Advocates for the continued reliance on coal for baseload electricity cheered late last year when North America’s largest power-related carbon capture and sequestration (CCS) facility was commissioned. Since then, that pool of advocates is evaporating as prominent electricity industry decision-makers publicly distance themselves from coal and champion alternatives for a low- or no-carbon future. If CCS is to rescue coal-based power, time is of the essence.

History shows it’s unwise to bet heavily against coal. At the same time, past performance is no guarantee of future results.

Vocal electricity industry CEOs, such as NRG Energy’s David Crane, have distanced themselves from coal in recent public comments. Even before the U.S. Environmental Protection Agency’s (EPA’s) proposed Clean Power Plan, leading Wall Street banks proclaimed in 2007 through their “carbon principles” that they would not finance coal-fired power plants without carbon capture and sequestration (CCS). Meanwhile, the Canadian province of Ontario reduced its coal share of electricity from 25% to zero in under 10 years.

Historically coal-based utilities, including Tennessee Valley Authority, American Electric Power (AEP), Duke, and Southern Company, are retiring old coal units and building gas-fired combined cycle or nuclear units. Despite CCS research, demonstration, and development programs (see “The Carbon Capture and Storage R&D Frontier” in this issue), the Obama administration’s hostility toward coal is evident in the EPA’s draconian emissions rules for coal-fired power, which essentially are a forcing function for CCS.

Meanwhile, use of coal for power generation grows in China and India, and recently even made a comeback in Europe when natural gas prices went the wrong way and governments pulled back on nuclear power.

Handicapping the future of coal aside, the real question is less whether coal can be economically competitive with CCS and more how fast CCS technology can become a viable commercial addition to a coal plant compared to the techno-economic development of the options it will compete against.

As this article shows, that shrinking pool of advocates for coal had better assume a heightened sense of urgency. With natural gas price forecasts at historic lows, older coal plants being retired at an alarming rate, wind and solar continuing to make in-roads when utilities seek capacity, and a slate of grid-scale energy storage technologies proceeding through development and commercialization, recent setbacks in CCS activities—including the Feb. 3 Department of Energy (DOE) defunding of FutureGen 2.0—loom large.

Scale Required for Success

In the aggregate, the CCS numbers are disturbing:

■ Only three large-scale coal-fired power plant CCS projects likely will be operating in North America by 2020.

■ According to Fossil Forward, issued to the DOE in January by the National Coal Council, the total CO2 capture from all CCS projects operating, under construction, or in advance planning in the U.S. is 65 million tons/year, less than the 77.6 million tons/year CO2 output from just West Virginia’s coal-fired power stations.

■ Of 22 large-scale CCS projects around the world in operation or under construction, fewer than 10 are power-related.

■ The total number of large-scale projects (including those in planning) worldwide is 55, but this is 10 fewer than in 2013, according to The Global Status of CCS: 2014, issued by the Global CCS Institute.

■ Three high-profile U.S. projects—DOE’s FutureGen, AEP’s Mountaineer, and Tenaska’s Trailblazer—have been shelved or cancelled. Another large project, Summit Power, is listed as still in planning.

■ Fossil Forward notes that no CCS option has achieved a technical readiness level (TRL) above 6 on a 0 to 10 scale.

At minimum, a process at commercial size must achieve extended periods of operation (typically several years) under variable operating conditions to qualify for a TRL above 6. TRL is an important metric for the highly regulated power industry because of its generally low tolerance for technical risk. According to Fossil Forward, a conservative definition of a “commercial” technology for the power industry is when it can claim 10% of the installed base or 50% market share for new installations. At the current rate of CCS development, commercial options won’t be available until 2030 in the best-case scenario and more likely not until 2040, according to published reports.

While the bulk of demonstration activity is in the U.S., Canada, and other Organisation for Economic Co-operation and Development (OECD) countries, 70% of the deployments need to occur in non-OECD countries, according to the International Energy Agency, in order to have a meaningful impact on projected average worldwide temperature by 2050. However, China is pursuing only four large-scale projects (beyond early planning) and India none.

Even a 260-MW equivalent power plant CCS project at the Belchatow coal-fired plant in Poland, one of the world’s largest power plants, could not make it past investment hurdles, according to the Jan-Feb 2015 issue of Carbon Capture Journal. Legal issues concerning the CO2 pipeline and sequestration sites were major barriers.

Although processes to recover CO2 from flue gas or other gas streams have been proven and commercial for decades, enormous barriers remain. Barriers for coal-fired power applications are, above all others, scale and geology. Others include the need for:

■ Convergence of technology to minimize technical risk and cost—a dominant technology and several deep-pocket, bankable suppliers competing with value engineering and evolutionary cost reductions.

■ Understanding the impact on grid reliability and operational and maintenance costs.

■ Insurance companies willing to provide coverage.

■ Banks willing to finance debt service.

■ Public utility commissions allowing cost recovery.

Costs Are “In Line”

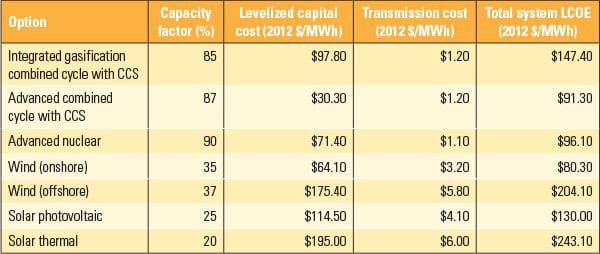

The U.S. Energy Information Administration (EIA) released a report on levelized costs of electricity (LCOE) for new generation resources in its Annual Energy Outlook last year (Table 1). The critical point is that coal with CCS is not economically disadvantaged when you consider that a generating facility that operates, at best, one-third or one-fourth of the time (wind and solar), and unpredictably at that, is different from one that hums closer to 24/7/365. Renewable-sourced generation can be made to resemble baseload when paired with other resources (see “Leveraging Generation Synergies with Hybrid Plants” in the April issue), but storage, for example, would add significantly to the LCOE. Other cost evaluations of generation options show that coal with CCS can compete, once it is proven and commercial.

|

| Table 1. Levelized cost of electricity (LCOE) for new generation (operating in 2019). This table is abridged from the version appearing in the 2014 Annual Energy Outlook. Source: Energy Information Administration |

Retrofits Are Problematic

Prospects for retrofitting CCS to existing plants are not straightforward. According to analyses conducted by Dale Simbeck, SFA Pacific Inc., the following issues present themselves:

■ Many coal units are old and inefficient. Adding CCS would reduce output by 20% to 30% (because of CCS’s parasitic needs) and result in overall fuel-to-electricity efficiencies of 24% to 25%.

■ Space is severely constrained because of the plot area already taken up by the addition of particulate, SO2 and NOx removal processes over several decades.

■ Distance to major CO2 storage or reuse sites is prohibitive, especially for older power plants near urban areas.

■ Permitting long CO2 pipelines may be difficult or impossible.

Simbeck argues that simply replacing older coal plants with gas-fired combined cycles (CCs), with or without CCS, is a better long-term strategy for carbon mitigation than retrofitting coal plants with CCS. His analysis shows that natural gas prices have to surpass $13/MMBtu before it makes more sense to replace older coal units with new coal equipped with CCS.

Because of the large energy penalties associated with CCS, Simbeck and others in the industry prefer to evaluate systems based on CO2 avoided rather than CO2 captured. The cost per avoided ton is higher than the cost per captured ton, because it takes into account the significantly reduced efficiency and output of a unit equipped with CCS, which lead to higher emissions per increment of electricity generated.

Another knotty issue with CCS retrofits is that many techniques to minimize the efficiency and output penalties involve extensive thermal integration of the process with the power generation unit. In other words, according to a report by Worley Parsons, Carbon Capture Overview, retrofitting older units means more than “bolting on” the CCS equipment.

Three Carbon Capture Pathways

The three accepted generic pathways for carbon capture are:

■ Pre-combustion: Coal is gasified to produce hydrogen and CO2, and the latter is stripped out of the syngas before the fuel is burned, usually in a gas turbine.

■ Post-combustion: CO2 is stripped out of the flue gas exhaust from a conventional boiler or gas turbine.

■ Oxy-combustion: Coal is “burned” in a pressure vessel using pure oxygen instead of air.

Both the pre-combustion and oxy-combustion options result in a more concentrated CO2 stream, which reduces the cost and complexity of separation.

The tradeoffs among the three are very intricate. For example, the CO2 stripping unit operation may be smaller and less complex, but a costly air-separation plant is required.

Post-combustion CO2 stripping is most familiar to the power industry—AES has operated a 30-MW equivalent post-combustion CO2 removal process at its Shady Point (Oklahoma) circulating fluidized bed facility for almost three decades—however, contaminants in the flue gas can impair the process. To illustrate: According to the Worley Parsons report, even a power plant with a state-of-the-art SO2 scrubber would require an SO2 polishing step before the flue gas enters the CCS process. Traditionally, utilities overwhelmingly prefer post-combustion emissions control systems because they can be “turned off” if there are operating issues, without jeopardizing electricity output.

On the other hand, pre-combustion, or syngas stripping, enjoys an 80-year legacy of technical optimization and commercial practice in the petrochemical industry, where CO2 removal is called “gas sweetening.” However, coal is far more heterogeneous than oil or natural gas, and the constituents of coal flue gas or syngas—such as ash, O2, ammonia, trace metals, and sulfur—all aggravate the CO2 stripping process and are typically present in much larger quantities than in petrochemical applications.

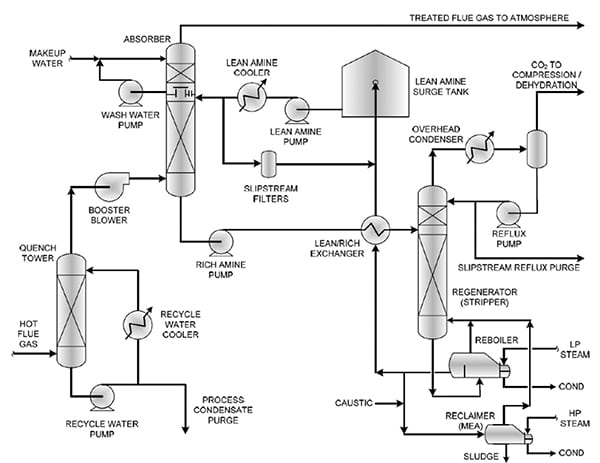

Regardless of technology familiarity, scale remains a challenge. As the Worley Parsons report notes, between 1978 and 2000, at least 12 commercial CO2 capture plants have been commissioned and range in size from 90 to 1,200 tons/day; yet, a 500-MW coal-fired unit will require CO2 capture more like 5,500 tons/day. Also illuminating is that all of these units employ the same basic process (mono-ethanol amine, MEA) with variations in the strength of the solvent and additives, such as inhibitors, used to optimize the process (Figure 1).

|

| 1. MEA absorption regeneration process. The MEA process involves these major unit operations: flue gas cooling (bottom left), mixing and reaction with amine-based solvent (top, right), and stripping of the CO2 from the amine and recycle of the solvent (right side). Courtesy: Worley Parsons |

Whether retrofit or new, the Worley Parsons report concedes that while “there are no clear long-term [CCS] winners, post-combustion is the only proven technology compatible with the world’s huge investment in the fossil-fuel infrastructure.” SFA Pacific’s Simbeck reaches a similar conclusion, stating that only the MEA and modified MEA processes can be reasonably considered by power plant owner/operators at this time.

Technology Contenders

The only currently operating full-scale power generating facility with CCS is Boundary Dam Unit 3 in Saskatchewan, Canada. The CCS technologies used by SaskPower’s Boundary Dam and the other projects expected to start up before 2020 have to be considered leading contenders, having achieved reasonable scale and significant operating time.

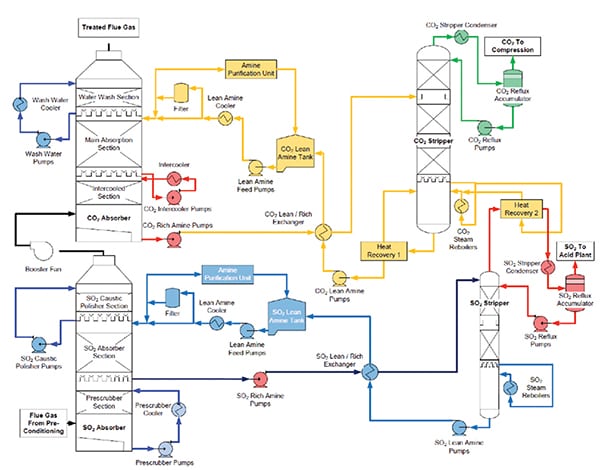

Boundary Dam—Shell Cansolv. TheBoundary Dam project captures and sequesters 90% of the CO2, or 1 million tons annually, from a 1960s vintage 150-MW lignite-fired unit as part of enhanced oil recovery (EOR) operation. CCS and a 66-kilometer pipeline were added as part of a retrofit and refurbishment program that proved to be less expensive than installing a new gas-fired CC, according to SaskPower. Total project cost is close to $1.5 billion, $240 million of which was picked up by the Canadian government. SaskPower reported in February that, after 130 days of commercial operating experience, the performance of the plant was “exceeding expectations.”

The proprietary CO2 stripping process used at Boundary Dam is Shell Cansolv, one of several amine-based chemical solvent processes (Figure 2). Generally, amine-based stripping involves a solvent, such as MEA, di-ethanol amine (DEA), or methyl di-ethanol (MDEA), often with other compounds in the mixture to improve performance. The solvent forms “weak” chemical bonds with CO2, making it easy to strip the CO2 in a subsequent regeneration step, usually by applying heat. Note that Cansolv is a combined SO2/CO2 removal process.

|

| 2. Cansolv. The Shell Cansolv process used at Boundary Dam’s Unit 3 in Saskatchewan employs a proprietary lean amine solvent formulation and removes both CO2 (upper half) and SO2 (lower half) as SO3, which can be further processed to sulfuric acid. Courtesy: SaskPower |

SaskPower reports that the parasitic energy requirements are 21%, lower than the typical 24% to 40% reported for other CCS schemes. The utility has also reported that it could shave $200 million off of a similar project based on the lessons learned thus far. Part of the learning process has involved a pilot unit built and operated at Boundary Dam and another CCS research facility at SaskPower’s Shand station.

After several years of operation, Boundary Dam would qualify for a TRL of 7, according to the National Coal Council report referenced earlier. Important as it is, the Boundary Dam project was originally planned to be three times the size actually completed.

Kemper County Energy Facility—IGCC. Mississippi Power Co.’s integrated gasification combined cycle (IGCC) Kemper County Energy Facility represents the pre-combustion approach. Its essential advantage is that the gasifiers operate at elevated pressures (500 to 1,000 psig) so the CO2 partial pressure is higher in the fuel gas stream and the CO2 fraction is not as dilute. This reduces the size and cost of separation process vessels.

Syngas from a coal gasifier generally contains hydrogen and carbon monoxide. The water-gas shift reaction (in which water and CO react to form hydrogen and CO2) is employed upstream of the CO2 stripping unit. Other impurities (such as sulfur and particulate) are also stripped out upstream.

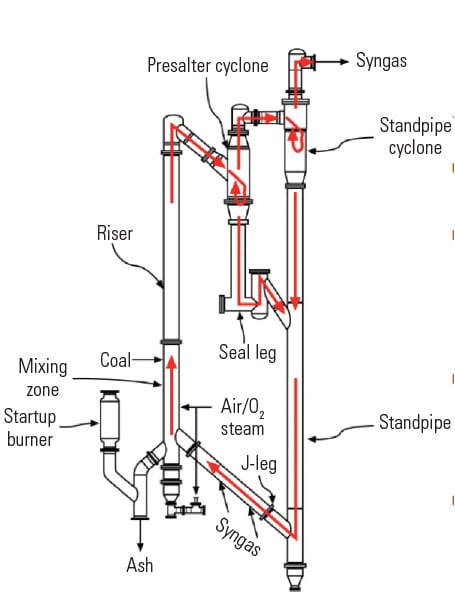

The 582-MW greenfield Kemper project uses Mississippi lignite as feedstock in a gasification process specifically tailored for low-rank coal, called transport integrated gasification (TRIG) and developed by Southern Company and the engineering firm KBR. The process (for power plant applications) is based on air-blown circulating fluidized bed gasification (Figure 3). Most IGCC units operating to date employ oxygen in an entrained bed reactor.

|

| 3. TRIG. The Kemper IGCC is based on the unique circulating fluidized bed gasifier arrangement known as a transport integrated gasification (TRIG) reactor. Source: Southern Company |

The plant has experienced numerous schedule delays and cost overruns (total costs are running close to $6 billion), but the combined cycle has been running on natural gas, and the gasifier/CCS portion is scheduled to start up by May. It is expected that 65% of the CO2 (3 million tons annually) will be captured. As at Boundary Dam, Kemper’s CO2 is destined for an EOR site, 60 miles away. Selexol CO2 stripping is employed and is distinguished from amine-based processes through use of a physical solvent. Generally, physical solvent processes require less steam to strip out the weakly bonded CO2.

The target CO2 emission rate from the facility is 800 lb/MWh, significantly lower than the EPA’s projected standard of 1,100 lb/MWh. Other byproducts from the facility will be sulfuric acid and ammonia.

Once operating for several years, Kemper could qualify for a TRL of 8, according to the Fossil Forward report.

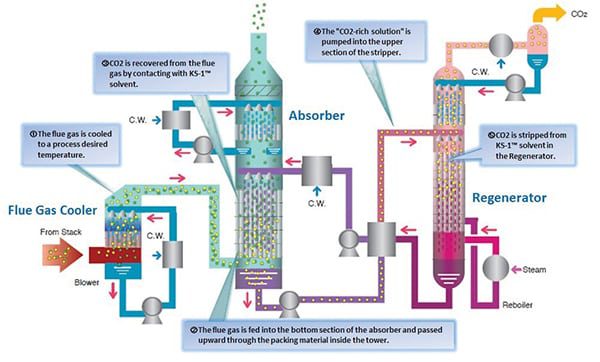

Petra Nova—KM CDR. At the WA Parish plant in Texas, one of the largest coal-fired stations in the U.S., owner/operator NRG Energy will capture 1.4 million tons of CO2 as a 250-MW (equivalent) slipstream (90% CO2 removal) from a 600-MW unit and deliver it via 82-mile pipeline to EOR fields in West Texas. Mitsubishi Heavy Industries’ (MHI) KM CDR process (Figure 4), employing a proprietary solvent called KS-1, will be used to strip the CO2 from the flue gas. This process was tested at Southern Company’s James Barry station at 25 MW equivalent.

|

| 4. KM CDR process. After cooling in the flue gas cooler to 45C or lower, flue gas is fed into the absorber and upward through the packing material inside the tower. As the flue gas passes through the material, KS-1 solvent is distributed evenly, allowing it to selectively capture CO2. KS-1 solvent with captured CO2 is collected in the bottom of the absorber, heat exchanged, and pumped into the stripper, where the CO2-rich solution is distributed onto a strip of internal packing placed in contact with an upward stream of stripping-steam produced by the reboiler. This steam strips CO2 from the CO2-rich solution at the stripper. Finally, the stripped lean solution is cooled and reintroduced into the absorber through the heat exchanger and cooler. Courtesy: MHI |

KS-1 is described as a sterically hindered amine solvent, essentially one where the amine molecule has been modified to improve its ability to react with CO2. According to MHI, KS-1 results in a process that requires 68% of the regeneration energy compared to conventional MEA, exhibits a solvent loss and regeneration rate 10% that of MEA, and a circulation rate that is 60% lower than MEA.

The Worley Parsons report lists two sterically hindered solvents, AMP (2-amino 2-methyl 1-propinol) and piperazine, a cyclical diamine with molecular structure C4H10N2. They combine the higher reaction rates of primary and secondary amines with the lower regeneration energy of tertiary amines. Simbeck notes that KS-1 is “the standard today and likely the best real-world option,” although the chemical industry continues to seek better MEA solvents.

The Petra Nova scheme is unique because an 80-MW gas-fired cogeneration unit is being built along with the CCS to supply the steam and electricity. In addition, the CO2 will be compressed to a pressure (2,115 psia) that allows it to behave as a supercritical fluid—resembling a liquid but expanding like a gas—presumably to lower compression and transport costs. Startup is scheduled for the end of 2016. Cost of the facility is estimated at $1 billion, $167 million courtesy of U.S. taxpayers through the DOE Clean Coal Project Initiative.

Petra Nova would qualify for a TRL of 7 after several years of operation. As an indication of the scale-up this represents, MHI’s largest commercial KM CDR process installed to date is ~450 tons/day CO2 recovery. Petra Nova represents close to 4,000 tons/day or approximately a 10:1 scale-up.

Projects Beyond North America

As mentioned earlier, the non-OECD countries need to deploy CCS if it is to affect global temperatures by 2050. Nowhere is that need more urgent than China, where coal-based electricity production continues to grow. However, projects in that country appear to be moving slowly.

Massachusetts Institute of Technology’s Carbon Capture and Sequestration projects database lists only four projects in China, all in the planning stages. The Global CCS Institute’s November 2014 report, The Global Status of CCS, notes that there are 12 large-scale CCS projects in that country. Four with EOR are furthest along in planning.

Unfortunately, GreenGen, a project once described as the centerpiece initiative to advance near-zero emissions in China, involving coal-fueled generation with hydrogen production and CCS, appears to be moving slowly. The first phase of that project, construction of the 250-MW IGCC facility, has been completed. According to an account in Cornerstone magazine (a coal industry publication), owner China Huaneng Group has been wrestling with achieving continuous operations. Phase II, construction of a 7% syngas slipstream CO2 capture facility, reportedly began last year. Phase III, not expected until after 2020, is the construction of a 400-MW integrated IGCC CCS. The plant processes subbituminous coal.

The other significant power-related project in the Global CCS Institute report for China is a new 1,000-MW power plant with integrated CCS and EOR, described as “newly identified.”

No other non-OECD countries in Asia are listed as having significant power-related CCS activities.

As for the rest of the world, the only other place with significant multi-project activity is the United Kingdom. Five large-scale projects are on the books, but all are in the planning stage with start dates between 2018 and 2020. All are taking advantage of government subsidies.

Other Challenges

Assuming commercial carbon capture options were available today, CCS still presents myriad challenges.

The flexibility of coal units with CCS will be limited and, by extension, their value for dispatch and cycling. The IGCC approach on its own limits operating flexibility compared to traditional boiler-based coal units. When you have numerous interdependent process unit operations, it is difficult for a plant to respond to a dispatch command of, say, plus or minus 100 MW at 10 MW/min. or to run at 30% of maximum continuous rating.

Permitting, monitoring, and liabilities associated with sequestration sites have received less attention than the carbon capture processes; however, like nuclear waste (even after reprocessing), sequestered CO2 has to be managed forever. Geotechnical experience with stored CO2 is limited. A key question is, how long will it take to convince lawmakers and the public that the approach is safe for generations to come?

Although the correlation of gas fracking with earthquake activity has yet to be widely substantiated, similar questions about the long-term geotechnical implications of eventually storing billions of tons of CO2 underground must be considered. Vast differences in underground geologic structures come into play, for which sequestration has to be demonstrated over decades at the least.

Although the early CCS projects are targeting EOR, the CO2 volumes from coal-based power will quickly overwhelm that market. Experts concede that deep saline storage sites dedicated to CO2 sequestration will be necessary, but the research, development, and demonstration work in this area is lagging. The pipelines necessary to move CO2 to storage or use sites could resemble the nation’s natural gas pipeline system.

In the category of unintended consequences, the geotechnical impact of billions of tons of CO2 underground simply isn’t known. After all, 40 years ago, nobody thought pumping it into the atmosphere would ever pose a problem. ■

— Jason Makansi (jmakansi@ pearlstreetinc.com) is president of Pearl Street Inc., focused on technology deployment in the power industry.