Fusion’s first challenge is scientific: can we make it work at scale? Its second, far tougher test is economic: can we make it cheap enough to matter?

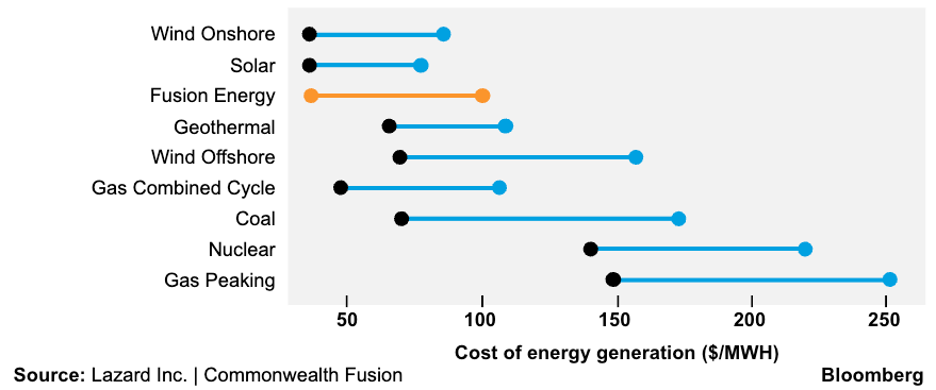

Global private investment has passed $10 billion, governments are launching new programs, and regulators are beginning to streamline pathways for advanced fusion machines. But one question will determine whether fusion becomes a core part of the grid or another cautionary tale: Can it compete on cost? That answer hinges not on physics, but on a brutal cost target: $50 per megawatt-hour.

Unprecedented Demand and a New Energy Baseline

Global electricity use is surging, driven by two hungry forces: AI and a growing worldwide population.

Every step-change in computing has multiplied power demand, and the shift to GPU‑intensive AI inference is no different, with 80-90% of AI compute used for inference. Now think about the billions of queries autonomous agents will execute on our behalf. JP Morgan estimates that data centers, AI, and associated power systems will require $5 trillion of investment in the next five years.

COMMENTARY

Meanwhile, the global population is headed toward 8.5 billion in 2030 and 10 billion by 2061, with much of that growth concentrated in regions still climbing the electrification curve. Put those trends together, and you have one of the largest expansions of electricity demand since the Industrial Revolution.

Fusion can help us meet this demand, capturing 20% of global electricity generation by 2050—but that will require roughly 1,500 1-GW plants. Getting there demands more than scientific breakthroughs. It demands economic ones.

Why $50/MWh Is Required

The grid is already choosing its champions. Today, solar is the clear leader in cost‑effective power generation, and it remains the fastest way to add new capacity. It is the cheapest source of new electricity in the world and the dominant driver of new builds. A one‑gigawatt solar farm can come online in under 18 months, a pattern repeated hundreds of times across the U.S., China, Europe, and India. Combined‑cycle gas also remains highly competitive and bankable, reinforcing a tough economic benchmark for any new technology.

For fusion to win long‑term power purchase agreements, it has to compete within that landscape. As Commonwealth Fusion’s Bob Mumgaard has argued, fusion must deliver energy at around $50/MWh to achieve broad adoption. Fusion’s 24/7 baseload advantage is real, but it won’t matter if the energy costs two to three times more than alternatives.

That cost target has several implications:

- Capital costs for fusion plants must land in the low billions, not the $10–15 billion associated with large fission machines today.

- Construction timelines must shrink. A decade-long build schedule makes fusion uncompetitive against faster, cheaper alternatives.

- Operating costs must be predictable, with modular component replacement from day one.

The Geopolitics of Cost: China’s ‘Sputnik Moment’

Cost competitiveness isn’t just an engineering problem; it’s a strategic one. China has integrated fusion and AI into its latest five‑year plan and is treating the sector as a military‑linked program. It continues to outspend the U.S. on fusion and leads the world in fusion-related patents. More consequentially, China is focused on controlling component supply chains.

Whoever ships the first wave of equipment for commercial fusion plants will effectively define the global vendor stack, from high‑voltage capacitors and superconducting magnets to specialized materials. As we’ve seen with solar panels, batteries, and wind turbines, supply‑chain leadership locks in cost advantages for decades.

For fusion to be both affordable and strategically secure, Western companies need to invest early in domestic and allied manufacturing for components of critical subsystems.

Materials Innovation for Pulsed‑Power Economics

In many fusion concepts, particularly inertial confinement and IMG‑based designs, high‑voltage capacitors are the beating heart of the system. They must store megajoules of energy and deliver it in nanoseconds, surviving billions of cycles without failure.

Today’s capacitor supply chain is concentrated in a small number of vendors, many overseas. And the technology isn’t optimized for the demanding duty cycles of fusion drivers, with legacy materials constraining performance.

That drives up lead times and costs just as fusion developers are trying to move from prototypes to full‑scale drivers. It also opens an opportunity: innovate at the materials and manufacturing level to dramatically improve volumetric efficiency, temperature tolerance, and operational lifetime, which in turn reduces plant costs.

Big Fish, Small Fish: The Coming Wave of Consolidation

When fusion clears its technical and cost hurdles, industry structure will shape who wins. Traditional manufacturers of turbines, transformers, and other heavy power plant equipment are already struggling to keep up with today’s demand.

For example, GE Vernova, one of the world’s largest power systems companies, has said it is sold out on new gas turbines through 2028. It expects 2030 to be sold out by the end of this year. Shortages like these will push major players to explore fusion systems, integrating and selling them into small, medium, and large-scale applications similar to how GE, Westinghouse, and Siemens handle gas and fission solutions.

As fusion projects move from proof‑of‑concept to first‑of‑a‑kind plants, larger industrial players will acquire or partner with fusion startups and advanced component suppliers. The big fish will absorb the small, but only after those smaller firms have proven designs and supply chains.

For innovators in materials, pulsed power, and controls, the path to cost‑competitive fusion runs through strategic partnerships that embed their technologies into platform‑scale offerings.

So, Can Fusion Compete?

Yes, but only if the industry treats cost as a first‑order design constraint and focuses on integration with existing infrastructure. That means aligning plant economics with the cost realities that solar and combined-cycle gas have set.

This will require:

- Designing drivers and power electronics for modularity and maintainability.

- Investing in domestic and allied supply chains before China’s lead becomes insurmountable.

- Leveraging advanced materials to extend equipment lifetime and cut cost per megawatt-hour delivered.

The physics is advancing. The capital is flowing. The regulatory path is clearing. Whether fusion becomes a cornerstone of the 21st‑century grid will depend on decisions made now around critical materials, supply chains, and cost discipline.

—Shaun Walsh is CMO for Peak Nano.