fraction of the first component—dominated by petroleum-product, electricity, and natural gas subsidies—it is a major factor in the spillover component. Its estimated annual magnitude of some $530 billion in that category is exceeded only by oil-product subsidies of $670 billion. Managing that prospective longer-run and significant environmental impact of global coal combustion doesn’t obviate the importance of dealing sensibly with the export issue, but it is the perspective to which our and the world’s sights need to be concurrently directed.

—Joel Darmstadter is a senior fellow at Resources for the Future. This article originally appeared in RFF’s “Resources” magazine and is reprinted by permission with minor style edits for this publication.