Global resources of variable renewable energy—primarily wind and solar—despite breakneck growth over the past two decades, are beginning to run up against technological and policy limitations on further deployment, and future growth will depend on significant changes in policy and grid design, according to a new report.

Released on September 20, Variable Renewable Energy Sources Integration In Electricity Systems 2016—How To Get It Right was prepared by the World Energy Council (WEC), a global network of energy experts representing 3,000 organizations from more than 90 countries. Among other findings, it notes that while wind and solar offer many benefits, “the total cost and the overall impact of [renewable energy] on national electricity systems is often underestimated by consumers and policy makers.”

Surging Capacity, Lagging Generation

According to the report, global installed capacity of renewable energy (from all sources) has more than doubled over the past decade, reaching 1,712 GW at the end of 2014. In 2015 alone, the 150 GW of new renewable capacity coming online accounted for 60% of all new generating capacity reaching commercial operations. Currently, renewables account for 23% of global annual production, about three-quarters of that being supplied by hydropower.

The WEC reviewed a wide range of data, including case studies from 32 countries worldwide that represent 89% of installed wind and solar capacity and 87% of total generation. It found that despite impressive growth in capacity, operating hours for variable renewables lag well behind other sources.

“World averages of annual equivalent operating hours for different technologies range from 6,300 hours for nuclear to 3,700 hours for hydro, around 2,000 hours for wind and almost 1,200 for solar,” it says.

The report notes that levelized costs for renewable energy sources continue to drop, substantially in the case of wind and solar, but cost ranges remain quite broad, especially for solar. While some solar projects are competitive with non-renewable sources, most are considerably more expensive across their lifetimes.

Challenging Economics

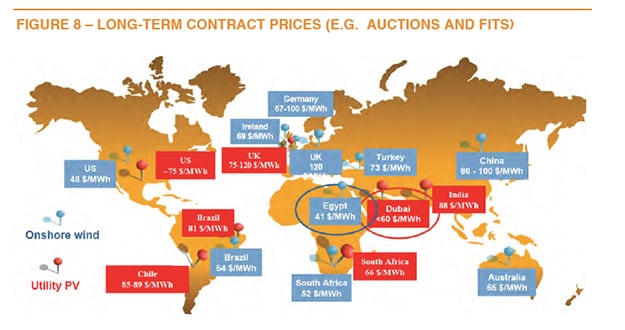

Not surprisingly, economics for wind and solar plants are heavily dependent on the capacity factors they can achieve. The solar projects with the lowest power prices are found in the Middle East, where capacity factors are relatively high, while the most expensive are in northern Europe (Figure 1). The most competitive onshore wind farms are found in North Africa, the U.S., and Brazil, where capacity factors can reach 50%, while the most expensive are typically in Europe and China, where capacity factors are limited for a variety of reasons.

That’s meant a range of results at the retail level. “In countries with electricity markets, [variable renewables] have contributed to the overall reduction of wholesale price, but for most customers this has not avoided significant increase of their bills,” the report says.

One troublesome trend for renewable advocates is the stark drop in new investment in Europe as policy incentives have been scaled back in recent years (Figure 2). Globally, investment in new renewable resources in developed countries has fallen from a high of $191 billion in 2011 to $130 billion in 2015. The bulk of that drop has occurred in the European Union. However, investment in developing countries has grown from $87 billion to $156 billion over the same period, offsetting the decline in the developed world.

The country case studies suggest that part of the reason for declining investment in the developed world has been declining returns—massive investment in some countries’ renewable capacity has produced only small contributions to total electricity production.

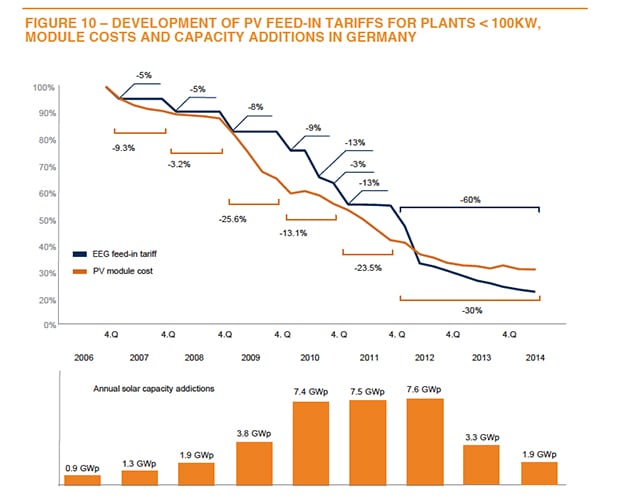

While some nations such as Denmark have managed to achieve high renewable penetration—Denmark’s wind and solar output exceeded 50% of national demand in 2015—others such as Germany have seen relatively little return despite huge growth in capacity. The report notes that although Germany now has total installed wind and solar capacity that exceeds 100% of its maximum peak demand, that capacity accounts for less than 20% of its annual production.

Range of Solutions for Future Renewable Integration

The challenges for greater renewable integration are both economic and technological, the WEC said. A substantial amount of development has occurred in areas that are not ideal for maximum production, which has led to high prices for power from those projects. At the same time, over-generation during periods of low demand in certain areas has led to market disruptions and substantial curtailments.

This has occurred in part because development of transmission capacity has often not kept pace with development in renewable generation. Very often, regions of peak generation are located well away from areas of peak demand, causing grid congestion and forcing curtailments. The conclusion is that the substantial investments in renewable capacity have often not been directed efficiently.

Still, the report says, these challenges are not insurmountable. Improved generation forecasting, greater generation flexibility to address rising intermittency, expansion in capacity and sophistication of electric transmission, and expanded energy storage capacity, will make a substantial difference, the report notes.

Changes in market design are also necessary. “The energy market alone does not provide price signals which are sufficiently strong and effective for long-term planning and security of supply,” it says. Solutions the report suggests are faster scheduling, larger balancing areas, and pooling of smaller production, especially for solar. Revisions to capacity markets, carbon trading, and handling of negative pricing will also be required. “In general, an energy only based market is insufficient to ensure security of supply” in systems with large amounts of renewables.

One thing the report cautions against is one-size-fits-all solutions. “Each country power system is unique, even if some general recommendations can be drawn,” it notes. “Sophisticated technical, economic and regulatory analysis on a project basis must be conducted over an adequate period of time.”

—Thomas W. Overton, JD is a POWER associate editor (@thomas_overton, @POWERmagazine).