What Worldwide Nuclear Growth Slowdown?

Data detailing plans for new nuclear reactors worldwide show few effects of the March 2011 Fukushima accident. China and Russia in particular continue to be hot spots for nuclear development, but cost overruns, construction glitches, and ongoing safety reviews are slowing construction projects elsewhere.

On paper at least, the March 2011 accident at Japan’s Fukushima Daiichi nuclear power plant that followed a devastating earthquake and tsunami barely altered the list of operating power reactors and nuclear projects planned for construction.

At the end of 2011, there were 435 power reactors in operation with a total capacity of 369 GWe, 2% fewer than at the beginning of the year, according to the International Atomic Energy Agency’s (IAEA’s) annual report published in August. The decrease in generating capacity was due to the permanent retirement of 13 reactors. Twelve of the 13 traced their closure to the accident at Tokyo Electric Power Co.’s Fukushima plant. The tally included four reactors at the Fukushima plant itself and eight in Germany. A 13th reactor was shuttered in the United Kingdom due to its age.

Those closures were offset somewhat as seven new reactors were connected to the grid in 2011, an increase from five reactors in 2010, two in 2009, and none in 2008.

The IAEA said the Fukushima accident slowed nuclear power’s expansion but did not reverse it. Its post-accident projection of global nuclear power capacity in 2030 was 7% to 8% lower than what was projected before the accident. The agency now expects nuclear capacity to grow to 501 GWe in 2030 in its low projection and to 746 GWe in its high projection.

Most of the projected growth will occur in countries that already have operating nuclear power plants. Countries in Asia as well as Russia are expected to be the focus of new expansion projects. Of the 64 new power reactors under construction at the end of 2011, 26 were in China, 10 in Russia, six in India, and five in the Republic of Korea (South Korea).

Despite these plans for new reactors, nuclear power projects face a laundry list of challenges.

French power company Électricité de France SA (EDF) said in August it will delay construction of four planned nuclear reactors in the UK. EDF had planned to start building the first reactors next year. Published reports said EDF now plans to take time to evaluate the consequences of delays at a French reactor under construction in Flamanville as well as the Fukushima accident. EDF is expected to release a new timetable for the UK projects this fall.

Other countries such as Belgium, Italy, and Switzerland have reevaluated their nuclear programs since March 2011. And countries such as Austria, Denmark, Greece, and New Zealand continue to exclude the nuclear power option outright.

In Asia, plans for more than 12.7 GW of new nuclear capacity in South Korea have been delayed amid Fukushima-inspired safety concerns. Korea Hydro & Nuclear Power Co. Ltd. pushed back the date for completing two reactors by at least 10 months due to a delay in government approval. The reactors were first scheduled to enter service in 2016 and 2017. In addition, construction of four other reactors has been pushed back by at least one year. And plans for two other reactors have been scrapped altogether, according to local news reports quoting company officials.

In Japan, nonbinding plans (that could be reversed) were announced by the government in mid-September to phase out nuclear power by 2040. The “policy goal” called for all 50 of the country’s reactors to close once they reach 40 years in operation. In addition, no new reactors would be built. At a press briefing in Tokyo, National Policy Minister Motohisa Furukawa said, “We will introduce policies to bring nuclear power generation down to zero within the 2030s… so that we can build a society that does not rely on nuclear power as early as possible.” Before the March 2011 accident, nuclear supplied 26% of the country’s electricity. Long-term plans had been in place to raise that contribution to 53% by 2030.

Higher Costs and Delayed Starts

Closer to home, the first new nuclear plants in the U.S. in years are costing more to build than first thought and are experiencing construction delays that are pushing back their projected in-service dates. Some plans for new reactors have been scrapped altogether. For example, NRG Energy wrote off a $481 million investment in two planned reactors in Texas shortly after the 2011 Fukushima accident, citing uncertainties.

The Associated Press reviewed public records and regulatory findings and said licensing delay charges, rising construction costs, and construction errors are driving up the costs of reactors in Georgia, South Carolina, and Tennessee anywhere from hundreds of millions of dollars to as much as $2 billion. Some of the news agency’s reporting focused on work at the Vogtle, V.C. Summer, and Watts Bar stations:

- Plant Vogtle. The Associated Press reported that the Georgia Power–led Vogtle project, initially estimated to cost $14 billion, has run into more than $800 million in extra charges related to licensing delays. A construction monitor hired by state regulatory authorities has said that co-owner Southern Co. is having trouble holding to its budget. The plant, whose first reactor was supposed to be operational by April 2016, is now delayed seven months (Figure 1). Southern Co. and others say cost overruns are to be expected in projects this complex, and that overruns are balanced by other savings over the life of the plant. Southern Co. expects Plant Vogtle will cost $2 billion less to operate over its 60-year lifetime than initially projected because of tax breaks and historically low interest rates.

1. Steady progress. The new Units 3 and 4 at Plant Vogtle are beginning to take shape. In the foreground is the foundation for the turbine building (right) and the containment vessel (left). In the middle of the photo are the same foundations for Unit 4. On the far left are the foundations for the hyperbolic cooling towers, one per unit. In the background, the prefabrication of the containment shells continues. The photo was taken in August 2012. Courtesy: Southern Co.

- V.C. Summer Nuclear Station. This South Carolina reactor was expected to cost around $10.5 billion but has experienced cost increases of around $670 million, the news agency said. Owners say the project remains on or under budget, helped by favorable interest rates and labor costs that are lower than expected. The first reactor’s in-service date has been delayed from 2016 to 2017; the second reactor reportedly is eight months ahead of schedule with an in-service date targeted for early 2018.

- Watts Bar Nuclear Plant. Completing work on the long-mothballed Watts Bar plant in eastern Tennessee, initially budgeted at $2.5 billion, will cost up to $2 billion more, the Tennessee Valley Authority (TVA) said this past spring. The utility said its initial budget underestimated how much work was needed to finish the plant, and the utility wasted money by not completing more design work before starting construction. The project had been targeted to finish this year but has been postponed until 2015.

Another utility in line to build, Progress Energy—which completed its merger with Duke Energy this summer—pushed back construction plans for two reactors in Florida because of economic uncertainty, low demand growth, and inexpensive natural gas for power generation. Progress now expects its first new reactor to be finished in 2024.

Meanwhile, Progress faces problems with its existing Crystal River nuclear plant. The reactor went offline in September 2009 for maintenance and upgrades, but the plant’s 42-inch-thick concrete containment building cracked during the outage. Efforts to repair the damage cost $500 million and resulted in more cracks. Repairing the new cracks was first estimated to cost another $900 million to $1.3 billion, plus more than $1 billion for replacement power.

In early August, Duke Energy CEO Jim Rogers said the previous high-end estimate of $1.3 billion is likely too low. The utility has not decided whether to repair the plant or permanently shut it down. An independent technical evaluation commissioned by Duke’s board was expected to be completed in early September, Rogers told a local newspaper. “The cost estimate is trending higher,” Rogers was quoted as saying. “The repair plan appears to be technically feasible but issues remain.”

The U.S. Nuclear Regulatory Commission in early August put a hold on requests for new reactor construction and license renewals.

Spent Fuel Storage Dilemma

Further complicating new nuclear’s outlook, the U.S. Nuclear Regulatory Commission (NRC) in early August put a hold on requests for new reactor construction and license renewals after a federal court ruling questioned the agency’s plans for storing spent nuclear fuel (SNF).

The NRC’s moratorium will delay almost 20 requests by utilities for new construction and operating licenses or license renewals. Those projects include Ameren Corp.’s bid for a 20-year license renewal at its Callaway plant in central Missouri, a renewal request by the Calvert Cliffs power plant in Maryland, and a request by Florida Power & Light to build two reactors at its Turkey Point nuclear plant south of Miami.

Some two dozen environmental groups sought the delay after a federal appeals court ruled in June that the NRC’s plans for long-term storage of SNF at individual reactors were insufficient. The ruling came in response to a lawsuit by attorneys generals in New York, New Jersey, Connecticut, and Vermont over a relicensing application for the Indian Point nuclear plant. The federal appeals court found that spent nuclear fuel rods stored onsite at power plants “pose a dangerous, long-term health and environmental risk.”

The NRC sought for decades to build a national waste storage site at Yucca Mountain in the Nevada desert, but that plan was scrapped two years ago by the Obama administration.

A decision in August offered good news to North America’s nuclear industry when Canadian nuclear regulators issued a site preparation license to Ontario Power Generation (OPG) for new reactors proposed at the Darlington site in Ontario. The license was the first to be issued in Canada in 25 years and will be valid for 10 years. It means that preconstruction activities such as clearing, excavating, and grading the land adjacent to the company’s existing four-unit Darlington station can begin.

Two potential vendors are preparing detailed construction plans, schedules, and cost estimates under service agreements signed with OPG in June. SNC Lavalin/Candu Energy Inc. and Westinghouse have a year to complete their reports for the Enhanced Candu 6 and AP1000 reactor designs respectively. The reports will be submitted to the Ontario provincial government, which will decide whether to move forward with the project.

Planned Reactor Construction

The U.S. currently has 104 operating nuclear reactors at 64 plants across the country. Around half of those units are more than 30 years old. The Nuclear Energy Institute says 19 companies and consortia are studying, licensing, or building more than 30 reactors. The NRC is reviewing 10 combined license applications from nine companies and consortia for 16 nuclear power units. Even so, work is actively under way at just a handful of sites, and one major international nuclear group—the World Nuclear Association (WNA)—counts only the Watts Bar reactor as currently under construction. It considers a plant “under construction” only after first concrete for the reactor has been poured. By that measure, neither Vogtle unit appears on the WNA’s tally even after three years of work at the site.

Research by POWER on data maintained by the WNA suggests that globally, plans for new nuclear generating capacity rose between 2008 and 2012 despite the effects of the worldwide economic crisis and the Fukushima accident.

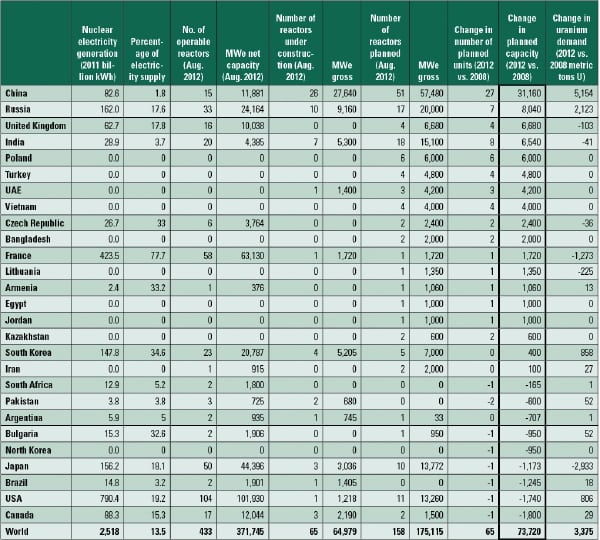

As Table 1 shows, almost 74 GW of planned capacity representing 65 reactors were added to the list of planned reactors worldwide between 2008 and August 2012. China added the most planned units, 27, which if built, would add more than 31 GW of nuclear generating capacity. (See p. 48 for more on China’s nuclear plans.) The WNA said China had 26 reactors under construction as of August, with a combined 27.6 GW of generating capacity. China currently has 15 reactors in service with a combined generating capacity of 11.9 GW.

Table 1. Nuclear remains a part of generation plans worldwide. Source: World Nuclear Association

Russia increased the number of its planned nuclear units by seven between 2008 and 2012. It now plans to build 17 reactors with a combined 20 GW capacity. Russia has 10 reactors under construction at present, representing almost 9.2 GW of capacity. Its installed capacity is almost 24.2 GW at 33 reactors.

WNA data show that 16 countries increased the number of planned nuclear reactors between 2008 and 2012. Those increases account for 74 reactors and a combined generating capacity of more than 82.5 GW.

At the other end of the spectrum, WNA data show that the number of planned reactors fell by one each between 2008 and 2012 in South Africa, Argentina, Bulgaria, North Korea, Japan, Brazil, the United States, and Canada. Those losses equal around 8.7 GW of generating capacity. Pakistan was the only country to cut its number of planned reactors by two during the four years between 2008 and 2012. It currently has no plans to add more nuclear power. Pakistan has two reactors under construction with a combined capacity of 680 MW and three reactors currently operating with a combined capacity of 725 MW.

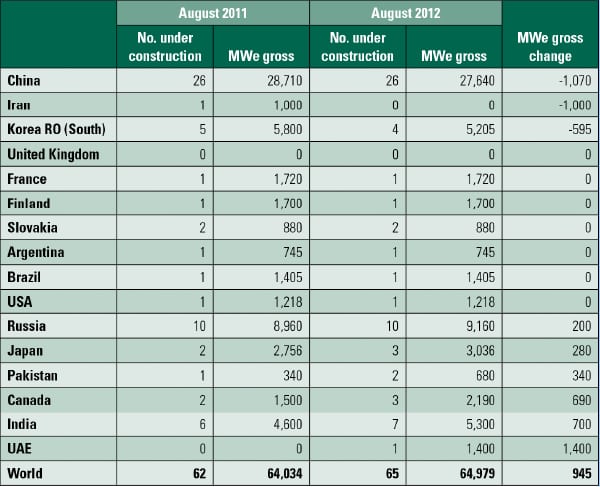

The Fukushima accident had little effect on the gross amount of new nuclear capacity under construction worldwide, even in Japan, where the accident took place. According to WNA data in Table 2, three reactors with a combined 3,036 MW of capacity were under construction in Japan as of August 2012. That was up from two reactors and a combined 2,756 MW reported in 2011. Worldwide, almost 65 GW of nuclear generating capacity was under construction in August. That was up 945 MW from 2011.

Table 2. Fukushima had little impact on global reactor construction plans. Source: World Nuclear Association

The WNA expects almost 10.6 GW of nuclear capacity to enter service this year (Table 3). That includes three units in India, two in South Korea and China, and one each in Russia, Argentina, and Iran. The WNA also counts in its 2012 total the completion of refurbishment work on three units in Canada: Bruce A1, Bruce A2, and Point Lepreau Unit 1.

Table 3. Nuclear reactor expected in-service dates. Source: World Nuclear Association

Next year, some 14.9 GW of capacity are expected to be completed, representing 13 reactors. The count includes seven reactors in China, two each in Slovakia and South Korea, and one in Russia. One U.S. completion included in the WNA’s count for 2013—Watts Bar Unit 2—is likely to slip to 2015 after TVA revised its expected completion date earlier this year.

Uranium Supplies

Increased nuclear generating capacity seems unlikely to tax global supply channels for uranium. World uranium resources appear ample to meet requirements for the foreseeable future, but timely investment in facilities will be needed to make sure production keeps pace with growing demand, according to a new edition of the “Red Book” published jointly by the IAEA and the Organization of Economic Cooperation and Development’s Nuclear Energy Agency.

The latest Red Book edition concluded that total identified uranium resources have increased by more than 12% since the last edition, which included data up to 2009. Even so, lower-cost uranium resources were found to have decreased “significantly” due to increased mining costs. Nevertheless, with total identified resources standing at 7,096,600 metric tons (mt) of uranium (U) recoverable at costs of up to $260 per kilogram, identified resources reportedly are sufficient for at least 100 years of supply for the world’s nuclear fleet. So-called undiscovered resources (defined as resources thought to exist based on existing geological knowledge but requiring significant exploration to confirm and define them) stand at 10,400,500 mt.

WNA data suggest that growth in global demand for uranium for electricity generation rose 3,375 mt between 2008 and 2012, as shown in Table 1. The increase occurred even as Japan cut its demand for the fuel by almost 3,000 mt over the period. That drop was more than offset by demand growth in China (up 5,154 mt from 2008 to 2012) and Russia (up 2,123 mt). U.S. demand rose 806 mt and Canadian demand rose 29 mt.

The Red Book said the increase in the uranium resource base stems from concerted exploration and development efforts. Some $2 billion was spent on uranium exploration and mine development in 2010, a 22% increase from 2008 figures, with a focus on areas with the potential for hosting in-situ leach (ISL) recovery operations.

The report ranked Kazakhstan as the world’s leading uranium producer—standing at 54,670 mt in 2010—in a period when global production has increased by more than 25% since 2008. Two countries joined the list of those reporting uranium production figures since the previous Red Book: Malawi, which started uranium production in 2009, and Germany, where uranium production resumed through uranium recovery from mine remediation work.

Globally, ISL is now the dominant mining method, accounting for almost 40% of 2010 production, the result of ISL production increases in Kazakhstan. Underground mining’s share stood at 32%, open pit mining at 23%, and co-product and byproduct recovery from gold and copper mining operations made up 6%.

The world’s operating commercial nuclear power reactors cumulatively required 63,875 mt of uranium per year in 2010. By 2035, this is forecast to grow to between 97,645 mt and 136,385 mt, depending on growth scenarios. The scenarios take into account the effects of policies introduced by some countries following the March 2011 Fukushima accident.

Currently defined uranium resources are “more than adequate” to meet the high case demand as far out as 2035, but not without “timely investments” in uranium production facilities, the report said. “Significant investment and technical expertise will be required to bring these resources to the market and to identify additional resources. Sufficiently high uranium market prices will be needed to fund these activities, especially in light of the rising costs of production,” it said.

In August, Canada’s minister of environment approved a deep open pit mine at Midwest, near McClean Lake in Saskatchewan. AREVA Resources and Denison Mines are also evaluating other potential mining methods, including conventional underground and surface jet bore drilling, using Surface Access Borehole Resource Extraction mining technology. The deposit has indicated resources of 16,500 mt of uranium at 4.66% U. Milling will be at McClean Lake, 15 kilometers away. There are no current plans to start mining.

Secondary sources of uranium (stockpiles of natural and enriched uranium, downblended weapons-grade uranium, reprocessed used fuel, and the reenrichment of depleted uranium tails) will continue to be required, although their role is expected to decline post-2013, when agreements between Russia and the U.S. to downblend highly enriched uranium from nuclear weapons for use in nuclear fuel expire.

— David Wagman is executive editor of POWER.