Increasingly, today’s electric power grids are interacting with microgrids and in more complex ways. Yet, much work needs to be done to integrate microgrids and flexible demand into the wide-area synchronous grid to enable broader, fairer, and smoother participation in grid service markets, which should help reduce electric costs and improve service reliability for all. Studies indicate that renewable generation microgrids are now competitive with gas generation for reliability and cost.

Small electric grids have been around since the beginning of electric power, but with modern wide-area synchronous grids, microgrids are now the dominant form for small electric systems. Early electric grids were powered by bulky fossil fuel-powered engines and evolved from direct current grids to alternating current grids with central generation as grids quickly expanded across the first electrified cities. Still today, organizations often use small diesel/gas-powered generators as a backup for grid failures.

Diesel/gas generators are self-contained grid systems that typically maintain voltage and match loads. As diesel/gas generator operating costs are high, it is not normally economical to export diesel/gas-generated power into the wide-area synchronous grid.

The situation is different with new distributed wind and solar generation. These new renewables, along with gas generation, are the main source of new power generation and are replacing retired central station power generation. Power from distributed solar and wind can serve local loads, reduce transmission loads, and export power to the wide-area synchronous grids. However, large remote generation sites may need new transmission to connect to loads in distant population centers.

Some large solar and wind farms are generators without island capability that are connected to larger wide-area synchronous grids. Adding battery storage or diesel/gas generators to solar or wind generation forms a microgrid (Figure 1) and can provide potentially valuable island operation, increasing local power reliability and resiliency. Distributed energy microgrids are normally connected to the wide-area synchronous grids and microgrids are increasingly providing more advanced services than just bulk export power and serving local loads.

|

|

1. A microgrid can utilize a variety of generation and storage options to increase power system reliability and resiliency for the loads being served. Source: Shutterstock |

Benefits and Challenges of Distributed Microgrids

Distributed microgrids present a business model challenge to investor-owned utilities and transmission systems as these microgrids are increasingly able to compete in wholesale energy, capacity, and ancillary services markets, and displace utility loads and utility revenue. Utilities are increasingly building their own renewable generation, often with a microgrid architecture to meet the demands for new generation and grid reliability required by regulators, but utilities are being asked to do much more than compete with distributed power. ISOs, RTOs, utilities, and regulators are working to transition electric grids to allow fair competition to provide reliable low-cost power. Utilities were once a natural monopoly. Now, they are being asked to help build out an efficient, workable, low-carbon distributed system, and figure out how they will fit into that system.

ARC Advisory Group market studies of microgrids and grid-scale battery suppliers show these markets growing, with large compound annual growth rates. The traditional grid hardware, software, and service providers are very strong suppliers to the microgrid market. Many smaller suppliers have also emerged in the nanogrid market for residential PV systems with battery storage.

Worldwide, lithium batteries have established a strong lead in the market for grid-scale batteries in part by the economies of scale. PJM Interconnection, an early adopter, demonstrated that lithium batteries can be used effectively for grid frequency control applications. As the markets for frequency control get saturated, there are many other markets where new grid-scale battery applications can compete.

Basically, a grid-scale battery with a modern power inverter/converter is an instant microgrid all by itself. Coupling microgrids to meet demand-side flexibility is a problem that must be solved. This will require new technology, new regulations, and new business models, and the smart grid to perform new tasks it was designed to do but has never done before at scale.

Possible Solutions

The Electric Power Research Institute’s (EPRI’s) Integrated Energy Network (IEN) concept is described in its U.S. National Electrification Assessment report, issued in 2018. The EPRI concept of an IEN—the idea that the effective integration of energy supplier and user networks can and will lead to more reliable, flexible, and affordable energy services—implies some big changes ahead and plenty of opportunities for smart grid-connected home automation to reshape how consumers can use their load flexibility to save money and restructure the future electric grid.

The power industry has always had the choice to integrate the user side of the grid to reduce peaks and smooth loads. Pumped-hydro storage was built in some cases to avoid cycling nuclear plants; the new distributed generation grid also needs that type of operational flexibility. So, what is different now that we need to integrate to the demand side? The difference is the system now has unprecedented network communications, digital technologies, mobile devices, smart meters, smart grid standards, and the electrification of transport and building heating, ventilation, and air conditioning (HVAC). These enable far greater flexibility to adjust demand on the user side of the grid. While this is arguably the most complex systems integration problem society faces today, ARC believes all the technology needed to succeed is in place.

While natural gas has an important role to play, The Economics of Clean Energy Portfolios—published in 2018 by the Rocky Mountain Institute (RMI)—warns of the high costs of a rush to gas generation. RMI provides business-model research to show renewable energy, including wind and solar, and distributed energy resources, including batteries, have fallen precipitously in price in the last 10 years. At the same time, developer and grid operator experience with these resources has demonstrated their ability to provide many, if not all, of the grid services typically provided by thermal power plants. This renewable electric generation in the context of the future IEN is a major driving force for microgrids.

Electric grids are increasingly deregulated, but deregulation has a long way to go before small players can compete in all the markets where large generators or large loads currently do. Grids are already using local marginal pricing (LMP) to drive generation and loads, but this price is meaningless to small users. Even with smart meters and smart grid standards, small microgrids and nanogrid operations have not reached the point where they are driven by the real-time local price of power.

More homes will have solar PV and batteries, electric vehicles, heat pump hot water heaters, and electric-driven HVAC systems, but how can homeowners with flexible loads participate in the IEN? How can they be compensated for the grid services they might provide? PV battery systems do not support power export, electric vehicles do not support V2G (vehicle-to-grid) or remote charging applications, heat pump hot water heaters do not support scheduling, end-users cannot buy Wi-Fi enabled residential circuit breakers that support grid price scheduling, and the mobile apps for HVAC controls today are not ready to integrate with the future IEN.

The smart grid, smart home, and smart appliances and devices will need connectivity with these new technology and business applications. New communications and grid real-time pricing integration that supports mobile devices are missing today. They are quite complex because they need to work within the market rules, and safety and operational constraints of the physical electrical system. The speed of this transition depends on the path society will take to decarbonize the electric grid, as well as on innovative new products and services. There is a need to aggregate many smaller microgrids and nanogrids into an entity that is large enough to compete in electric markets, but the challenge to organize and control many small electrical systems remains formidable.

Architectural Options

A major advance in electricity pricing theory occurred in 1988 when four professors at the Massachusetts Institute of Technology and Boston University (Fred C. Schweppe, Michael C. Caramanis, Richard D. Tabors, and Roger E. Bohn) published a book titled Spot Pricing of Electricity. It presented the concept that prices at each location on a transmission system should reflect the marginal cost of serving one additional unit of demand at that location. It then proposed a control system solution to determining these prices by solving a system-wide cost minimization problem while complying with all the system’s operational constraints such as generator capacity limits, locational loads, and line current limits. The problem is solved using linear-programming (LP) optimization algorithms. The LMPs then emerged as the LP solution by computing the shadow prices for relaxing the load limit at each location. ISO New England runs such an LP every 10 minutes, and participating generators and loads act directly on this LMP calculation.

In the U.S., these grid control ideas led to the Energy Policy Act of 1992. To transition from vertically integrated business monopolies and increase competition via pricing mechanisms, utilities have seen a continuing stream of deregulation worldwide. In the U.S., the Federal Energy Regulatory Commission issued the landmark order 888 in 1996, which was intended to deregulate the vertical electric power market and separate generation from transmission.

Various market-based reforms are still ongoing. Some implementations have had partial success, but the transactive energy market—a system of economic and control mechanisms that allows the dynamic balance of supply and demand—is far from a solved problem, with plenty of technical implementation issues and no shortage of political influences. The regulatory framework, business models, and technical integration issues remain unsolved as aggregators struggle to include such small grid players into the grid markets.

The Tale of Two Visions

The need for reliability and resilience is increasingly important as power customers continue to suffer economic losses from outages. Existing coal and nuclear plants are in decline, especially in the developed world of North America and Europe. China has essentially paused new nuclear plant development but has managed to build out generation capability that is more than 50% larger than U.S. generation. Solar, wind, and natural gas are dominating new power generation worldwide. Solar is overtaking wind for new generation in many parts of the world and solar deployments at the residential level mean there are many small generators.

There are many ways to structure the grid architecture, but here are two contrasting visions. One option is called Grand Central Optimization where the transmission system operator (TSO) interacts directly with all grid players. A second option is the Layered Decentralized Optimization distribution system operator (DSO). These are described in more detail in an IEEE report by Lorenzo Kristov (who previously worked at CAISO), Paul De Martini, and Jeffrey D. Taft titled A Tale of Two Visions: Designing a Decentralized Transactive Electric System, and also a more recent summary written by David Roberts titled “Clean energy technologies threaten to overwhelm the grid. Here’s how it can adapt.”

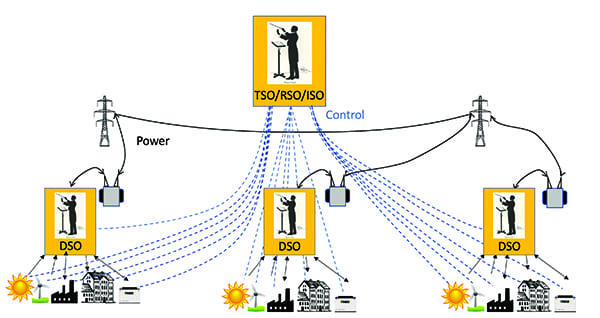

The Grand Central Optimization Vision. The Grand Central Optimization vision (Figure 2) is the logical extension of the wholesale market structure that exists in TSO areas today, but with many more and diverse distributed energy resources (DERs) participating in the wholesale markets. This includes DERs on both the customer and utility sides of the meter. It would be quite complex for a single residence to enter into a business relationship with the wholesale markets and equally difficult for a TSO to deal with every single small customer. Some level of aggregation appears to be required.

|

|

2. In the Grand Central Optimization vision, the transmission system operator (TSO) interacts directly with all grid players including distribution system operators (DSOs). Courtesy: ARC Advisory Group |

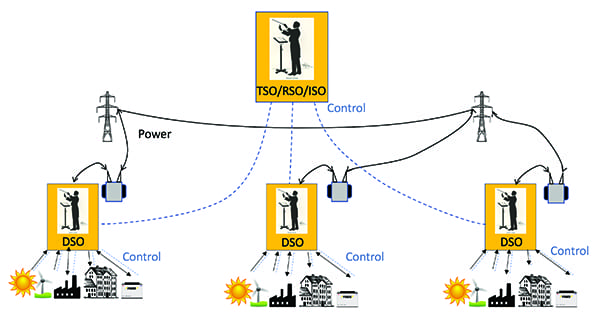

The Layered Decentralized Optimization Vision. Instead of numerous DERs (microgrids and nanogrids) bidding directly into the wholesale market, and being scheduled and dispatched by the TSO, with the Layered Decentralized Optimization option (Figure 3), the DSO would aggregate all DERs within each local distribution area (LDA). This would include DERs that are aggregated into virtual resources by third-party aggregators. In this model, an LDA is defined as the distribution infrastructure and connected DERs, and end-use customers below a transmission-distribution (T-D) interface substation or LMP pricing node. The total DSO would then provide a single bid to the wholesale market at the T-D interface. This allows the LDA to buy or sell energy, and offer capacity and ancillary services, to the transmission grid. This is the distributed control option.

|

|

3. In the Layered Decentralized Optimization vision, the DSOs aggregate all distributed energy resources within each local distribution area. Courtesy: ARC Advisory Group |

One Problem at a Time

The ability of electric grids worldwide to move from largely central generation to increasingly distributed generation is arguably the most complex systems integration problem of our time. Liu Zhenya of China’s “state grid” (with nearly a million employees and 1.1 billion customers) has grand plans for transmission lines to connect the whole world, starting with all of Asia. The evolving connection of physical grids requires a corresponding architecture of the grid control system and the grid business system. While a single worldwide grid is a grand futuristic vision, the general issues of connecting smaller grids down to the scale of micro and nanogrids is the kind of difficult problem that our grid regulators, utilities, aggregators, politicians, and technical communities must solve to be able to provide reliable electric power fairly and efficiently. ■

—Rick Rys is a senior consultant based in Dedham, Massachusetts, with the ARC Advisory Group.